Bank of Baroda MCLR cut: When your bank trims lending rates, this is how your home, car, personal loans EMI is calculated

When a bank follows a cut in lending rates benchmark, one can surely expect their EMIs on home loan, personal loan and vehicle loan to get cheaper.

The good news of RBI’s policy repo rate cut by another 25 basis points, is now evident among banks and borrowers. At first it was state-owned SBI who trim down home loan lending rates, and later another largest PSB namely Punjab National Bank (PNB) cut its MCLR rates, and now 110-years old Bank of Baroda (BoB) has made its move. Just like PNB, BoB has also cut its marginal cost of funds based lending rate (MCLR) by 10 basis points. When a bank follows a cut in lending rates benchmark, one can surely expect their EMIs on home loan, personal loan and vehicle loan to get cheaper. However, not many are aware how exactly MCLR plays a role in their retail loans. Let’s find out!

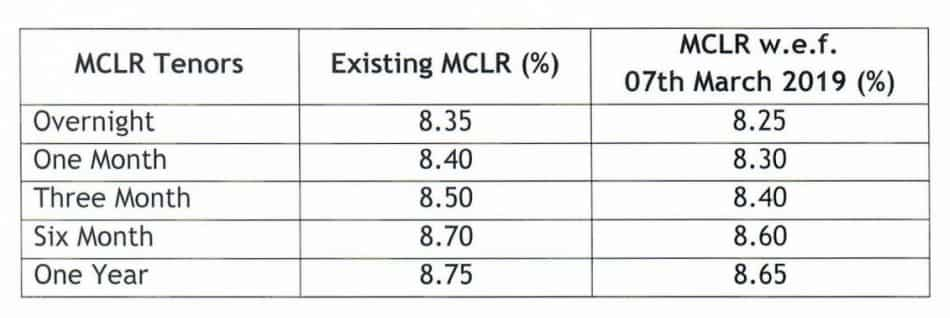

At BoB, MCLR for overnight tenor now stand at 8.25% from previous 8.35%, while for one month, three month and six month tenor, this lending rate will be at 8.30%, 8.40% and 8.60% from previous 8.40%, 8.50% and 8.70% respectively. Meantime, MCLR for one year tenor will stand at 8.65% compared to previous 8.75%. The new rates of BoB will come in effect from March 07, 2019 onwards.

When a bank cuts MCLR, this is how loan rates are calculated!

In simple words, MCLR is used as an internal benchmark or reference rate for a bank, where the lender is not allowed to lend money to borrowers below this benchmark rate. Hence, MCLR is used as an hierarchy while deciding home loan, personal loan and car loan interest rates.

While deciding the actual loan interest rate, a bank adds the components of spread to the MCLR. Every month, a bank resets the MCLR rate either by increasing or cutting or keeping it unchanged. However, whatever be the MCLR, it is the spread decided for a loan that will reflect in your EMIs. Take note, a floating rate for loans is offered at a spread over the benchmark.

#CorporateRadar | देखिए मेटल सेक्टर की दिग्गज कंपनी हिंदुस्तान कॉपर के चेयरमैन और मैनेजिंग डायरेक्टर संतोष शर्मा की खास बातचीत।

पूरा इंटरव्यू देखें: https://t.co/1EcPs4cAOY@copper_ltd @poojat_0211 pic.twitter.com/C33qqBA4NL

— Zee Business (@ZeeBusiness) March 6, 2019

Thereby, a bank cannot lend below the MCLR at the aabove-prescribedmaturity, for all loans must be linked with this standard.

Furthermore, even if let’s suppose your spread on loan is kept unchanged by the bank, however, the fact that MCLR has been brought down as per guidelines must reflect in your interesting rates. This will make EMIs cheaper so to believe!

Notably, MCLR rate cuts are more beneficial when policy repo rates are also in similar trend which is currently the case, because then banks will no longer have the need to not keep loan interest rate higher or unchanged. Just like borrowers, even banks borrow from RBI and policy repo rate is that interest rate they must pay, if this becomes cheap for banks they are better positioned to keep lending rates lower as well. Hence, the citizens who opt for loan benefit as well.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

01:28 PM IST

Bank of Baroda Recruitment 2025: Apply now for 4,000 apprentice vacancies—Check eligibility, stipend, and how to apply

Bank of Baroda Recruitment 2025: Apply now for 4,000 apprentice vacancies—Check eligibility, stipend, and how to apply  Budget 2025: Top PSU stocks to watch for investment opportunities

Budget 2025: Top PSU stocks to watch for investment opportunities CPI inflation likely to moderate to 5% in December from 5.5% in November: BoB report

CPI inflation likely to moderate to 5% in December from 5.5% in November: BoB report India likely to attract $20-25 billion FPI inflows in FY25, recent outflow temporary: Bank of Baroda

India likely to attract $20-25 billion FPI inflows in FY25, recent outflow temporary: Bank of Baroda NBCC arm gets Rs 65 crore work order in Bengaluru from Bank of Baroda

NBCC arm gets Rs 65 crore work order in Bengaluru from Bank of Baroda