Income Tax: The Indian Income Tax system is intricate as it covers important aspects of the economy. There are various concepts in Income Tax and one concept that is often confusing for taxpayers is the difference between Tax Deducted at Source or TDS and Tax Collected at Source or TCS.

Let us understand both concepts in detail.

Income Tax: What is Tax Deducted at Source or TDS?

TDS is the amount deducted from payments made for specified services. The source can be professional fees, contract payments, commission and royalty payments and so on. TDS can also be applied to certain types of investment including interest earned from fixed deposits and other deposits in banks, post offices, and so on.

The concept of TDS was introduced with the aim to collect tax from the source of income.

Income Tax: How does TDS work?

According to the concept of TDS, a person or an institute (deductor) who is liable to make payment for service shall deduct tax at source and remit the same into the account of the Central Government.

This TDS amount can be claimed back on the basis of Form 26AS for the TDS certificate issued by the deductor.

Income Tax: TDS tax slab

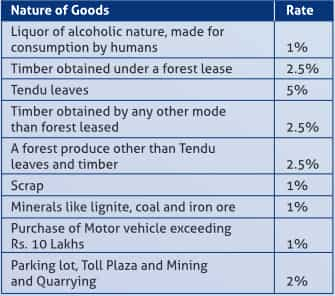

Income Tax: What is Tax Collected at Source or TCS?

A tax collected by a seller or a service provider from the buyer at the time of sale of goods or provisions of services is TCS. It is applicable to certain goods and services such as alcohol, coal, toll plaza, etc.

It is applicable on amounts involved in the transaction more than Rs 2 lakhs. The TCS rate varies from 0.1 per cent to 10 per cent depending upon the type of goods or services.

Income Tax: TCS slab

Income Tax: TCS Vs TDS

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

11:51 AM IST

Zomato gets Rs 803.4 crore tax demand from GST authorities

Zomato gets Rs 803.4 crore tax demand from GST authorities  Income tax refunds jump 46.3% to Rs 3.04 lakh crore in April-November

Income tax refunds jump 46.3% to Rs 3.04 lakh crore in April-November No proposal on income tax relief for senior citizens under consideration: Centre

No proposal on income tax relief for senior citizens under consideration: Centre  Income tax return filer base up 2.2 times in 10 years, 5 times growth in Rs 50 lakh-plus income category: Sources

Income tax return filer base up 2.2 times in 10 years, 5 times growth in Rs 50 lakh-plus income category: Sources  This is India's only tax-free state, residents earn crores without paying Income Tax

This is India's only tax-free state, residents earn crores without paying Income Tax