Here's how banks can save themselves from NPA stress

Bad loans are one of the reasons why banks are currently suffering through higher provisions, deterioration in asset quality, higher slippages and thus lower earnings.

Viral Acharya, Deputy Governor, Reserve Bank of India (RBI) recently spoke about banks' capital needs to solve bad loans problem.

Bad loans are one of the reasons why banks are currently suffering through higher provisions, deterioration in asset quality, higher slippages and thus lower earnings.

Recently, a Global Financial Stability Report released by the International Monetary Fund (IMF) highlighted that Indian banking sector comes out as worse-off compared to other emerging economies in terms of little bank capital that it has set aside to provision for losses on its assets.

In this context, Acharya said, “ We keep hearing clarion calls for more and more government funding for recapitalisation of our public sector banks. Clearly, more recapitalisation with government funds is essential. However, as a majority shareholder of public sector banks, the government runs the risk of ending up paying for it all.”

Acharya added, “The expectation of government dole outs might have been set by the past practice of throwing more money after the bad. Take for instance our bank recapitalisation plan of 2008-09 after the global financial crisis: banks that experienced the worst outcomes received the most capital in a relative sense. Most of these banks need capital again.”

While the central bank has been taking various measures like recent PCA framework and standard assets provisioning (SAP) method, yet many analysts believe, RBI cannot do it alone to tackle the bad loans problem.

Fitch Ratings said, “RBI will not be able to address problems in the banking sector on its own. Significant efforts to resolve bad loans, for example, would leave banks in need of recapitalisation, given that haircuts and increased provisions would be required. State banks are generally in a poor position to raise new capital, which makes them largely reliant on the government for recapitalisation.”

Now what has been done cannot be undo, but Indian banks can still save themselves from these bad loans distress in future by taking into account below mentioned factors.

Acharya in his study report called 'A Bank Should Be Something One Can “Bank” Upon' explained few measures.

Private Capital Raising: PSBs can still raise private capital in order to share the government's burden of recapitalising, as this brings in discipline and gets bank shareholders, boards and management to more seriously care about the quality of lending decisions.

Asset Sales: Not all assets or loan portfolios can be bad those who are in good shape can be sold in the market. Bank's also hold non-core assets such as insurance subsidiaries, market-making divisions, foreign branches, etc. Such non-core assets can be readily sold.

Divestments: As per Acharya, this move would overall improve banking sector health, creating an an opportune time for the government to divest some of its ownership of the restructured banks. It would reduce the overall amount the government that need for bank capital and help preserve fiscal discipline, along with stable inflation outlook.

To address the extant bad loans problem and to avoid the repeat failures, Kotak Institutional Equities also chalked down few measures.

Conversion of debt to equity in power sector and steel sectors:

Sanjeev Prasad, Sunita Baldawa and Anindya Bhowmik analysts of Kotak said, “Conversion of debt into equity in the above mentioned sector will benefit bank in three ways. These are - banks will not suffer a permanent diminution in the value of their loans if the assets are operational and viable, while they can also participate in any upside in the value of equity and lastly they can sell the equity investment at larger stage."

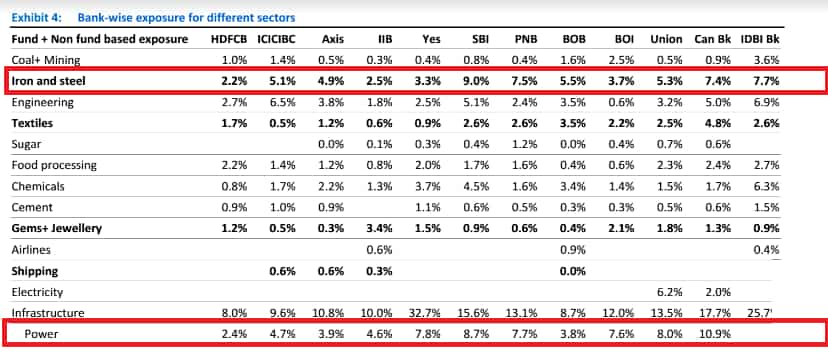

Bank-wise fund and non-fund based exposure in steel sector has been between 2% - 9% whereas in power sector it has been between 2% - 11%.

