Explained: What are different types of banks in India and how they function?

Different types of banks have different eligibility criteria that they need to fulfill to be listed under the Reserve Bank of India (RBI).

The Ministry of Finance has been holding several pre-budget meetings with different shareholders of the market and industry experts. The Finance Minister also had a pre-budget meeting with the trade union leaders, where the representatives voiced their strong disagreement against the privatization of banks. This year, several banks including co-operative banks, non-scheduled commercial banks, and payment banks have been in the limelight for different reasons.

Here are the details of different types of banks and the eligibility criteria they need to fulfill to be listed under the Reserve Bank of India (RBI).

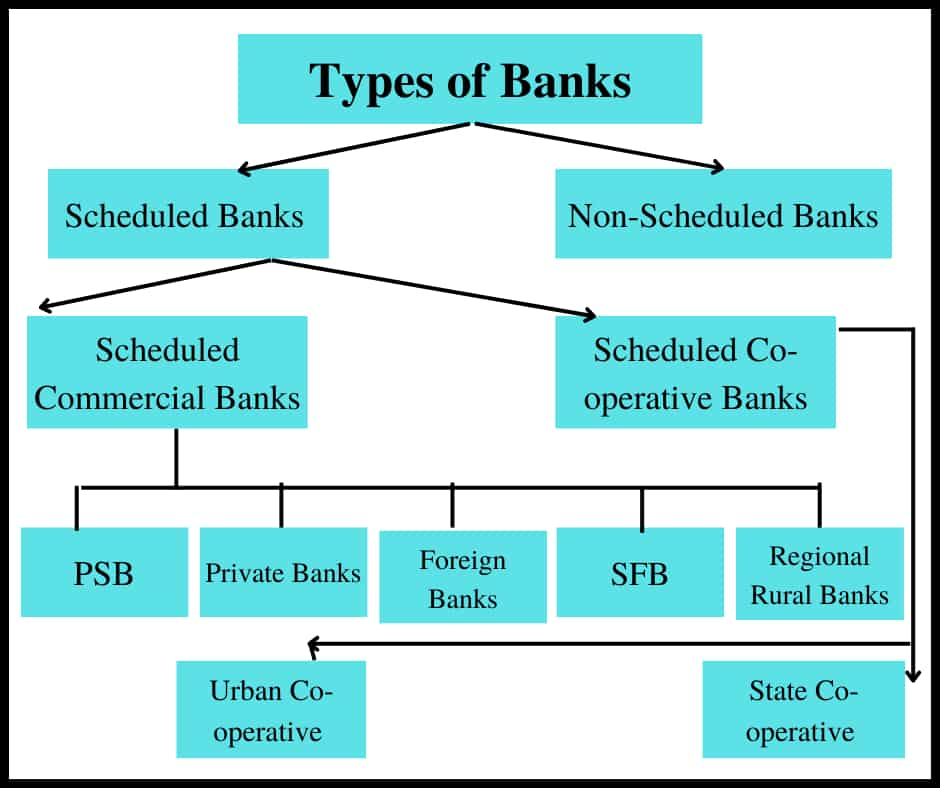

1. Scheduled Banks

The scheduled banks are those banks that are listed in the second schedule of the RBI Act 1934. But a bank needs to have a paid-up capital and raised funds of at least Rs. 5 lakh to be eligible as a scheduled bank. One of the major benefits of these banks includes availing low-interest loans from the RBI. These banks also need to maintain an average daily CRR (Cash Reserve Ratio) balance with the central bank according to the rates set by it.

These banks also are liable to submit returns at regular intervals, to the RBI as per the regulations of the Reserve Bank of India Act, 1934 and Banking Regulation Act, 1949.

Scheduled banks are broadly of two types:

Scheduled Commercial Banks

Scheduled Co-operative Banks

A) Scheduled commercial banks

Scheduled commercial banks can further be classified into 5 different categories:

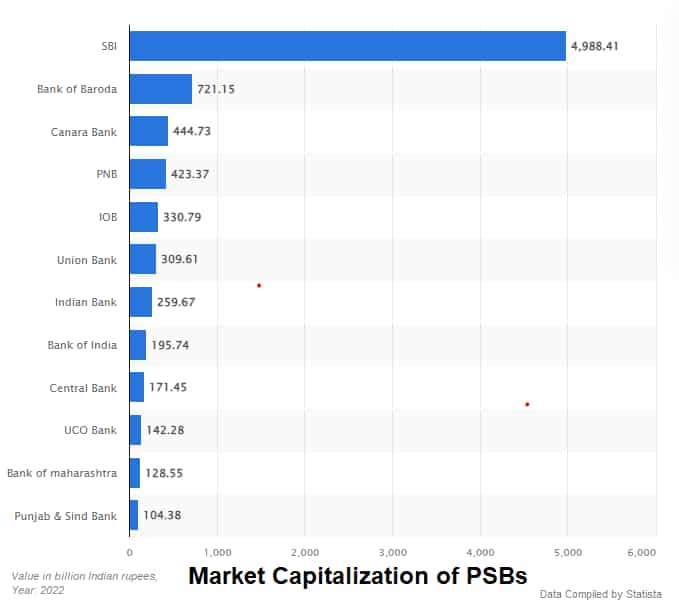

i. Public Sector Banks (PSBs)

