Cement sector Q1 review: What lies ahead after mixed performance in Q1? Check top stocks to bet on

According to Nirmal Bang Securities, at 93 million tonnes (MT), cement volumes in the June quarter increased by 14 per cent YoY. The overall volume was up by 10 per cent YoY at 380 MT in FY23, the brokerage notes.

)

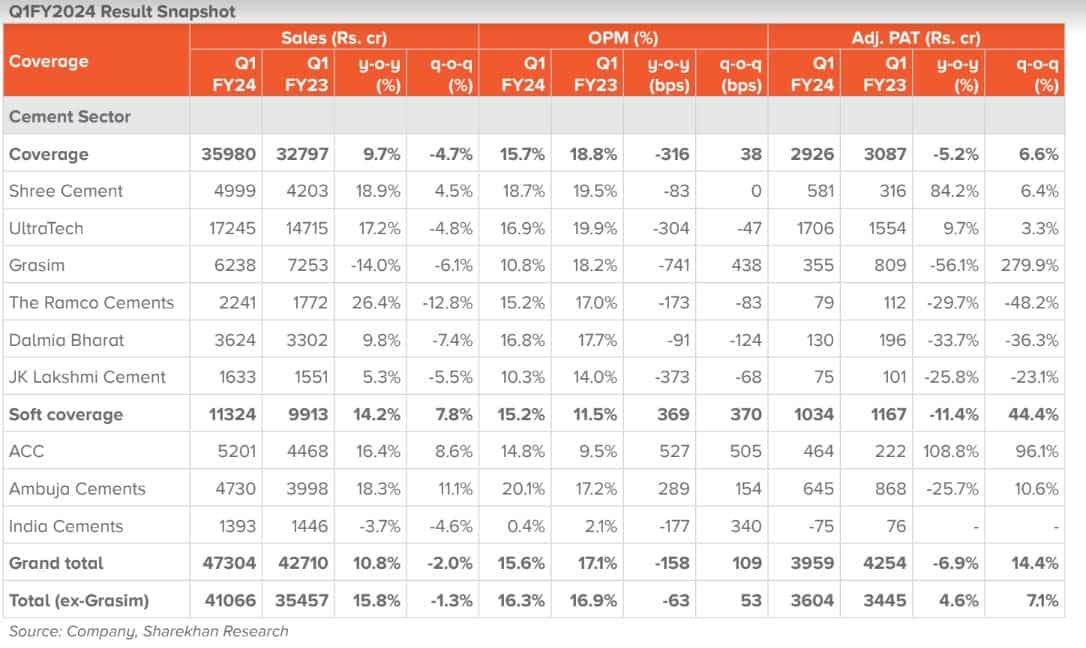

The cement sector reported mixed results for the quarter ended June 30, 2023 (Q1 FY24). According to a report by Sharekhan, the cement companies' revenue during the quarter grew 15.8 per cent year-on-year (YoY), with a dip of 6.3 per cent YoY in weighted average EBITDA/tonne. The net profit increased marginally by 4.6 per cent YoY, while blended realisations declined by 2.5 per cent YoY, as estimated.

According to Nirmal Bang Securities, at 93 million tonnes (MT), cement volumes in the June quarter increased by 14 per cent YoY. The overall volume was up by 10 per cent YoY at 380 MT in FY23, the brokerage notes.

As per analysts tracking the sector, encouraging demand from the housing and infrastructure sectors, coupled with the low base of 1QFY22, which was hit by the second COVID wave, were the main drivers for cement volume.

"A strong demand environment, along with lower power and fuel costs and other expenses, aided earnings growth," said Sharekhan.

On the other hand, realisations dropped 0.5 per cent to 4 per cent quarter-on-quarter (QoQ), according to a report by ICICI Securities.

What's ahead for the cement sector?

Nirmal Bang Securities believes favourable macro trends will boost the cement industry’s growth in FY24, as overall cement consumption will increase from 9 per cent to 10 per cent in FY24, even though pricing will remain flat compared to FY23.

Further, cement demand is expected to rise given the government's commitment to infrastructure development and the ongoing need for housing amid rapid urbanisation and rising housing loan penetration.

Sharekhan expects cement companies to continue to benefit from a strong demand outlook in FY2024, along with better control of key operating costs.

"Power and fuel costs are expected to tread lower over the next two quarters, while pet coke and coal prices are showing signs of inching upwards," the report said.

It added that cement prices are expected to remain stable during FY2024, given a strong demand environment, and most capacity additions are slated to come on stream by FY2024-end and during FY2025.

Conversely, ICICI Securities is cautious about the cement sector due to the following factors:

a) continued weak pricing power;

b) historical evidence of a fuel cost drop, not driving;

c) the risk of low demand in FY25 due to a high base in FY24;

d) high odds of huge capacity build-up in FY26E;

e) uncertainty owing to aggressive capacity addition by Adani Cement

Which stocks should one buy?

UltraTech, Grasim Industries, The Ramco Cements, and JK Lakshmi Cement are preferred picks of Sharekhan.

ICICI Securities has maintained a 'reduce' rating on UltraTech Cement, Shree Cement, and Orient Cement and a 'sell' call on India Cements.

Meanwhile, the brokerage recommends adding shares of ACC, Ambuja Cement, and Grasim.

It recommends buying shares of JK Cement.

Nirmal Bang Securities is bullish on the following stocks:

Stock returns

Catch the latest stock market updates here. For all other news related to business, politics, tech, sports and auto, visit Zeebiz.com.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

03:27 PM IST

Supreme Court ruling on royalties, taxes to affect mining firms' profitability: Moody's

Supreme Court ruling on royalties, taxes to affect mining firms' profitability: Moody's  Cement sector Q4 preview: Volume likely to grow in high single-digits; impact of weak cement prices to be offset by lower costs, operating leverage

Cement sector Q4 preview: Volume likely to grow in high single-digits; impact of weak cement prices to be offset by lower costs, operating leverage Cement sector Q3 preview: EBITDA likely to improve amid low double-digit demand growth

Cement sector Q3 preview: EBITDA likely to improve amid low double-digit demand growth Cement companies likely to invest Rs 1.2 lakh crore to add 145-155 metric tonnes capacity by FY27

Cement companies likely to invest Rs 1.2 lakh crore to add 145-155 metric tonnes capacity by FY27 UltraTech's margin disappoints Street, weighs on other cement stocks. Here's what investors should do

UltraTech's margin disappoints Street, weighs on other cement stocks. Here's what investors should do