Dalal Street Voice: Dhaval Kapadia of Morningstar gives asset allocation tips to investors with 10 years of horizon

Dhaval Kapadia has more than 23 years of experience in areas including fixed income, equity markets and investment advisory.

Dhaval Kapadia, Director- Managed Portfolios, Morningstar Investment Advisor India said that assuming a horizon of 10+ years, one could look to invest with a portfolio mix of about 80-85% into equities (Large/Mid/Small-cap/International – 50/10/5/20) and 15% into fixed-income funds.

Kapadia has more than 23 years of experience in areas including fixed income, equity markets and investment advisory. Prior to joining Morningstar in 2014, he spent nearly six years at Axis Bank, leading a team of Investment Advisors, which were a part of the Wealth Management & Private Banking businesses.

In an interview with Zeebiz's Kshitij Anand, Kapadia said one could also look to have about 5-10% exposure to gold, from a diversification perspective as gold has a low correlation with other asset classes and is seen as a safe-haven asset in times of global risk-off sentiment. Edited excerpts:

Q) What does the BJP win in 4 states mean for markets, economy and reforms?

A) Market participants could perceive this as a pre-cursor to the general elections in 2024. Continuity in government and the presence of the ruling party at the state level is viewed as positive in executing government schemes efficiently and pushing through reforms at the ground level, which could support economic growth.

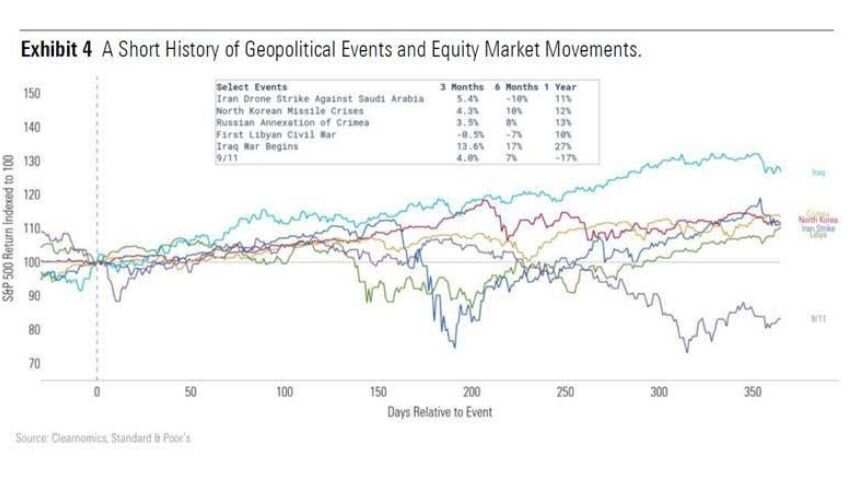

Q) The war-like scenario must have wiped out a good 5-10% of investor portfolio in a matter of weeks. What advice would you like to give to investors? Should one stay put, add on dips or cash out – what does the history suggest?

A) A look at the history of geopolitical events since 2000, indicates that equity markets (represented by S&P 500 below) have generally recovered any losses over the subsequent 1-year period (except for the US terrorist attacks in 2001).

Hence, it would be advisable for investors to stay put. A look at the historical index growth of the broader equity market index (S&P BSE 500) shows that markets have scaled higher peaks through time responding to drivers such as inflation, earnings growth, and change in valuations.

Over long horizons (10+ years), equities can be expected to deliver around 4-5% over the long-run inflation rate.

Withdrawing any corpus would lower your portfolio value to the extent of the amount withdrawn and you might lose out on any subsequent gains on the withdrawn corpus that would have accrued till the end of your investment horizon. The withdrawals defeat the purpose of investing which is to generate wealth.

Investors should stick to their long-term strategic asset-allocation which in turn depends on their risk appetite (ability and willingness to take risk) and not try and time the markets.

You can consider re-balancing your asset allocation back to your recommended long-term asset allocation in case of any material drift due to the recent market correction.

Any sharp correction in the market in response to short-term events should be seen as an opportunity to buy into the market, after weighing in any potential impact of the event on the long-run return drivers.

