EPFO members alert! Some say National Pension System is better than EPF, VPF; know what NPS calculator says

EPFO members or Employees' Provident Fund Organisation subscribers have been mandatorily investing 12 per cent of their basic monthly salary in the Employees' Provident Fund (EPF) account as the EPF interest rate is 8.5 per cent and its completely risk-free.

EPFO members or Employees' Provident Fund Organisation subscribers have been mandatorily investing 12 per cent of their basic monthly salary in the Employees' Provident Fund (EPF) account as the EPF interest rate is 8.5 per cent and its completely risk-free. Taking advantage of this, some people add the Voluntary Provident Fund (VPF) component too as it helps EPFO members to garner whopping returns without taking any risk.

However, in the changed circumstances, when EPF interest earned on more than Rs 2.5 lakh per annum investment is under income tax scanner, should the middle class continue to invest in EPF and opt VPF as it will help them earn more and save income tax too?

According to tax and investment experts, one should look at the National Pension System or NPS Scheme too as it is market linked and in the long-term time horizon, it would give around 10 to 11 per cent returns, which is around 1.5 per cent to 2.5 per cent higher than EPF interest rate.

Batting in favour of NPS Scheme, SEBI registered tax and investment expert Jitendra Solanki said, "NPS Scheme is market linked while EPF or VPF is completely risk-free. In NPS, one gets exposure in both equity and debt while EPF or VPF is completely a debt investment. An NPS account holder can choose up to 75 per cent equity exposure while there is binding that one can't withdraw more than 60 per cent of the NPS maturity amount."

WATCH | Click on Zee Business Live TV Streaming Below:

Standing in sync with Solanki, Manikaran Singhal, Founder, easymponeying.com said, "EPF or VPF is income tax exempted under Section 80C while in NPS, there is additional Rs 50,000 income tax exemption other than Section 80C. However, in my opinion, both are long-term investments and in the long-term, one can expect at least 12 per cent returns on equity and 8 per cent returns on debt investments. So, if a person chooses 60 per cent equity and 40 per cent debt exposure then, in the long-term, an NPS account holder can expect to garner more than 10 per cent returns from NPS, which is around 2 per cent higher than EPF or VPF.