These are the government-owned banks in India, where a majority stake is held by the Ministry of Finance of the Government of India or the finance ministry of other state governments of several other states in India. PSBs currently has a total market capitalization of more than Rs. 8200 billion as of May 2022. In PSBs, the government should own 50 per cent or more of the total stocks of the banks.

ii. Private Sector Banks

In these banks, private individuals or entities own the majority of the shares or equity. Private banks that were established before 1968 are classified as the old private sector banks and those established after 1991 (after economic reforms) are categorized as new public sector banks. Such banks currently have a total market capitalization of more than Rs 23000 billion.

iii. Small finance banks (SFBs)

As per the guidelines of the RBI, SFBs have been established to cater to the need of the unserved and underserved sections of the population, and supply credit to small business units; small and marginal farmers; micro and small industries; and other unorganized sector entities, through high technology-low cost operations. Resident individuals/professionals (Indian citizens), singly or jointly, each having at least 10 years of experience in banking and finance at a senior level; and Companies and Societies in the private sector, that are owned and controlled by residents (as defined in FEMA Regulations, as amended from time to time), and having a successful track record of running their businesses for at least a period of five years, can set up small finance banks, as per the norms. RBI has mandated that The minimum paid-up voting equity capital for small finance banks shall be Rs.200 crore, except for such small finance banks which are converted from UCBs.

Currently, the total market capitalization of SFBs stands at more than Rs 50,000 crore in 2022.

iv. Regional Rural Banks

These banks operate at the regional level in different states of India with a population usually around 10,000 and have been formed under the Regional Rural Banks Act, of 1976. As per the Regional Rural Banks (Amendment) Bill, 2014, the authorized capital of each RRB should be Rs 5 crore. It does not permit the authorized capital to be reduced below Rs 25 lakh.

v. Foreign Banks

Banks with their head offices based in cities abroad and their branches in India are classified as Foreign banks.

In India, there are currently 12 PSBs including the State Bank of India (SBI), Bank of Baroda etc, 21 private sector banks like Axis, and ICICI, 12 Small Finance banks (Suryoday SFB and Ujjivan SFB), four payment banks, 43 regional rural banks, and 45 foreign banks.

B) Scheduled Co-operative Banks

A co-operative bank is a small-sized, financial entity, with its members being the owners and customers of the Bank. They are registered under the States Cooperative Societies Act.

They are broadly classified into:

Urban co-operative banks (UCB): These banks are co-operative banks in urban and semi-urban areas. RBI has hiked the minimum capital adequacy ratio (CAR) for Urban Cooperative Banks (UCBs) with deposits above Rs 100 crore to 12 per cent from the earlier floor of 9.0 per cent in July’22.

State co-operative banks: They are the highest-level cooperative banks in each of the states. There are around 24 state co-operative banks.

2. Non-scheduled Banks

These banks are not listed in the 2nd schedule of the RBI act, 1934. Thus, they don’t need to fulfill all the criteria under clause 42 but need to follow specific guidelines as laid down by RBI. Banks with a reserve capital of less than 5 lakh rupees are classified as non-scheduled banks. There are three such banks in India which include Capital Local Area Bank Ltd - Phagwara (Punjab), Krishna Bhima Samruddhi Local Area Bank Ltd, Mahbubnagar (Andhra Pradesh), and Subhadra Local Area Bank Ltd., Kolhapur (Maharashtra)

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

05:04 PM IST

PSU banks' gross NPA falls to 5.53%; total profit stands at Rs 70,167 crore in Apr-Dec FY23

PSU banks' gross NPA falls to 5.53%; total profit stands at Rs 70,167 crore in Apr-Dec FY23 Banks, financial institutions need to design project-specific products for meeting Rs 111 lakh crore NIP target, says DFS Secretary

Banks, financial institutions need to design project-specific products for meeting Rs 111 lakh crore NIP target, says DFS Secretary Banking stocks showstopper in otherwise volatile market; BoB, PNB gain most - check valuations

Banking stocks showstopper in otherwise volatile market; BoB, PNB gain most - check valuations CKYCR identifier number: RBI confirms centralized KYC for all bank accounts coming soon — check how it will work and benefit account holders

CKYCR identifier number: RBI confirms centralized KYC for all bank accounts coming soon — check how it will work and benefit account holders  SBI slashes FY23 growth forecast from 7.5% to to 6.8% on way-below Q1 GDP numbers

SBI slashes FY23 growth forecast from 7.5% to to 6.8% on way-below Q1 GDP numbers