Q) If someone plans to put in Rs 10L after the recent double-digit fall seen in benchmark indices from 52-week highs. What is the right asset allocation strategy considering someone is in the age bracket of 30-45 years of age? Also, should one do lump sum or STP?

A) Investors should ideally follow an asset allocation-based approach (mix of equity, debt, commodities, real estate, etc.) for investing towards one’s goal.

While fixed-income lends stability to the portfolio, equities play a crucial role in wealth generation over the long run with the potential to deliver superior inflation-adjusted returns compared to fixed-income.

Valuations play a crucial role while determining exposure to any asset class /security. Lower (cheaper) valuations reduce the risk of high future capital loss and improve upside potential, and vice-versa.

· The allocation to equities should be a function of your risk profile and investment horizon as related to your goal. Investors should stick to their strategic asset allocation (SAA) which in turn depends on their risk appetite (ability and willingness to take risk) and not try and time the markets. Higher the investment horizon and risk appetite, higher can be the allocation to equities.

· Assuming a horizon of 10+ years, one could look to invest with a portfolio mix of about 80-85% into equities (Large/Mid/Small-cap/International – 50/10/5/20) and 15% into fixed-income funds. The international equity allocation offers diversification across geographies and also acts as a hedge against rupee depreciation. For investment in fixed-income, you can consider fixed income funds with a high (safer) credit quality portfolios such as Banking & PSU debt funds and Medium to long term funds. One could also look to have about 5-10% exposure to gold, from a diversification perspective as gold has a low correlation with other asset classes and is seen as a safe-haven asset in times of global risk-off sentiment.

· Volatile asset classes (equity, gold) witness sharp cycles with both strong up-move phases and down-move phases. Given their cyclical nature and high volatility, it is advisable to invest in a staggered manner, via the SIP or STP route.

A SIP/STP facilitates regular investments at periodic intervals, enabling an investor to average out the cost of his investments. This benefits investors in falling markets since they would be buying units at cheaper prices. The STP duration could be around 6-12months given that the volatility may be short-term in nature.

See Zee Business Live TV Streaming Below:

Q) With interest rates likely to head North – what is the right strategy for MF investors? Should they look at tweaking their asset allocation?

A) Since 2019, the RBI has cut the policy rate sharply (250 bps) and announced a slew of measures to support the slowdown in the economy. These measures along with abundant liquidity in the banking system resulted in yields falling across the yield curve, particularly at the shorter end leading to a steepening of the yield curve.

Currently, the medium-end of the curve (4 to 7-year segment) offers an attractive yield pick-up relative to the shorter end (1 to 3 year segment) of the curve. Hence, from a risk-reward perspective the medium-term segment looks attractive. In the YTD period, the yield curve has seen an upward shift to some extent reacting to rising global bond yields amid the global economic recovery and inflationary pressures, and more recently on account of steep rise in crude oil prices.

Corporate bond spreads have narrowed significantly compared to their long-term averages (particularly for the AAA-rated segment); so subsequent widening of spreads could present additional downside risk to investors. Hence, funds with high exposure to G-secs look more suitable than corporate bond funds at this juncture.

For those investing for a reasonably long horizon (more than 5 years), one could follow a core and satellite approach for the fixed-income portion of the portfolio.

The core allocation (75-80%) should be invested into shorter duration high credit quality accrual funds (short-duration, floating-rate and medium duration funds) and the rest (~20-25%) to longer duration funds such as Medium-to-long term and Dynamic Bond Funds.

One could consider target maturity funds (investing in Government securities with 5-10 years maturities) having a maturity date close to their investment horizon.

These entail minimal interest rate risk if held to maturity and also have a low expense. Investors should evaluate the suitability of the above recommendations with their risk appetite in perspective.

Q) Retail investors reaffirmed their faith in equities amid volatility (geopolitical towards later part of the month) as equity funds saw a net increase of more than Rs 19000 cr in Feb. What is your view and do you think this war-like scenario could result in a slowdown in the flows?

A) Equity mutual funds have witnessed robust inflows (Rs 1.56 Tn cumulative) over the past year, as markets scaling record highs since the lows of March 2020 has piqued investor asset in equities as an asset class – also evident by the record rise in the number of Demat accounts relative to pre-pandemic levels.

