Explained: How drop in PNB MCLR will impact your home, personal and car loans

In a major good news to borrowers, state-owned lender Punjab National Bank has cut down its marginal cost of fund based lending rate (MCLR) by 10 basis points with immediate effect.

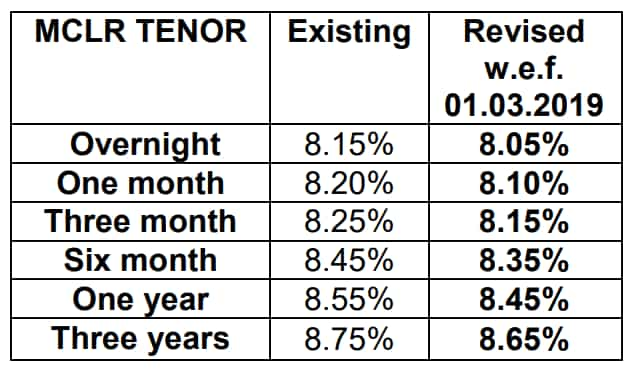

In a major good news to borrowers, state-owned lender Punjab National Bank has cut down its marginal cost of fund based lending rate (MCLR) by 10 basis points with immediate effect. At PNB, now MCLR for overnight stands at 8.05% from previous 8.15%, while for 1 month tenure it is at 8.10% from previous 8.20%. For six month period, MCLR comes at 8.35% from previous 8.45%. In case of 1 year, MCLR now is at 8.45% from previous 8.55% and in the highest bracket, this lending benchmark is now at 8.65% from previous 8.75%. Such comes as a sign of relief to retail borrowers seeking to take personal, home and car loan. MCLR is a boundary which is set by banks and their overall lending depends upon this factor.

If MCLR is trim down, such should create an impact on new borrowers as their EMIs will become cheaper on loans. However, the existing borrowers can decide to shift, but there are certain factors that loan taker must note before making any decision.

The MCLR is the latest one to be developed by RBI which replaced the previous base rate of deciding lending rates. Effective since April 01, 2016, MCLR was supposed to bring transparency in the methodology adopted by a bank for calculating interest rates on home loan, car loan, personal loan, etc.

Banks decide on their interest rate by adding components to MCLR. These are - marginal cost of funds, Cash Reserve Ratio, operating costs and tenor premium.

But how exactly MCLR impacts your loans depends upon the spread decided by a bank.

Every month, a bank resets the MCLR rate either by increasing or cutting or keeping it unchanged. However, whatever be the MCLR, it is the spread decided for a loan that will reflect in your EMIs. Take note, a floating rate for loans is offered at a spread over the benchmark.

There are two situations that can arise from MCLR cut.

Situation 1 - MCLR cut, Spread same

For example - Currently, your MCLR rate is at 9% with a spread over benchmark of 25 basis points. This will mean your home loan interest rate comes at 9.25%. If the bank decides to cut MCLR by 10 basis points and keeps the spread at 25 bps. This would mean your MCLR has come down to 8.90% and with spread of 25 bps, your home loan then will come at 9.15%.

Such is a very rare occasion, as RBI has complained on banks not following a transparent form of lending.

Situation 2 - MCLR cut, spread hike

This is a most likely the picture on your lending rates. For example, MCLR rate which was at 9%, was brought down to 8.75%. The bank further decides to hike spread by 25 bps, which will now become 50 bps. Hence, then your home loan rate remains unchanged at 9.25%.

Therefore, make sure to know your banks spread on your loan over MCLR.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

03:53 PM IST

HDFC Standard Life buys PNB Housing Finance shares worth Rs 90 crore

HDFC Standard Life buys PNB Housing Finance shares worth Rs 90 crore PNB Housing Finance jumps 11% on strong Q2 performance; broader market shows mixed trends

PNB Housing Finance jumps 11% on strong Q2 performance; broader market shows mixed trends  Eraaya Lifespaces' subsidiary secures Rs 250 million contract - Details

Eraaya Lifespaces' subsidiary secures Rs 250 million contract - Details fixes floor price for share sale") Punjab National Bank (PNB) fixes floor price for share sale

Punjab National Bank (PNB) fixes floor price for share sale  Karnataka government pauses SBI, PNB deposit withdrawals for 15 days

Karnataka government pauses SBI, PNB deposit withdrawals for 15 days