Are you planning to take loan from these banks; your EMIs on home, personal loan will rise ahead

By hiking a repo rate RBI has taken a lot of risk. While it tries to ease down inflation, consumers will face the brunt of this hike.

The Reserve Bank of India (RBI) has given an open invitation to banks in freely hiking their lending rates on home loans, auto loans and personal ones as well. The central bank has set a new table by raising policy repo rate by 25 basis points for the first in the Narendra Modi government’s reign of four years. RBI had no option but to take policy repo rate at 6.25% from previous 6% due to higher crude oil, MSP hike and 7th Pay Commission which are hampering their CPI inflation target in future. Now this hike in repo rate would give further chance to lenders in raising their MCLR which will in return mean any loan taken would make you pay higher EMIs. Many banks both state-owned and private ones have already started raising their benchmark lending rates, which is a bad news for consumers.

By hiking a repo rate RBI has taken a lot of risk. While it tries to ease down inflation, consumers will face the brunt of this hike.

As the benchmark Marginal Cost based of lending rate (MCLR) is directly linked to Repo Rate - therefore any increase in repo rate will lead to increase in MCLR.

Such would in return lead to rise in interest rate for borrowers who have taken floating rate home loan, personal loan and business loan.

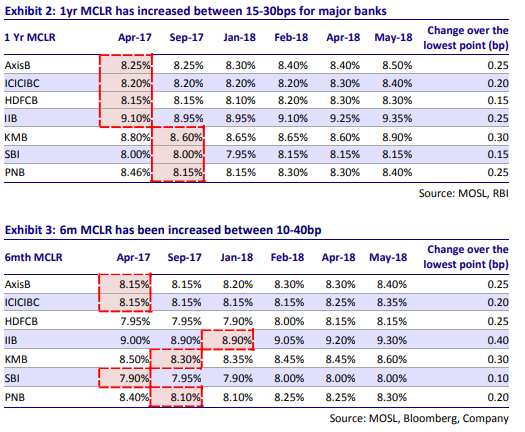

If you have loan or are planning to borrow from the below mentioned bank than your EMI is set to rise. So far these banks have raised MCLR in the range of 5 basis points to 140 basis points.

Largest lender State Bank of India (SBI) was first to not shy away in raising MCLR by 10 basis points to 8.25% for a tenure of 1 year from previous 8.15%. Other banks followed suit.

Currently, ICICI Bank and HDFC Bank are charging MCLR rate of 8.40% each for 1 year tenure.

Meanwhile, banks like Indian Bank, Punjab National Bank, Bank of Baroda, Syndicate Bank and Bank of India have raised MCLR for 1 year tenure to 8.50%, 8.40%, 8.45%, 8.55% and 8.50% respectively.

On the other hand, Oriental Bank of Commerce and Karur Vyasa Bank have raised MCLR highest to 8.65% and 9.30% for a tenure of 1 year.

Higher lending rates is a good news for banks because that is their main source of income but bad news for consumers because they are ones who will pay higher interest rates.

Rajnish Kumar, Chairman, SBI on RBI monetary policy said, “The RBI decision to raise repo rate by 25 bps is a preemptive and welcome move. Simultaneously, the decision to keep the stance in neutral mode indicates RBI willingness to be flexible and accommodative. On the development front, the bouquet of measures are positive. In particular, the increase in FALLCR will provide more liquidity to banks and moderate short end interest rates. Other measures like increase in threshold limits for affordable housing, encouraging continued formalization of MSME sector are in the right direction. The change in SDL valuation norms are long term positives and the spread of MTM losses over 4 quarters will provide the banks with much needed relief.”

While R SubraimaniaKumar, MD & CEO, Indian Overseas Bank said, “The Policy with neutral stance and the narratives are towards strengthening the fundamentals, especially the inflation. Economic revival on a sound footing and increased capacity utilization are reassuring statements, which will spruce up investments.”

SubraimaniaKumar added, “Recognising the MSME sector strain and extending the relief of 180 days for asset classification is a very positive and forward-looking step. Banks may have some relief as well.”

An EMI is a fixed amount of money that a borrowers needs to pay on a monthly basis to lenders or financial institutions, towards the loan amount they have taken.

Nitin Aggarwal and Alpesh Mehta analysts at Motilal Oswal said, “We however expect deposit/lending rate to tighten further as deposit growth remains subdued (8.5% currently vs credit growth of 13.1%) while incremental loan-deposit ratio (one year) remains elevated (111% currently).”

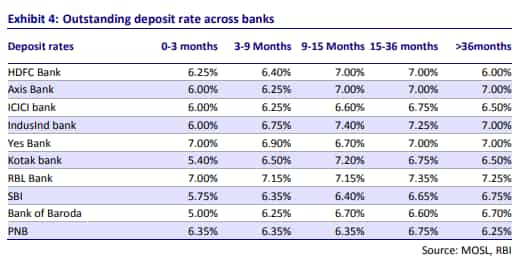

Teresa John, Analysts at Nirmal Bang says, “In our view, the rise in market interest rates is encouraging a shift to bank credit from non-banking sources such as the commercial paper and corporate bond market. With higher rates being the only means to garner deposits to fund credit growth, banks are increasing deposit rates.”

John added, “Consequently, lending rates will continue to edge up, but at a slower pace than inflation which implies that real lending rates are likely to trend downwards (not into negative territory) in the near term, which is growth supportive.”

Apart from raising policy repo rate, RBI boosted lending for affordable housing in Pradhan Mantri Awas Yojana (PMAY). It also warned banks regarding low ticket housing loans.

The duo at Motilal said, “The revision in housing loan limit for PSL eligibility will help bring convergence of Priority Sector Lending guidelines with the Affordable Housing Scheme and support the growth in low-cost housing segment. SBIN, BOB, HDFCB, ICICIBC, AXSB will benefit most from this with in our coverage.”

It needs to be noted that, RBI has shown disappointment in banks way of rising MCLR earlier because the central bank believed that lenders are not giving in policy repo rate of 6% benefit to end consumers.

However, now the tables of have turned. With RBI having a job to control inflation, the banks will see good credit growth of the back of higher lending rate, but consumers will be the one to face brunt of such an outcome.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

04:26 PM IST

RBI December monetary policy decision: Repo rate remains steady for eleventh time; 'neutral' stance continues

RBI December monetary policy decision: Repo rate remains steady for eleventh time; 'neutral' stance continues RBI Governor says inflation horse has been brought to stable with a lot of effort: Full text of his October 9 speech

RBI Governor says inflation horse has been brought to stable with a lot of effort: Full text of his October 9 speech RBI Monetary Policy: Governor Shaktikanta Das proposes to cut cheque clearance time to a few hours

RBI Monetary Policy: Governor Shaktikanta Das proposes to cut cheque clearance time to a few hours Retail inflation gradually easing, food prices still a concern: RBI Bulletin

Retail inflation gradually easing, food prices still a concern: RBI Bulletin Nifty crosses 23,000, Sensex up over 800 pts after RBI revises FY25 GDP growth projection to 7.2%

Nifty crosses 23,000, Sensex up over 800 pts after RBI revises FY25 GDP growth projection to 7.2%