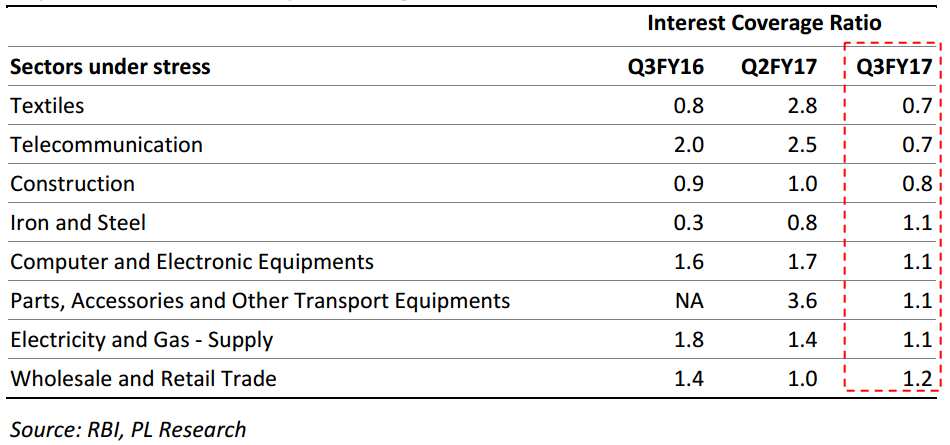

R Sreesankar, Pritesh Bumb and Vidhi Shah of Prabhudas Lilladher said, “Sector like textile, construction and iron & steel could also need SAP as they remain vulnerable with lower interest coverage ratio.”

Demand for steel and power sector is good ahead and hence a conversion of debt into equity could support bank to improve their asset quality.

The trio at Kotak said, “We expect overall demand for power to increase over time but state governments can boost consumption of power through ‘right’ pricing for household and industrial consumers. While for Indian steel we expect capacity utilisation to improve to around 90% by FY2020. Nonetheless, 30-40% haircut to loans may be required to improve the viability of certain steel assets.”

Government Committee:

Without formal support of government, public banks are mostly reluctant to execute any resolution scheme that entails 30-50% write-down of loans to large private companies.

Thus Kotak guides for a temporary government committee should be sufficiently empowered to take decisions on the nature of resolution for each stressed asset above a certain size Rs 2,500 crore.

These committee's can draw on the inputs of 2-3 independent agencies (rating agencies and valuation agencies) on (1) the ‘right’ capital structure of the company in the cases where debt will be converted into equity and/or (2) the ‘right’ level of debt that can be serviced by the cash flows of the company," added Kotak.

Indian Accounting Standard:

The new Ind-AS accounting standard for banks applicable from April 1, 2018 may dramatically alter the provisioning for NPAs. Banks may no longer have the luxury of making incremental provisions over time after a credit default, which the current mechanism of asset classification and provisioning allows.

Moreover, Acharya and many analysts believe PCA framework and consolidation of banks as another positive move to tackle bad loans.

As per the Economic Survey, gross NPAs climbed to almost 12% of gross advances for public sector banks at end-September 2016.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

03:22 PM IST

Viral Acharya's resignation: RBI union moots collegium of experts to select governors, deputy governors

Viral Acharya's resignation: RBI union moots collegium of experts to select governors, deputy governors Why RBI deputy governor Viral Acharya resigned: Here's official RBI response

Why RBI deputy governor Viral Acharya resigned: Here's official RBI response RBI deputy governor Viral Acharya resigns, may return to the US: Sources

RBI deputy governor Viral Acharya resigns, may return to the US: Sources Urjit Patel quits in shock move! Viral Acharya next?

Urjit Patel quits in shock move! Viral Acharya next? RBI vs Centre: Urjit Patel in spotlight, markets on watch

RBI vs Centre: Urjit Patel in spotlight, markets on watch