Notes ban likely to impact cashless economy, bonds: India Ratings

The government's recent ban on circulation of Rs 500 and Rs 1,000 currency notes is likely to impact various sectors right from cashless economy to growth of India's economic growth to financials of payments banks and banks, among others, said India Ratings and Research (Ind-Ra).

Prime Minister Narendra Modi in a surprise move this week announced to ban circulation of Rs 500 and Rs 1,000 notes from midnight of November 8 in an attempt to crack down black money and corruption.

According to India Ratings, the latest move has come after the disappointing collections made under the Income Disclosure Scheme (IDS), which gave the option to disclose unaccounted money.

Here are the sectors that India Ratings and Research (Ind-Ra) believes the government's latest move will be felt with differing intensities and for a different period of time:

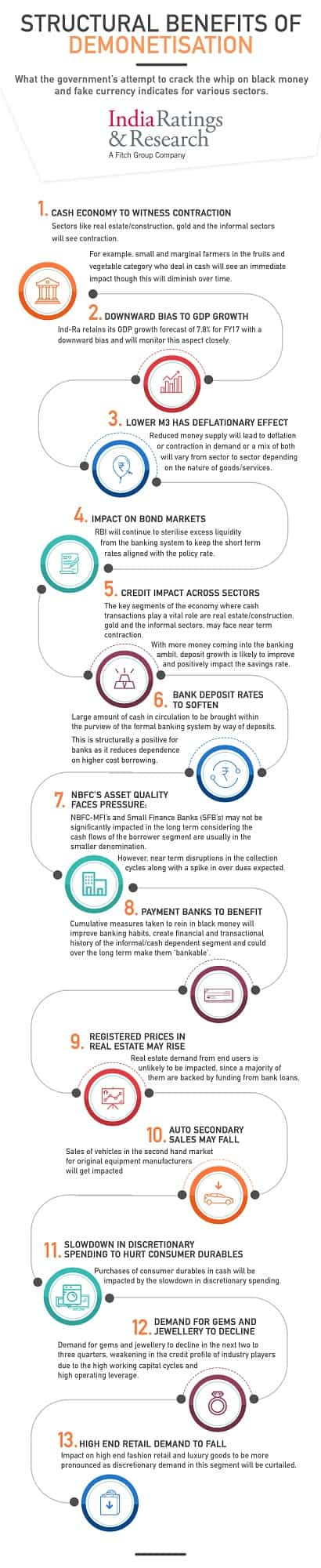

1. Cash Economy To Witness Contraction:

The currency of the aforesaid denominations constitutes around 86% of the total value of the currency in circulation, thus its impact on the cash economy will be significant. The key segments of the economy where cash transactions play a vital role are real estate and construction, gold and the informal sectors. For example, small and marginal farmers in the fruits and vegetable category typically require off-loading of their produce in the local Mandi in cash and could see an immediate impact.

2. Downward Bias to GDP Growth:

The sudden decline in money supply and simultaneous increase in bank deposits is going to adversely impact consumption demand in the economy in the short term. Ind-Ra retains its GDP growth forecast of 7.8% for fiscal year 2016-17 (FY17) with a downward bias and will monitor this aspect closely.

3. Lower M3 has Deflationary Effect:

Reduction in money supply can also have a deflationary effect in the economy. However, whether the impact of the reduced money supply will lead to deflation or contraction in demand or a mix of both will vary from sector to sector depending on the nature of goods/services.

4. Impact on Bond Markets:

Surge in deposits will create more demand for government bonds and other high rated bonds in a situation of tepid demand for credit, leading to lower bond yields especially in the shorter end of the curve.

Ind-Ra believes the RBI will continue to sterilise excess liquidity from the banking system to keep the short term rates aligned with the policy rate.

5. Credit Impact across Sectors:

Impact of this policy measure will flow to the economy mainly through the real estate/construction sector, which has strong linkages with sectors such as cement and steel and they will turn credit negative in the short-run. The key segments of the economy where cash transactions play a vital role are real estate/construction, gold and the informal sectors, which may face near term contraction.

With more money coming into the banking ambit, deposit growth is likely to improve and positively impact the savings rate.

6. Bank Deposit Rates to Soften:

Ind-Ra expects a large amount of cash in circulation to be brought within the purview of the formal banking system by way of deposits. This is structurally a positive for banks as part of this cash gets deposited as current account and savings account (CASA) deposits, reducing banks dependence on higher cost borrowing.

7. NBFC’s Asset Quality Faces Pressure:

Ind-Ra believes asset quality of retail asset financers, especially non-banking financial companies (NBFCs), which have developed expertise in the credit assessment of the informal segment and have built models around it to come under pressure in the short-term. NBFC-MFI’s and Small Finance Banks (SFBs) may not be significantly impacted in the long-term considering the cash flows of the borrower segment are usually in the smaller denomination.

However, there could be near term disruptions in the collection cycles along with a spike in over dues, which could put their liquidity strength and the disbursal cycle under pressure.

8. Payment Banks to Benefit:

Payment banks and others entities which are part of the transaction ecosystem are likely to be long-term beneficiaries, as more and more cash finds its way into the formal banking channels.

Ind-Ra believes the cumulative measures taken to rein in black money will improve banking habits, create financial and transactional history of the informal and cash dependent segment and could over the long term make them ‘bankable’.

10. Registered Prices in Real Estate May Rise:

The real estate demand from end users is unlikely to be impacted, since a majority of them are backed by funding from bank loans. Demand from investors for real estate however may come down since in some cases investors prefer cash transactions. Ind-Ra expects the supply of real estate in the secondary market, which is strongly rumoured to have a large cash component involved, to suffer in the short term, which may in turn improve demand for residential real estate in the primary market.

10. Auto Secondary Sales May Fall:

Sales of vehicles in the second hand market for original equipment manufacturers will get impacted, which will have a ripple effect on OEM sales, as buyers will not be able to dispose of their old vehicles easily.

11. Slowdown in Discretionary Spending to Hurt Consumer Durables:

To have moderate to negative impact in the short-term, since purchases of consumer durables in cash will be impacted by the slowdown in discretionary spending.

12. Demand for Gems and Jewellery to Decline:

Ind-Ra expects the demand for gems and jewellery to decline in the next two to three quarters. This would result in weakening in the credit profile of industry players due to the high working capital cycles and high operating leverage. The unorganised segment will be hit particularly hard given the large proportion of unaccounted inventory and high proportion of cash sales. Over the medium-term the organised industry players will benefit at the cost of the unorganised players.

13. High End Retail Demand to Fall:

The ratings agency expects the impact on high end fashion retail and luxury goods to be more pronounced as discretionary demand in this segment will be curtailed. In case of Quick Service Restaurants, although 60% to 70% of the transactions are currently in cash, the impact is likely to be moderate due to the low ticket size of purchases and high likelihood of patrons adapting to plastic money.

Ind-Ra projects demand across the retail sub-segments to shift to the organised segment over the medium term.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

04:38 PM IST

India abolishes larger banknotes in fight against graft, 'black money'

India abolishes larger banknotes in fight against graft, 'black money' PM Modi's black money stroke: Should you worry for your MF, stock investments?

PM Modi's black money stroke: Should you worry for your MF, stock investments? 9 steps you must take to exchange your old Rs 500, Rs 1,000 notes

9 steps you must take to exchange your old Rs 500, Rs 1,000 notes Notes Exchange Facility: Here are key things you should know

Notes Exchange Facility: Here are key things you should know  RBI issues new series of Rs 500, Rs 2,000 currency notes

RBI issues new series of Rs 500, Rs 2,000 currency notes