Income tax returns: Confused about claims from income from house property? What you should know

It is worthwhile to note that when a taxpayer owns more than one property, Income-Tax dept only allows one property to be reported as self occupied, while all others are reported as rented.

Each year taxpayers are busy collecting their bills or income data from different sources to claim tax benefit. Taxpayers have to pay taxes not only on their salary, but also from various other sources of income depending on the various tax rates. Taxes are paid on many sources of income like salary, capital gains or investment in equities, etc. So its a whole new world when you try to claim tax benefits from other income sources, before filing Income Tax Returns (ITR). But did you know, Income Tax Department also gives you an claim or deductions for your income from house property?

Archit Gupta, Founder and CEO - ClearTax said, “ As the name suggests this is usually in the form of rental income, however many taxpayers also report a loss under this head. This is because of the deductions they can claim from this head.”

According to ClearTax, It is worthwhile to note that when a taxpayer owns more than one property, the income tax only allows one property to be reported as self occupied, while all others are reported as rented. This is irrespective of whether or not these are actually rented or vacant.

If they are not rented, a reasonable rent a similar property would fetch is reported and tax paid on it, as if it were actually rented. In such a situation, the deductions listed above for rented property can be claimed.

Here’s a list of claims that you should remember for income from house property, as per ClearTax.

Municipal taxes paid

The amount of municipal taxes actually paid to the Government during the financial year can be deducted if there is rental income.

However, for a property which is self -occupied or is lying vacant, no deduction for municipal taxes can be claimed.

Standard Deduction

Keeping a house functional involves spending money on repairs, maintenance, painting, general upkeep etc. To cover for such expenses, the income tax allows a flat deduction of 30% from rental value less municipal taxes.

Unfortunately, this deduction is only available to rented properties. Note that 30% deduction can be claimed on rented property irrespective of the actual expenses.

Interest on home loan

Several taxpayers take a home loan for buying a property. They are eligible to deduct interest on home loan of maximum Rs 2 lakhs in a financial year. Which means, that for properties which are self occupied property or vacant, this will result in a loss.

Such loss can then be set off from remaining heads of income such as salary and interest income etc. Those who are paying interest on a rented property will make a deduction for municipal taxes, as well as standard deduction and then deduct the interest they pay on home loan.

Do note that for a rented property, even if a taxpayer can claim the entire interest paid as a deduction, the overall loss from house property would be restricted to Rs 2 lakhs only. Remaining loss due to interest can be carried forward to 8 years and can be adjusted against rental income.

Pre-construction interest

Interest paid on home loan is allowed as deduction only from the year in which the construction of the house is complete. Taxpayers who start paying EMIs even before completion of construction can claim pre-construction interest.

The deduction can be claimed in five equal installments starting from the year in which the property is acquired or constructed.

However, the maximum amount eligible for deduction for interest is restricted to Rs 2 lakhs only.

ClearTax explains how usually you end up getting losses in your incomes from house property and how one can set off these losses. Here’s an example.

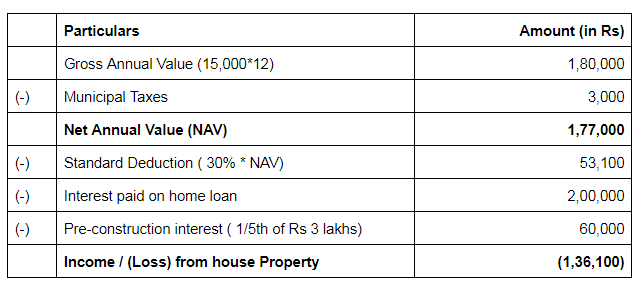

Mr Xavier owns a flat and is currently repaying a home loan - he pays Rs. 4 lakhs annually out of which Rs. 2 lakhs is interest. He has also incurred a pre-construction interest of Rs 3 lakhs. He has let out his flat for a monthly rent of Rs 15,000. He has paid municipal taxes for the FY 2017-18 of Rs 3,000 for this house. His “Income from house Property” calculation will look like this:

This loss can be set off against other heads of income during the year.

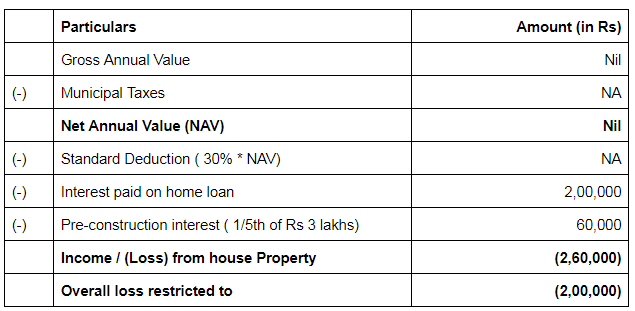

If, in the above example, the flat was not given on rent, the calculation would look like this:

The loss from house property for the FY 2017-18 would be RS 2 lakhs. The remaining loss of Rs 60,000 can be carried forward to future years for set off.

Therefore, in case if you have any confusion in regards to your tax claims or deductions from your income from house property, it is advisable to follow above mentioned instructions.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

05:16 PM IST

ITR Filing: Income tax department targets taxpayers claiming false deductions; sends notices to offenders

ITR Filing: Income tax department targets taxpayers claiming false deductions; sends notices to offenders ITR filing season: How much fine you will have to pay if fails to file ITR by 31 July; know here

ITR filing season: How much fine you will have to pay if fails to file ITR by 31 July; know here Non-taxable income: 5 different types of non-taxable income that can help you to save income tax

Non-taxable income: 5 different types of non-taxable income that can help you to save income tax ITR Filing: Follow these steps if your AIS form is not showing income tax paid while filing income tax return

ITR Filing: Follow these steps if your AIS form is not showing income tax paid while filing income tax return How to reduce tax by 52% using salary perks and NPS

How to reduce tax by 52% using salary perks and NPS