5 tax saving options other than 80C

Section 80C of the Income Tax Act of 1961 is one of the most popular tax saving options that allows for deductions up to Rs 1.5 lakh per annum. However, there are various other tax-saving options available that taxpayers may avail benefit from.

Section 80C of the Income Tax Act of 1961 is one of the most popular tax saving options that allows for deductions up to Rs 1.5 lakh per annum. PPF contributions, five-year term deposits and ELSS schemes are among the list of tax-free instruments under this section. However, there are various other tax-saving options available that taxpayers may avail benefit from. Here are a few:

1. Section 80E: Exemption of interest on education loan

Under section 80E, income spent to meet the interest component of education loans is not taxable. There is no limit on the deduction amount. However, it has to be noted that such a waiver is available for a maximum of 8 years or till the interest is paid. Any income spent beyond this time duration is taxable. It can be utilized to meet the higher education charges of either self, children or spouse.

These tax deductions can be availed by individuals only. Hindu Undivided Families (HUF) and companies can not avail of these tax exemptions.

2. Section 80TTA -Interest income generated from savings account deposits

Under section 80TTA, a deduction of up to Rs 10,000 per year on savings account interest is allowed. However, if one maintains multiple savings accounts in different banks, total cumulative interest is considered and is taxed under ‘income from other sources’.

If interest income exceeds Rs 10,000 in a year, depending upon aggregate annual income, the excess amount over the cap is taxed at rates. This tax deduction can be availed by individuals and HUF. Besides, NRIs may also avail of deduction under Section 80TTA.

Also read- Income tax return filing: What is ITR 1 Sahaj form? Check eligibility and steps to file online

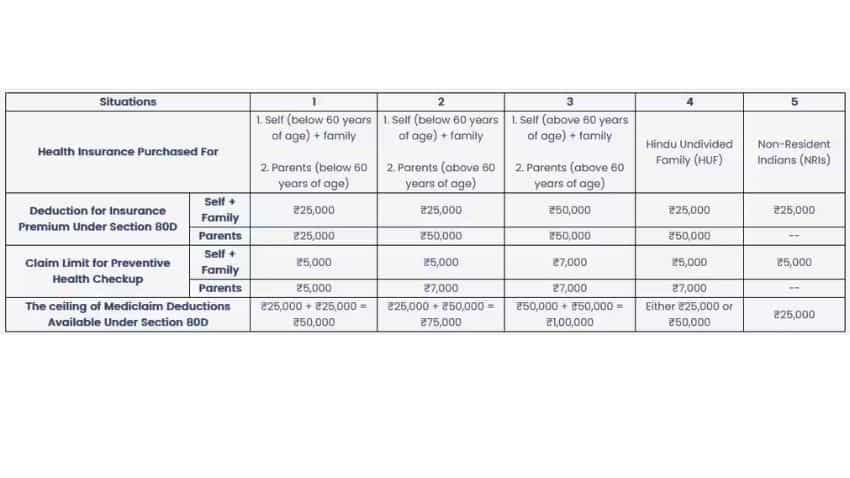

3. Section 80D- Deduction for Medical & Health Insurance

Under section 80D, money spent on medical and health insurance can be claimed. One is allowed to claim a tax deduction of up to Rs 25,000 on medical insurance premiums per financial year. The deduction limit of Rs 50,000 is allowed in the case of senior citizens. The limit applies to the premium paid towards health insurance purchased for self, spouse, children

and parents.

Medical expenditure incurred on senior citizens (aged 60 years or above) health is not covered under any health insurance scheme.

4. Section 80G--Donations made to charitable organizations

One can claim a deduction under section 80G for any income donated to charitable organisations. However, all donations do not cover under the section. Cash donations are exempt from tax calculations for up to Rs 2,000. Any cash donation exceeding the same does not qualify for the deduction.

Such contributions have to be made to registered charitable organisations. NRIs are also eligible to claim the benefits under Section 80G, given that their donations are to eligible trusts or institutions.

5. Section 10(10D)- Life insurance policy payout

Under Section 10(10D), the entire sum assured disbursed upon maturity of life insurance (maturity or death benefit) can be claimed for a tax rebate. However, such death benefit is exempted from tax calculations if it is availed after 1st April 2012, and total value premium charges are less than the full sum assured. If the policy is availed before 1st April 2012, then the premium expenses should be less than 20% of the total sum assured to be eligible for waivers under section 10(10D).*

HUFs, salaried and non-salaried individuals, foreign companies, body of persons and others are eligible for these tax exemptions.

Click Here For Latest Updates On Stock Market | Zee Business Live

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

02:09 PM IST

Zomato gets Rs 803.4 crore tax demand from GST authorities

Zomato gets Rs 803.4 crore tax demand from GST authorities  Income tax refunds jump 46.3% to Rs 3.04 lakh crore in April-November

Income tax refunds jump 46.3% to Rs 3.04 lakh crore in April-November No proposal on income tax relief for senior citizens under consideration: Centre

No proposal on income tax relief for senior citizens under consideration: Centre  Income tax return filer base up 2.2 times in 10 years, 5 times growth in Rs 50 lakh-plus income category: Sources

Income tax return filer base up 2.2 times in 10 years, 5 times growth in Rs 50 lakh-plus income category: Sources  This is India's only tax-free state, residents earn crores without paying Income Tax

This is India's only tax-free state, residents earn crores without paying Income Tax