A sizeable SIP book (industry level) has also helped in getting decent flows into funds, despite higher volatility in markets since November on concerns of tightening by major global central banks and the recent geopolitical tensions between Russia and Ukraine.

A sharp recovery in corporate earnings amid a pick-up in economic activity has trimmed down valuations that seemed pricey a few months ago, improving attractiveness for the asset class.

Markets have witnessed a drawdown of ~13% (S&P BSE 500) in the YTD period but have since quickly regained some ground (up 5% from March 07 till March 11).

Investors would also be cognizant of the sharp surge in equity markets since the lows witnessed at the outset of the pandemic.

Hence, flows could continue unless Russia -Ukraine tensions flare up raising concerns around global growth amid high commodity prices and faster tightening by the U.S. Fed to tame inflation.

Q) Crude above $100 – what is the kind of impact you foresee on markets, economy and India Inc. in upcoming quarters?

A) India imports over 70-80% of its crude oil requirement. Crude prices at the current high levels would weigh on India’s import bill widening the trade deficit which in turn would weigh on the rupee.

High crude oil prices could translate into an increase in fuel prices (petrol, diesel) along with the second order effect of an increase in raw material & transportation costs feeding into the price of most goods and services leading to higher inflation, which could impact demand and hurt economic growth.

Higher inflation would also lower the profit margins of India Inc. leading to depressed earnings, and result in higher valuations for equities which may correct to account for the same.

Higher inflation may also warrant faster monetary tightening by the RBI and lead to increased bond yields, which would impact borrowing costs in the economy and thereby impact demand.

Of course, the RBI would also consider the impact of higher inflation & global uncertainties on trade & broader economic growth prior to raising interest rates.

Q) Gold recently became buyers’ favourite – what should be your strategy in case someone plans to put fresh money in the yellow metal? Should they buy physical Gold or digital and why?

A) Gold plays an important role as a diversifier in a portfolio due to its low correlation with other asset classes and is seen as a safe-haven asset in times of global risk-off sentiment. It is seen as a store of wealth and as a hedge against inflation and currency depreciation.

Gold’s importance as a diversifier has been re-instated during the COVID-19 pandemic led sell-off in markets in February-March 2020, as it witnessed a drawdown of only ~11% in INR terms (S&P GSCI Gold Spot index) compared to ~38% drawdown by domestic equities (S&P BSE 500 TR Index).

From an asset-allocation standpoint, it is advisable to have some allocation to gold (~5-10%) for diversification benefits.

Like in other volatile assets, it is advisable to build exposure to gold in a staggered manner to benefit from rupee cost averaging. This benefits investors in falling markets since they would be buying units at cheaper prices.

Digital vs Physical Gold

Digital gold is a virtual method of investing in gold, without having to physically hold the gold and can be purchased for as low as Rs 1. Digital gold purchased is 24k gold and the buyer is assured of purity as it is certified by licensed agencies.

It is stored in insured vaults by the seller on behalf of the buyer. Digital gold can be sold online or buyers can even exchange it and take delivery of physical gold.

Physical gold, on the other hand, is usually mostly for jewellery and is typically not considered an investment option. It entails costs such as making charges, storage costs etc, adding to the investment cost.

Moreover, holding gold in its physical form at home is fraught with risks. Physical gold is typically purchased in multiples of 1 gram, while digital gold can be accumulated in much lower denominations.

(Disclaimer: The views/suggestions/advices expressed here in this article is solely by investment experts. Zee Business suggests its readers to consult with their investment advisers before making any financial decision.)

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

10:17 AM IST

Women's Day Special: 'Stronger women build stronger nations' - Women in Indian Mutual Fund Industry

Women's Day Special: 'Stronger women build stronger nations' - Women in Indian Mutual Fund Industry Open-ended domestic funds' AUM sees 43% jump yoy; SBI Mutual Fund attracts highest net inflows of Rs 39,282 cr in September quarter

Open-ended domestic funds' AUM sees 43% jump yoy; SBI Mutual Fund attracts highest net inflows of Rs 39,282 cr in September quarter