How to become a crorepati: Big EPFO impact! Turn just Rs 66 into MASSIVE Rs 1 crore in wealth

How to become crorepati: An employee can choose to contribute Voluntary Provident Fund or VPF in his EPFO account as it would help him or her garner an additional 0.75 interest more than the PPF investment.

How to become crorepati: Yes, your Employees Provident Fund Organisation (EPFO) account can be fixed to generate a higher amount of money for you than PPF. EPF or Employees' Provident Fund is something that an employee is bound to invest in. The benefit of investment in the EPF is contributory investment by the recruiter and the central government. However, there is another way of enhancing your EPF contribution. An employee can choose to contribute Voluntary Provident Fund or VPF in his EPF as it would help him or her garner an additional 0.75 interest on his or her contribution other than the PF contribution mentioned by the recruiter in the offer letter at the time of recruitment. In the long term, this small number can translate into a huge amount in terms of money in the bank for you. And yes, EPF beats PPF in terms of returns for a number of reasons.

Speaking on the benefit of choosing VPF instead of PPF (Public Provident Fund), Kartik Jhaveri, Manager — Wealth Management at Transcend Consultants said, "To save income tax outgo, people invest in Public Provident Fund as it gives an assured return which is currently t 7.9 per cent. However, there is one other EPF provision, which is called VPF, where a salaried individual can choose to enhance his or her EPF contribution on his or her own. If they do so, they will be able to get 8.65 per cent interest on his or her VPF investment along with the Section 80C tax exemption under the Income Tax Act." However, Kartik maintained that in VPF, the earning individual won't get the benefit of the recruiter's contribution.

See Zee Business Live TV streaming below:

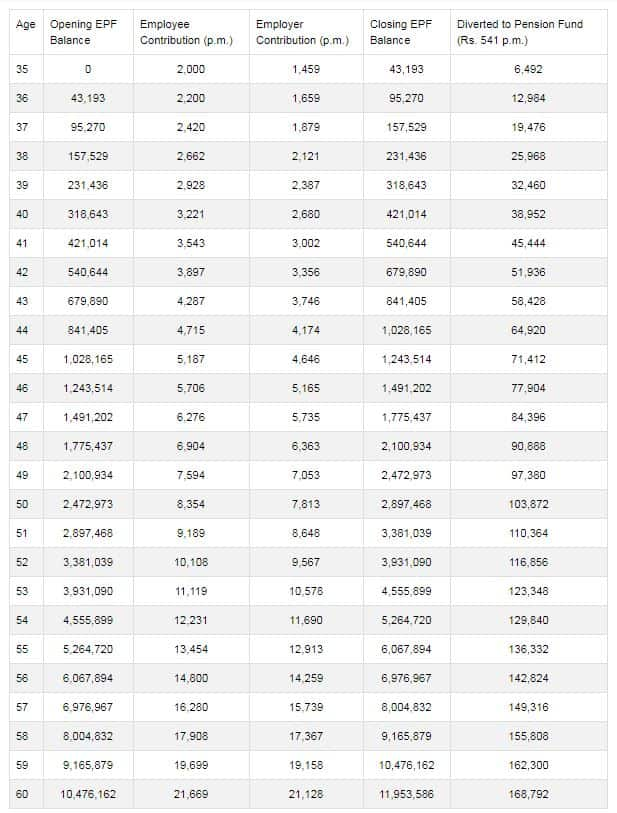

Check EPF-VPF calculator below:

Source: EPF Calculator

Source: EPF Calculator

So, VPF can be a good option to accumulate retirement funds. For example, let's take Rs 2,000 per month in the VPF. Also, a person would work at least 25 years and hence contribute for that long in the VPF. Means, he or she will be saving around Rs 66.66 per day to invest Rs 2000 per month in the VPF with 10 per cent top-up per annum. The EPF calculator suggests that after 25 years of contribution in the VPF, his or her closing EPF balance due to this VPF would be Rs 1,19,53,586 or Rs 1.19 crore.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

03:39 PM IST

Wealth Guide: Want to become real rich by investing early in residential real estate? Expert suggests these tips

Wealth Guide: Want to become real rich by investing early in residential real estate? Expert suggests these tips  Investing or want to invest in Mutual Funds to become rich? These 5 myths may shatter your dream - Beware of them!

Investing or want to invest in Mutual Funds to become rich? These 5 myths may shatter your dream - Beware of them! Crorepati Calculator: This mutual fund SIP trick will help you get more than double maturity amount — here is how

Crorepati Calculator: This mutual fund SIP trick will help you get more than double maturity amount — here is how account can make you rich in long-term! Follow this expert's tips") Crorepati Calculator: Your Public Provident Fund (PF) account can make you rich in long-term! Follow this expert's tips

Crorepati Calculator: Your Public Provident Fund (PF) account can make you rich in long-term! Follow this expert's tips Crorepati Calculator: Turn your Rs 200 per day savings into Rs 1 cr plus Rs 33,963 monthly pension; here is Money making tip

Crorepati Calculator: Turn your Rs 200 per day savings into Rs 1 cr plus Rs 33,963 monthly pension; here is Money making tip