Cementing your portfolio: Sharekhan sees Rs 1300 per share gains in UltraTech Cement; lists 4 triggers with this CAVEAT

UltraTech Cement shares have underperformed the Nifty50 by over 11% in 1-year yielding negative 5.4% returns versus 5.9% returned by the latter according to data sourced from Trendlyne. Momentum indicators RSI and MFI are at 50.8 and 63.6, respectively. A number below 30 is considered oversold and above 70 indicates overbought

Strong demand for cement from infrastructure, rural and urban housing segments coupled with benign fuel and raw material cost bodes well for UltraTech Cement Company. Brokerage firm Sharekhan estimates Rs 1300 per share gains in this counter, banking on four factors while underlining a strong caveat.

Stock to Buy | UltraTech Cement | CMP 7,099 | Target: Rs 8,500 | Upside: 18%

The stock was recommended at a price of Rs 7223. It quoted Rs 7,099 on the NSE on Monday at 11:45 AM, up 1.22 per cent from the Friday closing price.

Tailwinds

1) Cement Price Outlook: Led by a healthy price increase undertaken in the east, pan-India cement prices in October-November 2022 have increased by 1.3 per cent compared to Q2FY2023 average and are up 3 per cent versus Q3FY2022. Prices in eastern region were up 4 per cent m-o-m and 14 per cent y-o-y followed by the central region - up 3 per cent both m-o-m and y-o-y.

2) Growth Outlook: UltraTech is expected to see sustained demand emanating from the rural and infrastructure sectors. Further, demand from the real estate segment in the urban sector has started to witness strong traction with favourable government policies and a lower interest rate regime. Management is optimistic about a sustainable demand environment for the cement sector over the next 4-5 years, barring the near-term impact of the second wave.

3) Power and fuel costs: International coal prices declined by 8.5 per cent q-o-q during Q3FY2023 till date, while domestic prices corrected by 6 per cent m-o-m for December 2022 (average Q3FY2023 flat q-o-q) after rising 15.4 per cent m-o-m in October and 4.6 per cent in November. Retail diesel prices for October-November 2022 have stayed flat compared to Q2FY2023, while they are lower by 0.7 per cent YoY. UltraTech is expected to benefit from the expected decline in power and fuel costs partially during Q3FY2023 and fully during Q4FY2023, this brokerage noted.

4) Greenfield & Brownfield Expanions: In December 2022, the company commissioned 5.5 mtpa grinding units - 1.8 mtpa greenfield at Dhule in Maharashtra; 1.8 mtpa brownfield at Dhar in Madhya Pradesh and 1.9 mtpa greenfield at Pali in Rajasthan - taking its total cement manufacturing capacity in India to 121.35 mtpa. UltraTech also commenced production of 4 LMT wall care putty plant in Rajasthan during November 2022, taking its total wall care putty capacity to 13 LMT. UltraTech is the largest manufacturer of grey cement, ready mix concrete (RMC), and white cement in India.

Impact on Key metrics

Robust demand outlook, upward price revisions along with softer fuel and material costs will ensure better realization in key financial parameters including revenues, operating profit margins (OPM) adjusted net profit and EPS.

Source: NSE

Source: NSE

Technical View:

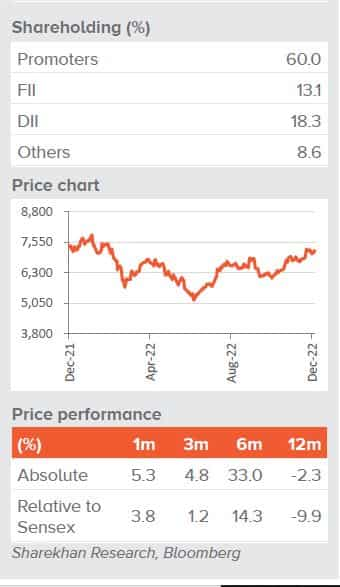

UltraTech Cement shares have underperformed the Nifty50 by over 11 per cent in 1-year yielding negative 5.4 per cent returns versus 5.9 per cent returned by the latter according to data sourced from Trendlyne. Momentum indicators RSI and MFI are at 50.8 and 63.6, respectively. A number below 30 is considered oversold and above 70 indicates overbought.

The stock is trading at PE multiple below industry medium.

The stock has been volatile with a Beta above 1 over the last three months.

Technical analyst Nilesh Jain holds a positive view on this stock and recommends buying at current levels and even on declines. Jain said that UltraTech stock has strong support at Rs 6750 while resistance at Rs 7300 which is the first target. He puts the next target at Rs 7600.

Jain, who is Assistant Vice President - Lead Derivative and Technical Research at Centrum Broking has a 8-week view on this scrip.

Valuation - Peer Comparison

Sharholding Pattern

Caveat:

Slowdown in housing sector demand or government spending on infrastructure or increased key input costs led by pet coke and diesel prices could unsettle the applecart, Sharekhan note in its report. Inability to improve capacity utilisation and profitability of acquired units could also be counterproductive for the company it said.

(Disclaimer: The views/suggestions/advises expressed here in this article is solely by investment experts. Zee Business suggests its readers to consult with their investment advisers before making any financial decision.)

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

09:37 PM IST

Dalmia Bharat, JK Cement, HeidelbergCement gain up to 3%: What's driving gains?

Dalmia Bharat, JK Cement, HeidelbergCement gain up to 3%: What's driving gains? UltraTech Cement to expand its electric truck fleet to 100

UltraTech Cement to expand its electric truck fleet to 100 Lower sales realisation hit margins of cement makers in Q2

Lower sales realisation hit margins of cement makers in Q2 india cements ultratech share price srinivasan sold promoter stake free float

india cements ultratech share price srinivasan sold promoter stake free float  UltraTech to acquire stake in India Cements by 32.72% worth Rs 3,954 crore

UltraTech to acquire stake in India Cements by 32.72% worth Rs 3,954 crore