Tata Motors top Nifty50 loser as auto major posts higher-than-expected loss in Q2; brokerages divided

Despite a lower than estimated September quarter results, at least 3 brokerages are bullish on Tata Motors stock and see an upside of 13-25%. Jefferies, which has maintained a buy rating on this stock puts over Rs 100 as an upside in the counter and is most bullish about the prospects of India’s leading OEMs in automotive space

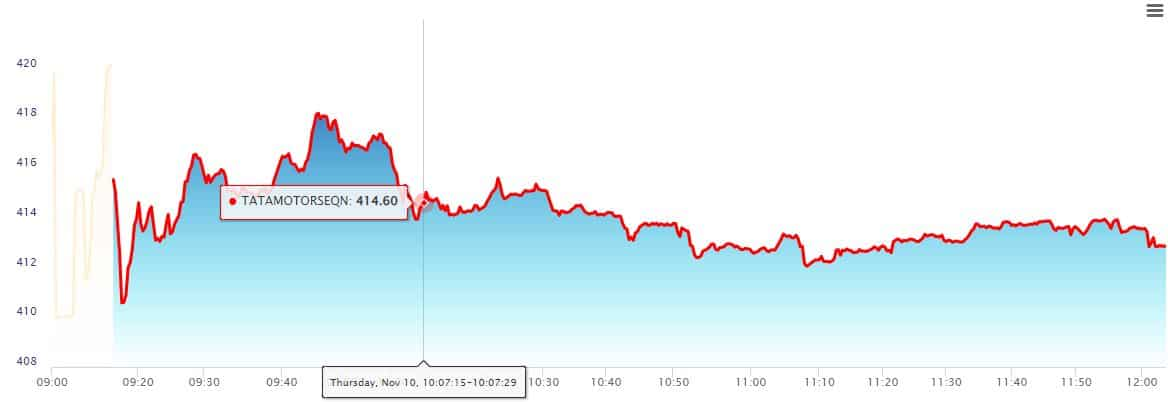

Tata Motors Share Price: Tata Motors crashed more than 5 per cent on Thursday, November 10, after the domestic automaker posted higher-than-expected net loss in the second quarter of the current financial year. The counter opened at Rs 420.50 apiece on the NSE and selling pressure dragged the stock to touch day's low of 409.20, emerging as top Nifty50 loser. The scrip had closed at Rs 433.15 in the last session. At 11:45, it quoted Rs 413 apiece.

Earlier on Wednesday, Tata Motors narrowed its consolidated net loss to Rs 945 crore for the September quarter, as sales picked up in marquee brand Jaguar Land Rover and across domestic as well as commercial vehicle segments. The auto major had reported a net loss (attributable to shareholders) of Rs 4,442 crore in the July-September period of the last fiscal. Total income increased to Rs 80,650 crore in the quarter under review, as compared to Rs 62,246 crore in the year-ago period, the company said in a regulatory filing.

The street estimated a profit of Rs 529 cr.

Meanwhile, despite a lower than estimated September quarter results, at least three brokerages are bullish on Tata Motors stock and see an upside of 13-25 per cent. Jefferies, which has maintained a buy rating on this stock puts over Rs 100 as an upside in the counter and is most bullish about the prospects of India’s leading OEMs in automotive space.

Meanwhile, CLS has raised its target price from Rs 473 to Rs 491 on strong passenger vehicle business and double digit margins for the commercial vehicle segment.

Morgan Stanley remains ‘Overweight’ on this stock and has put a target of Rs 502. The stock was recommended at the price of Rs 433.

However, JP Morgan has taken a contrarian view on the stock and cut the earlier price target of Rs 455 to Rs 410. The brokerage firm has ‘Neutral’ stance on this scrip. The brokerage in a note said that the reason for its down grade is attributed to JLR Q2 wholesales has disappointed, though retail was slightly better. It has cut FY23-24 consolidated EPS by 12-25 per cent. The brokerage is also of the view that the zero net debt target could get pushed beyond FY25.

Among other key metrics, EBITDA stood at Rs 6196 crore for the reporting quarter versus Rs 4050 crore and was up 53 per cent. Margins were up at 7.8 per cent against the estimated 10.5 per cent. In the year ago period they were at 6.6 per cent.

Demand continues to remain strong, however, it will remain a key monitorable in wake of global uncertainties, the company has warned in ts quarterly earnings filing to the exchanges.

The client order book is now at 205,000 units. The three most profitable models, the New Range Rover, New Range Rover Sport, and Defender account for over 70% of the order book

New electric model development on track, with work to transform our UK plants for the next generation of BEVs underway

Company focussing on signing long-term partnership agreements with chip suppliers, the company has said.

Source: NSE

Source: NSE

The stock has traded in wide range hitting its 52-week high of Rs 536.70 and 52 week low of Rs 366.20 in a span of 6 months.

(Disclaimer: The views/suggestions/advises expressed here in this article is solely by investment experts. Zee Business suggests its readers to consult with their investment advisers before making any financial decision.)

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

12:13 PM IST

Tata Motors announces price hike on trucks and buses; shares under pressure

Tata Motors announces price hike on trucks and buses; shares under pressure Tata Motors to hike commercial vehicle prices by up to 2% from January 2025

Tata Motors to hike commercial vehicle prices by up to 2% from January 2025 Tata Motors showcases advanced technology at BaumaConexpo 2024

Tata Motors showcases advanced technology at BaumaConexpo 2024 Tata Motors shares rise over 1% as company announces third price hike in 2024

Tata Motors shares rise over 1% as company announces third price hike in 2024 Tata Motor to raise passenger vehicle prices by up to 4% from January 2025

Tata Motor to raise passenger vehicle prices by up to 4% from January 2025