Small Saving Schemes turn attractive ahead of festive season; This is how it will hurt your EMIs on home, car loans

Notably, now investment in Small Saving Schemes looks way more attractive than what banks are offering you.

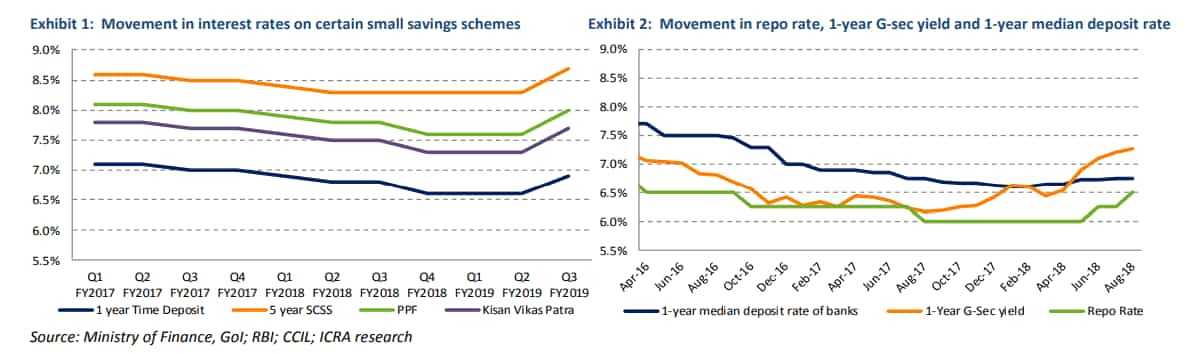

Making investment in savings deposits even more exciting for lower and middle class citizens, the government recently hiked interest rates on its small saving schemes. Govt hiked the interest rate after keeping rates unchanged for two quarters. For the October - December 2018 period, the interest rates increased in the range of 30 basis points to 40 basis points in various categories of investment pool. Notably, now investment in these schemes looks way more attractive than what banks are offering you. This surely will boost government’s schemes.

In ICRA’s view, this hike in interest rates on small savings schemes is largely in line with the uptrend displayed by G-Sec yields of various maturities, during the trailing three-month period. For instance, the G-Sec yields on 1-year, 2-year and 5-year bonds have increased on average by around 52 bps, 45 bps and 36 bps, respectively, in June-August 2018 relative to the previous three-month period.

In previous two quarters, the interest rates were kept unchanged despite the 10-year benchmark G-Sec yields for their corresponding reference periods had increased by 61 bps and 26 bps, respectively.

Small saving schemes are categorised under three broad heads (i) postal deposits, comprising savings account, recurring deposits, time deposits of varying maturities and monthly income scheme (MIS); (ii) savings certificates, including National Small Savings Certificate (NSC) and Kisan Vikas Patra (KVP); and (iii) social security schemes such as public provident fund (PPF) and Senior Citizens‘ Savings Scheme (SCSS).

Govt’s new rates on small savings schemes!

- For one year deposit, the interest rate is 6.9% quarterly from previous 6.6%.

- As for 5 year recurring deposits, the interest rate is increased to 7.3% on quarterly basis compared to previous 6.9%.

- Senior citizens are the biggest beneficiaries under new rates, as now they will receive 8.7% on 5 year savings scheme on quarterly and paid basis.

- On monthly income account, a person will receive 7.7% interest rate from previous 7.3%.

- Also in NSC, a person will get 8% interest rate annually from previous 7.6%. Similarly in Public Provident Fund Scheme, a person gets 8% interest rate annually from previous 7.6%.

- In case of savings made in Kisan Vikas Patra, you will be eligible to receive 7.7% on maturity in 112 months.

- Even the government increased interest rates to 8.5% annually in savings made under Sukanya Samriddhi Account Scheme from previous 8.1%.

Interestingly this new development in small savings scheme would be positive for government, however, it would not be a good news for banks and at some point RBI. What you need to remember is that, if banks are affected than you are impacted especially when it comes to your EMIs paid on home loans, personal loans and car loans.

Firstly, the systemic liquidity is expected to tighten in H2 FY2019, related to the upcoming harvest, festive and marriage season, state elections and busy season for credit.