NPS Calculator

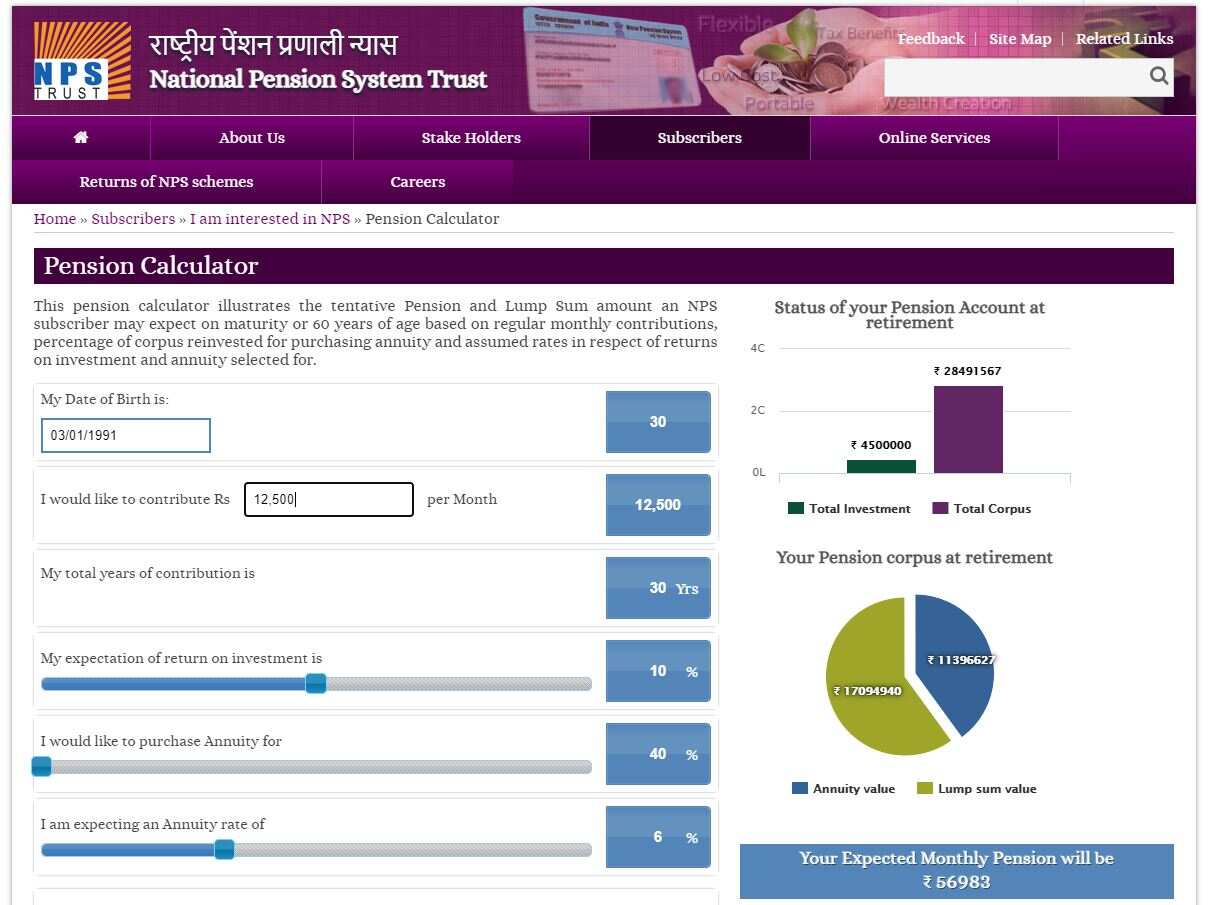

Checking the numbers out with an NPS calculator made it simple. Solanki said that if someone invests Rs 1.5 lakh in NPS for 30 years, the withdrawal amount will be Rs 1,70,94,940 or Rs 1.70 crore plus Rs 56,983 monthly pension.

Source: NPS Trust

Source: NPS Trust

EPF maturity amount

However, if we invest the same amount in EPF account assuming 8.5 per cent EPF interest rate for the entire 30 years period, the net amount at the time of redemption will be Rs 2,84,91,567 or Rs 2.849 crore but there will be no monthly pension available after withdrawal.

Income post retirement

Solanki said that even if one goes for bank FD with the residual amount of Rs 1,13,96,627; one's annual income would be Rs 5,69831.35 or Rs 47,485.94 per month (assuming 5 per cent bank FD) and it would be taxed like one's annuity in the case of NPS pension. So, if we compare the monthly income from Bank FD from the surplus amount gained through EPF investment, the return as pension would be lesser.

So, in the end, it would be better to go with NPS than EPF or VPF.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

09:12 AM IST

EPFO, ESIC subscribers may soon use claim amounts via e-wallets: Labour Secretary

EPFO, ESIC subscribers may soon use claim amounts via e-wallets: Labour Secretary EPFO extends deadline for employers to upload pending pension applications until January 31, 2025

EPFO extends deadline for employers to upload pending pension applications until January 31, 2025 EPFO Board approves key reforms: Auto-claim limit increased to Rs 1 lakh, pension disbursement streamlined & other decisions

EPFO Board approves key reforms: Auto-claim limit increased to Rs 1 lakh, pension disbursement streamlined & other decisions Domestic youth unemployment lower than global levels: Labour Ministry

Domestic youth unemployment lower than global levels: Labour Ministry Labour Ministry asks EPFO to focus on preparations to launch ELI Scheme

Labour Ministry asks EPFO to focus on preparations to launch ELI Scheme