TDS on salary: Do not pay higher taxes! Choose between new and old tax regimes wisely

Income tax: As per CA Ruchika Bhagat, MD, Neeraj Bhagat & Co., choosing the right tax regime from the old tax regime and the new tax regime can help taxpayers save more tax.

)

Income tax: If you have ever viewed your pay slip as an employee, you may have noticed that there is a gap between your CTC and your in-hand salary. That is because employers deduct tax from your salary before paying it in your account and deposit it with the government on behalf of the employee.

This deduction made by the employer is tax deducted at source or TDS. Section 192 of the Income-tax Act of 1961 deals with TDS on salaries. It requires all employers to calculate income tax on salaries that exceed the basic exemption limit and to deduct TDS on salary payments.

So how can you pay less tax on your salary?

As per CA Ruchika Bhagat, MD, Neeraj Bhagat & Co., choosing the right tax regime from the old tax regime and the new tax regime can help taxpayers save more tax.

Let's first take a look at both regimes.

New Tax regime

As of FY 2023-24, the new income tax regime is set as the default option. If one wishes to continue using the old regime, they must submit the income tax return along with Form 10IEA before the due date. There is also an annual option to switch between the two regimes to assess tax benefits.

In the 2023 budget, the government implemented five significant changes, which persist into FY 2024-2025, as no alterations were made in the interim budget of 2024. These changes included:

>>Introduction of full tax rebate on incomes up to Rs 7 lakh, compared to Rs 5 lakh under the old tax regime.

>> Elevation of tax exemption limit to Rs 3 lakh, accompanied by revised tax slabs.

>> Extension of standard deduction of Rs 50,000, previously exclusive to the old regime, to the new tax regime as well. Together with the rebate, which results in Rs 7.5 lakh as tax-free income under the new regime.

>> Deduction in family pension claim of Rs 15,000 or 1/3rd of the pension, whichever is lower.

>> Reduction in the surcharge rate on income over Rs 5 crore from 37 per cent to 25 per cent, leading to a reduction in the effective tax rate from 42.74 per cent to 39 per cent.

>>Increase in the exemption limit for non-government employees from Rs 3 lakh to Rs 25 lakh, marking an eight-fold increase.

Old tax regime

Within this framework, taxpayers have access to over 70 exemptions and deductions, encompassing benefits such as HRA and LTA, aimed at diminishing taxable income and consequently reducing tax liabilities. Among these, Section 80C stands out as one of the most favored and substantial deductions, permitting a reduction of taxable income up to Rs.2.5 lakh.

Taxpayers are afforded the flexibility to choose between adhering to the old tax regime or transitioning to the new one, depending on their financial circumstances and preferences.

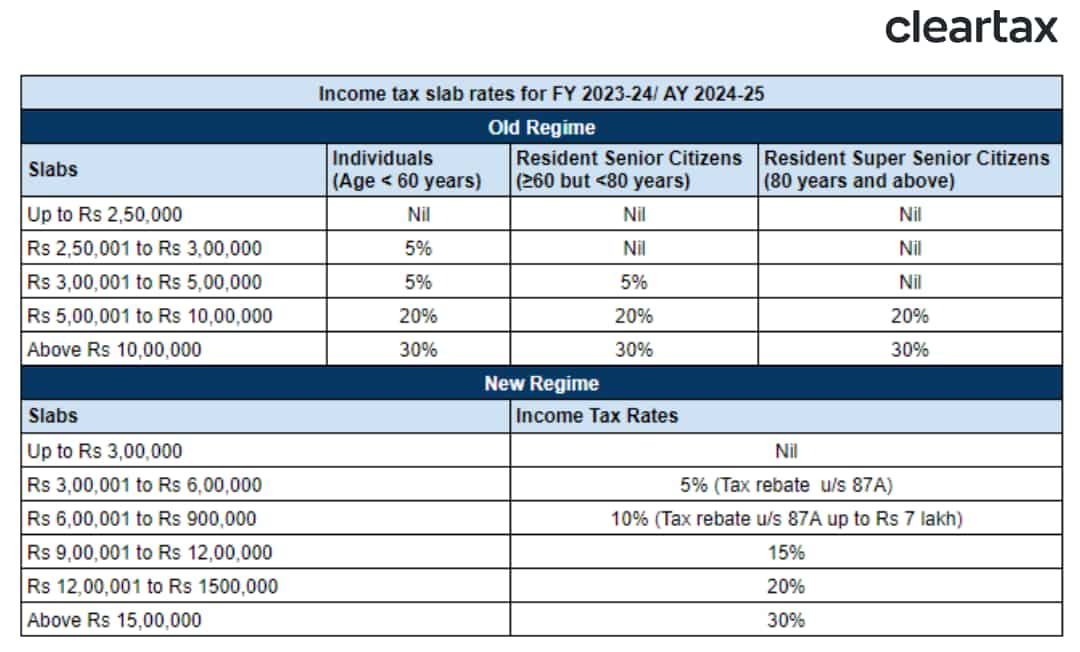

New and Old Tax slabs and rates

Which regime should one choose to save more tax?

As per Bhagat, both regimes have their pros and cons. While the old tax structure encourages saving habits, the new one favours employees with lower earnings and investments, albeit with fewer deductions and exemptions.

Furthermore, the new system is perceived as safer and simpler, reducing the potential for tax evasion. However, due to the unique circumstances of individual deductions and exemptions, a comprehensive comparison of the two regimes is necessary to determine the most suitable option for each person.

Things to consider while choosing between both regimes

As per the tax expert, when deliberating between the two tax regimes, it is crucial to consider the following:

>> Available tax exemptions and deductions under both regimes.

>>Comparing the tax liability based on this net taxable income under the old tax regime with that under the new tax regime.

>>Opting for the regime with the lower tax liability.

>>Notify the employer about the choice of regime to ensure the appropriate TDS deduction from the salary.

>> All losses from house property, capital gains, or business & profession, should be taken into account when selecting the regime. Both the current year's losses and the previous year's losses eligible for setoff will expire. Ineligibility to carry forward such losses may affect future income determination and taxes.

Catch the latest stock market updates here. For all other news related to business, politics, tech and auto, visit Zeebiz.com.

DISCLAIMER: The views and investment tips expressed by investment experts on zeebiz.com are their own and not those of the website or its management. zeebiz.com advises users to check with certified experts before taking any investment decisions.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

12:35 PM IST

Zomato gets Rs 803.4 crore tax demand from GST authorities

Zomato gets Rs 803.4 crore tax demand from GST authorities  Income tax refunds jump 46.3% to Rs 3.04 lakh crore in April-November

Income tax refunds jump 46.3% to Rs 3.04 lakh crore in April-November No proposal on income tax relief for senior citizens under consideration: Centre

No proposal on income tax relief for senior citizens under consideration: Centre  Income tax return filer base up 2.2 times in 10 years, 5 times growth in Rs 50 lakh-plus income category: Sources

Income tax return filer base up 2.2 times in 10 years, 5 times growth in Rs 50 lakh-plus income category: Sources  This is India's only tax-free state, residents earn crores without paying Income Tax

This is India's only tax-free state, residents earn crores without paying Income Tax