ICRA said, “While this would nudge banks to increase their deposit rates in Q3 FY2019, the extent of the same would lag the overall increase in the repo rate and the magnitude of the recent revision in small saving rates.”

As a result, ICRA expects small savings schemes to provide an attractive alternative to bank deposits in the coming months, which should help the GoI to avail a higher net amount from the NSSF, compared to its target of Rs. 1.0 trillion in FY2019

Therefore, such schemes have at times been highlighted as a factor that hampers transmission of monetary easing to bank deposit and lending rates, particularly during periods of tight liquidity.

MPC has raised the repo rate by 25 bps each in June 2018 and August 2018, which has only been partly transmitted to bank deposit rates. Since the beginning of FY2019, banks have raised rates on one-year, three-year and five-year deposits by 10 bps, 25 bps and 25 bps, respectively.

Experts at ICRA added that, the looming inflation risks, the robust GDP growth print for Q1 FY2019 and the continued weakening of the INR, suggest a high likelihood of a third consecutive rate hike of 25 bps in the October 2018 policy review. This is likely to be accompanied by a change in stance to withdrawal of accommodation, to signal another potential rate hike in the December 2018 policy review, unless inflation risks recede appreciably during Q3 FY2019.

Now if this is the case, that RBI may add another rate hike in India’s policy repo rate, then your interest rates on borrowing would go higher making your EMIs expensive.

Each lending and deposit rates decided by any bank has a direct relationship with policy repo rate.

When banks borrow funds from the central bank during shortage. For instance, now they are paying higher interest rate which is 6.50% this was not the case two policy ago as they just paid 6% till June 2018. So now with a 50 basis points hike borrowing from RBI becomes costly for banks.

Banks usually opt for loan from RBI after analysing their liquidity position and cost of funds before increasing the deposit rates and lending rates.

If there is a need of funds, then banks will begin in passing their repo rate burden on you by raising lending rates. It needs to be noted that, home loans and other floating rate loans are the ones which get highly impacted when RBI hikes repo rate.

Other option to save themselves from RBI’s repo rate, would be hike in deposit rates so that customers find it attractive to make investment with them.

However, as per ICRA, the hike in deposit rates by PSBs seem very limited.

Given the weak capital position of most public-sector banks (PSBs), their credit growth is likely to remain limited in FY2019, which would curtail their incremental deposit requirements and the need to attract additional funds by hiking deposit rates.

Some PSBs, which are relatively better placed on capital are like the State Bank of India (SBI), Canara Bank and the Bank of Baroda, may pursue credit growth, but the incremental hike in their deposit rates is likely to be limited because of reduced competition from other PSBs.

While as per ICRA, the private banks are in a position to pursue substantial credit growth and gain market share at the cost of the PSBs, they have not been able to make a large dent in the deposit franchise of the latter, despite offering somewhat higher deposit rates than PSBs.

An increase in deposit rates by PVBs may not necessarily result in a meaningful gain in their share in deposits; hence, they are likely to undertake modest calibrated hikes in their deposit rates in the immediate term.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

03:43 PM IST

From income tax slab to saving schemes - what has Budget 2023 done to Personal Finance? Here are the top 10 pointers

From income tax slab to saving schemes - what has Budget 2023 done to Personal Finance? Here are the top 10 pointers Kisan Vikas Patra scheme offers 6.9 pct interest; Which other schemes are offering HIGHER INTERESTS - Know here

Kisan Vikas Patra scheme offers 6.9 pct interest; Which other schemes are offering HIGHER INTERESTS - Know here SCSS Vs PPF Vs Sukanya Samriddhi – which savings scheme gives you HIGHEST RETURNS? Compare and find out yourself

SCSS Vs PPF Vs Sukanya Samriddhi – which savings scheme gives you HIGHEST RETURNS? Compare and find out yourself SCSS, PPF and Sukanya Samriddhi – 3 savings schemes with highest returns; Know features, benefits here

SCSS, PPF and Sukanya Samriddhi – 3 savings schemes with highest returns; Know features, benefits here Top small savings schemes interest rates: From NSC, PPF recurring deposit, Senior Citizens Savings Scheme, time deposit and more

Top small savings schemes interest rates: From NSC, PPF recurring deposit, Senior Citizens Savings Scheme, time deposit and more