Escorts Kubota hits new life high on robust growth prospect; brokerages divided

The auto and ancillary company’s management during the investors' virtual meeting reiterated its robust medium-term growth prospects.

Escorts Kubota share price touched an all-time high level of Rs 2,206.15 per share, after surging by over 8.5 per cent on the BSE intraday during Monday’s trading session. The stock surged mainly on the strong outlook of the company, announced by the management during an analysts' call.

The auto and ancillary company’s management during the investors' virtual meeting reiterated its robust medium-term growth prospects. The stock on Monday closed over 7.5 per share to Rs 2186 apiece, it has jumped nearly 22 per cent in the last one year and more than 34 per cent in the last six months.

Brokerages YES Securities and Motilal Oswal in their reports said that on the financial front by the financial year 2027-28 (FY28), the management expects that the revenues of the combined entity to grow 2.5 times of which exports contribution to increase to 15‐20 per cent and EBITDA to be increased to mid‐teens with ROCE/ROE increase to 23‐30 and 18 per cent.

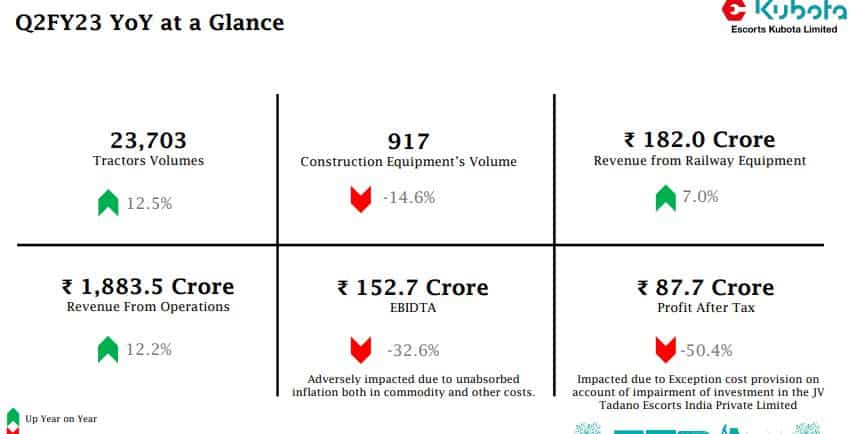

Image Source: Escorts Investor Presentation

The company’s focus would revolve around growing market share in India through new product launches; attaining leadership position in exports and continuing with the ramp-up of other businesses while improving profitability, the management said.

Despite the promising outlook laid out by the company’s management, several domestic brokerages are divided on Escorts Kubota between Buy and Neutral rating.

YES Securities raise FY24/25 EPS estimates by 2/6 per cent to factoring contribution from parts and engine verticals. However, it expects major benefits of new business opportunities such as spares and engines to start from FY25E.

Image Source: Escorts Investor Presentation

The brokerage said, “Significant ramp‐up in parts sourcing by Kubota global is key upside risk to our estimates. We build in revenue/EBITDA/PAT CAGR of 14/19/20 per cent respectively over FY23‐25E and upgrade the stock to Neutral with a lower target price of Rs 1,911 per share.”

While the mid-term growth strategy seems to be in the right direction, we would watch for its effective execution, Motilal Oswal said in a report on the company.

The brokerage said, “While the tractor cycle seems to be uncertain, the valuations are already reflecting volume recovery as well as the benefit of the Kubota partnership. We reiterate a Neutral rating with a target of Rs 1,875 apiece.”

Image Source: Stockedge

On the other hand, ICICI Securities retain a Buy rating amid wider opportunity at play with Kubota coming on board as a co-promoter and strong financials on healthy RoCE targets. It values Escorts Kubota at 25x P/E on core FY24E EPS with a target price of Rs 2,365 per share.

The brokerage was impressed with the cultural shift in the company, which Escorts Kubota is seeing imbibing the best practices. Incorporating the positives, it expects sales to grow at a CAGR of 14.4 per cent over FY22-24E, with consequent operating margins seen at 12 per cent by FY24.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

04:09 PM IST

Expect tractor industry festive season sales to grow 8-10% this year: Escorts Kubota CFO

Expect tractor industry festive season sales to grow 8-10% this year: Escorts Kubota CFO Escorts Kubota to hike tractor prices from May 1

Escorts Kubota to hike tractor prices from May 1 Should you buy, sell or hold Dr Reddy’s, L&T, Godrej Consumer, Gujarat Gas, other stocks today?

Should you buy, sell or hold Dr Reddy’s, L&T, Godrej Consumer, Gujarat Gas, other stocks today? Q3 Results 2023: Samvardhana Motherson, Pennar, Escorts Kubota, Symphony declare December quarter results - HIGHLIGHTS

Q3 Results 2023: Samvardhana Motherson, Pennar, Escorts Kubota, Symphony declare December quarter results - HIGHLIGHTS Traders Diary on 20 stocks: Buy, Sell or Hold strategy on Federal Bank, SBI Life, CONCOR, Escorts Kubota, others

Traders Diary on 20 stocks: Buy, Sell or Hold strategy on Federal Bank, SBI Life, CONCOR, Escorts Kubota, others