Castrol India to piggyback on lubrication industry growth, says HDFC Securities; recommends buy

The brokerage firm recommends a buy in this stock in the Rs 135-138 band with accumulation on dips to Rs 119.5 –122.5 band (14.0xCY22E EPS). It gives the price targets of Rs 151 and Rs 169 over the next 2 quarters. At the CMP of Rs 136.45 the stock trades at 15.8x CY22E EPS

Lubrication industry is likely to grow by 4-5 per cent over the next 2-3 years with Castrol India likely becoming the biggest benefactor, according to an HDFC Securities report. Castrol’s market share in the bazaar segment stands at 22-23 per cent with the nearest rival having a market share of 7 per cent, the report said.

Castrol India is an automotive and industrial lubricant manufacturing company.

See Zee Business Live TV Streaming Below:

In 2-wheeler, 4-wheeler and Commercial Vehicles segments, Castrol had 26-27 per cent, 35 per cent and 18 per cent market share respectively.

Despite weak demand due to lockdown, Castrol reported realisation at Rs197.7/ltr in Q2CY21 vs Rs 186.7/ltr in Q1CY21.

Recommendations

The brokerage firm recommends a buy in this stock in the Rs 135-138 band with accumulation on dips to Rs 119.5 –122.5 band (14.0xCY22E EPS). It gives the price targets of Rs 151 and Rs 169 over the next 2 quarters. At the CMP of Rs 136.45 the stock trades at 15.8x CY22E EPS.

This stock ended at Rs137.20, down by almost 1.4 per cent from the Friday closing price.

Fundamentals

The fundamentals are supported by healthy liquidity, zero debt with no plans to raise further debt.

Its financial flexibility is strong, supported by robust liquidity. As on 30 June 2021, the company has cash and cash equivalent of Rs 1162 cr and free cash flow to Enterprise value stood at 8.3 per cent in CY20 versus 7.4 per cent in CY19.

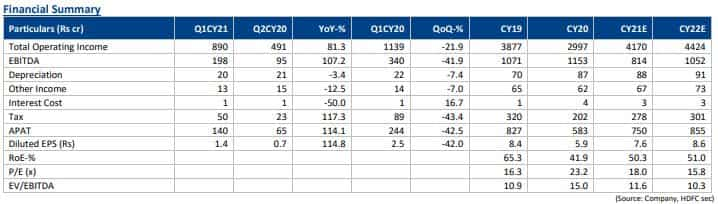

Castrol’s revenues from operations rose from Rs 2993 cr in CY11 to Rs 3877 cr (CY19, which is a 4% CAGR over the period. The revenue stood at Rs 2,997 cr in CY20, hit by the onslaught of Covid-19 pandemic. The Company reported EBITDA margin at a range of 26-30 per cent and net profit margin at a range of 18.5-21 per cent over the last six years.

The working capital has remained positive and the capex has also remained stable over the years.

Castrol is also expected to invest in niche acquisitions to strengthen its domain expertise in the medium term. These will be largely funded from its cash surplus and healthy accruals.

HDFC Securities has revised earnings and increased target price for the stock on the back of healthy growth outlook and strong profitability numbers in Q2CY21.

See Chart Here:

Key Triggers

HDFC Securities said that the sector is expected to grow despite challenges on account of demand disruptions due to COVID-19 pandemic, intensifying competition, slowdown in global/domestic macro-economic factors and rising popularity of Electric vehicles (EVs).

Castrol is in a strong position to withstand these challenges on account of its strong brands, technology and enduring relationships with key stakeholders, the report further said. Castrol has taken three price hikes since January and possesses high pricing power and commands premium for its products.

Castrol’s market share improved 2 per cent across all segments in Q2CY21. The company owns around 20 per cent market share in the overall Indian lubricants market.

Stock Performance

The stock has achieved targets of Rs 128 and Rs 136 after being recommended previously by HDFC Securities. The stock was recommended at Rs 116.70.

It also gives high dividend payout to investors, the report said.

Peer Comparison Chart:

Caveats

- The report acknowledges slowing growth for the company owing to market saturation, improved product quality requiring late replacement of lubes and electrification of vehicles in India.

- Supply disruptions on account of base oil and raw materials availability, logistics challenges and rupee depreciation are likely to adversely impact demand and supply.

- There is normal trend of some Original Equipment Manufacturers (OEMs) introducing lubricants under their own brand name, further impacting the competitive landscape.

- Growing popularity of Electric Vehicles could dampen the demand for lubricants as EVs have very less moving parts and hence require minimal lubrication.

(Disclaimer: The views/suggestions/advices expressed here in this article is solely by investment experts. Zee Business suggests its readers to consult with their investment advisers before making any financial decision.)

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

12:19 PM IST

Castrol India appoints Rakesh Makhija new chairman

Castrol India appoints Rakesh Makhija new chairman Castrol India spikes 5% after management’s strong guidance in analyst meet

Castrol India spikes 5% after management’s strong guidance in analyst meet Castrol India result: 4% increase PAT at Rs 194 crore

Castrol India result: 4% increase PAT at Rs 194 crore Q4 Results 2022: Tata Consumer Products, Havells, Castrol India announce March quarter results; here are key highlights

Q4 Results 2022: Tata Consumer Products, Havells, Castrol India announce March quarter results; here are key highlights Castrol India has cash of Rs 1,300 crore in the balance sheet: Deepesh Baxi, CFO & Wholetime Director

Castrol India has cash of Rs 1,300 crore in the balance sheet: Deepesh Baxi, CFO & Wholetime Director