Mutual Funds vs Bank Deposits: What should be your preferred financial product?

In earlier years when the inflation was at a high rate, Bank Fixed Deposit was an attractive choice, as there was zero risk and substantial return on the money invested. But, nowadays this is not the case with Bank Fixed Deposits. Though the risk level has not gone up the return side has faced a downfall.

Diwali celebrations just came to an end and most of us have started working on new financial plans. But, have you changed your investment plan which will definitely influence your finances in future? Let’s understand the best investment sectors available today in India.

In earlier years when the inflation was at a high rate, Bank Fixed Deposit was an attractive choice, as there was zero risk and substantial return on the money invested. But, nowadays this is not the case with Bank Fixed Deposits. Though the risk level has not gone up the return side has faced a downfall.

So, investment in FDs ignoring the core benefits of Mutual Funds, SIPs, etc. is just because of the unawareness and lack of knowledge. Due to that we are nothing but losing the extra money that can be earned.

In last 3 years, the interest rates are drastically fallen around 40 percent, which is kind of freaking. People generally end up doing incorrect mathematics of the returns on investments. As every step in the downfall of interest rates appears very small. Rate cuts are generally around 0.25% to 0.5% which prima facie sounds nothing.

In India, we can also say, it is a traditional issue, that we have hardly seen our parents investing in Equity or Mutual Funds. At a young age when we have all our strength and skillsets with us and ample opportunities waiting for us to earn money, the risk involved in Mutual funds seems tiny as compared to huge returns offered by it. As in any worst case scenario, if we do not get return up to that level or say we get returns less than FDs Risk free Rate. We are able to re-earn that opportunity loss as we are at the start of our career.

We should always invest in Mutual Funds instead of FDs. FD holders would not hesitate to invest in Mutual Funds having low-risk profiles. These have nearly at par rates of return with those of fixed deposit income.

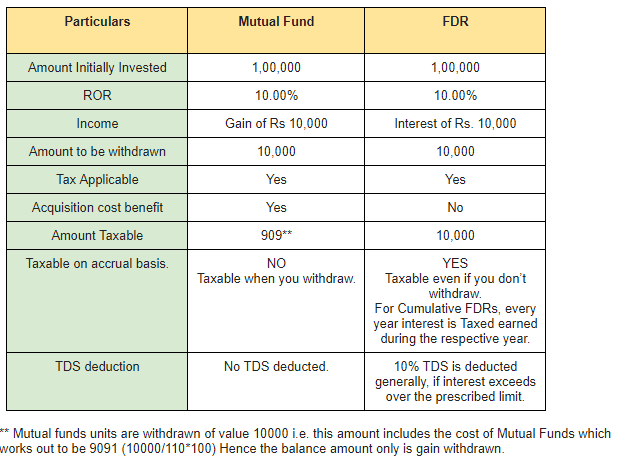

In addition to this, there lies a hidden benefit: Taxation. While withdrawing gains earned in Mutual Fund Investments, the tax required to be paid works out very less as compared to the case of withdrawal of interest of FDR. following table of comparison elaborates this.

For, easy calculations suppose the rate of return is 10.00% in both cases.

Following are differences to understand the best investment option:

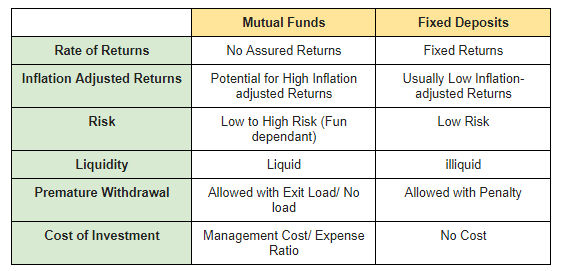

Fixed Deposits Vs Debt Mutual funds

● Liquidity: After redemption money can be received within 1–2 days

● Professional management: Can dynamically alter strategy & avail benefit of market

● No penalty on premature withdrawal.

Mutual funds are definitely depending on the market condition, unlike the FDs. But, if you are in the age bracket of 25 to 30 yrs and you can take risk (not a huge one) then you should invest most of your money into Mutual Funds or SIPs as it will give you extra benefits. Investors are suggested to invest in SIP for a longer duration (more than 5 years) to achieve desired financial goals. This is not the case with Fixed Deposits.

So, most likely, the yield on mutual funds would always be higher than fixed deposits given that you invest for long term and keep monitoring your money.

Rishabh Parakh is a Chartered Accountant and the Chief Gardener & Founder Director of Money Plant Consulting, a leading Tax & Investment Planning Advisory Service Provider. He also runs a personal finance blog called “Mango Investor” aka AAM Niveshak at www.mangoinvestor.com.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

12:56 PM IST

10 Financial habits to avoid for a smoother and diligent financial life

10 Financial habits to avoid for a smoother and diligent financial life  The Rule of 72: How long will it take for your monthly investment to cross Rs 10 lakh with 12% returns?

The Rule of 72: How long will it take for your monthly investment to cross Rs 10 lakh with 12% returns? Why for achieving financial freedom investors need to have adequate insurance coverage?

Why for achieving financial freedom investors need to have adequate insurance coverage? HCLTech elevates Shiv Walia as Chief Financial Officer

HCLTech elevates Shiv Walia as Chief Financial Officer Why over diversification of portfolio can jeopardise your financial planning? Know expert view

Why over diversification of portfolio can jeopardise your financial planning? Know expert view