Net interest margins to be a new pain point for banks?

Sumeet Kariwala, Anil Agarwal, Subramanian Iyer and Rahul Gupta of Morgan Stanley, in a report dated November 3, 2016 said that banks are going through NIM pressure due to lending rate cuts, lower interest rates and rising NPLs.

There was a time where Indian banks had only problem of rising non-performing loans (NPL). However, the conversation has now shifted to net interest margins (NIM).

Sumeet Kariwala, Anil Agarwal, Subramanian Iyer and Rahul Gupta of Morgan Stanley, in a report dated November 3, 2016 said that banks are going through NIM pressure due to lending rate cuts, lower interest rates and rising NPLs.

NIM are the measure of difference between the interest income generated by bank and the amount of interest paid out to their lenders like deposits, relative to the amount of their (interest-earning) assets.

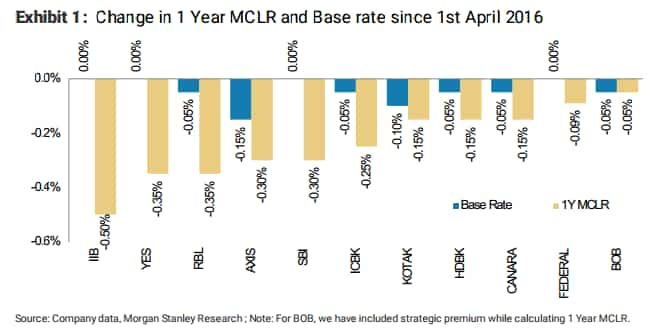

The marginal cost of funds-based lending rate (MCLR) was enacted by RBI on April 1st 2016 – a move to make rate transmission efficient. Following, banks have been trimming MCLR as deposit rates decline.

As MCLR is applied to new borrowers, large amounts of loan is still attached to base rate.

They said, “The base rate (which was retained for old lending) has been relatively sticky, implying no rate pass-through for earlier borrowers. There are differences in formula that are likely driving this, but it affects NIMs.”

With majority of loan book on old base rate, resulted in yields on the entire loan book though revisions have been made in the front book.

“Yet as time passes and more loans are MCLR-denominated, a meaningful pressure on NIMs will be seen. While some of this will likely be mitigated by lower funding costs, it will still hurt NIMs in FY17 and FY18, we believe,” said the trio.

Recently, banks like State Bank of India, HDFC bank and ICICI Bank has made cut in interest rate for home loan borrowers by 15 basis points, making borrowing cheaper.

Another problem was continuous lowering of interest rate among Indian banks which has mounted reinvestment risk.

“Given the relatively long duration on bonds that banks hold, rate declines take time to feed through earnings. However,as we have seen in previous (sustained) rate-cut cycles, this builds up over time and acts as a big drag on NIMs,” said Morgan Stanley.

Reinvestment risk usually arises from the payment of principal and interest, when a bond is reinvested at a lower rate than the original investment. It is expected to be even higher if any banks book material capital gains on bonds.

However, Morgan Stanley believes this will support earnings for one year, the bank would have to reinvest in lower-yielding bonds almost immediately.

Meanwhile with no signs of relief in NPLs in near time, revival in NIM looks far away.

What is the relation between NPL and NIM?

Usually if NPL formation slows, NIMs bounces back.

“Lower net NPLs would help, as that would imply that a larger chunk of assets are earning interest income,” they added.

As per Reserve Bank of India's (RBI) data, the NPLs have crossed $138 billion (approx Rs 8,71,746 crore) in June 2016, an increase of 15% in just six months.

Morgan Stanley expects net NPLs to decline in the system, but sees the quantum of decline probably slower ,especially at public sector banks, given the lack of profitability to provide for bad loans quickly.

On the other hand higher loan-to-deposit (LD) ratio could be a driving factor for NIM. But yet bank will need adequate capital for this.

Lastly, banks may shift their loan mix towards higher-yielding assets which carry higher risk weights, said analysts at Morgan Stanley.

Once again, private banks will not bare majority of NIM burden just like NPLs compared to PSBs.

The report said,"Private banks should be able to slow the pace of NIM compression. For PSBs, which are already facing significant NIM compression, it is tough to see how NIMs expand against this backdrop."

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

02:57 PM IST

Bank of Baroda raises MCLR on select tenor loans by up to 15 basis points

Bank of Baroda raises MCLR on select tenor loans by up to 15 basis points Facing margin pressure, Axis Bank ups loan rates by 5 bps

Facing margin pressure, Axis Bank ups loan rates by 5 bps RBI refuses to cut repo rate: Will your home loan EMIs come down?

RBI refuses to cut repo rate: Will your home loan EMIs come down? RBI's CRR move to put monthly burden of Rs 1,050 crore on banks

RBI's CRR move to put monthly burden of Rs 1,050 crore on banks MCLR Cut: Is it time to get a home loan or should you wait some more?

MCLR Cut: Is it time to get a home loan or should you wait some more?