Alok Saigal of Edelweiss Wealth decodes process of long-term wealth creation via different asset classes

Investing through an asset allocation approach requires discipline, but more than anything it requires time because only in the long-term one would be able to see the results of asset class decisions, Alok Saigal, President & Head, Private Wealth, Edelweiss Wealth Management said.

Investing through an asset allocation approach requires discipline, but more than anything it requires time because only in the long-term one would be able to see the results of asset class decisions, Alok Saigal, President & Head, Private Wealth, Edelweiss Wealth Management said in an interview with Zeebiz’s Kshitij Anand.

Alok has a total experience of over 19 years. Prior to joining Edelweiss, he has held leadership roles in corporate and investment banking, investment management, and advisory both in India and Singapore at HDFC Bank and Darashaw.

See Zee Business Live TV Streaming Below:

Edited Excerpts:

Q) Is there a perfect asset class for any portfolio? What should be the criteria?

A) The concept of savings and investment for an individual or an entity could be as subjective as choosing one’s clothing or preferring selective cuisines.

Different investors prefer different routes to meet their objectives, life goals etc. This can also depend on the accessibility to a particular asset class even if an investor has developed a liking.

Multiple factors need to be evaluated in order to explore the multi-faceted investment world before someone can be assigned a ‘perfect’ asset class for oneself.

In fact, investing through an asset allocation approach requires discipline, but more than anything it requires time because only in the long term one would be able to see the results of asset class decisions.

This is what makes the process of identification of suitable asset classes very important at the very early stages of investing.

A curated process to analyze appropriate risk-reward dynamics is needed while choosing an asset class as per the specific needs of an investor.

For example, an investor with the need for capital protection would primarily invest in a safe asset class like fixed income while restricting the allocation in equity to a minimum.

This tells us that the investor needs to clearly outline needs, objectives, goals, and risk appetite so that a ‘perfect’ asset class could be suggested.

Q) Which are various asset classes available to investors?

A) An investor should be aware of various asset classes available in the market and at the same time should be able to differentiate between asset classes based on return, risk, correlation, etc.

Basically, instruments carrying similar attributes, both from a descriptive and statistical perspectives, as well as showing high correlation among each other are classified into a single asset class.

Also, a single instrument cannot be classified as part of more than one asset class. So, with this understanding, let’s look at various asset classes available before we talk about selecting one out of many.

Equity:

The instruments under this asset class provide shares into ownership of the company. Theoretically, in case of liquidation of the company, proceeds against the equity shares are guaranteed after the debt is paid.

However, this textbook definition does not pass through one’s mind while investing in equity. Instead, the factors like added risk, superior returns, and easy liquidity associated with equity asset class form part of decision-making pertaining to asset allocations.

High volatility associated with equity also brings mark-to-market losses in the portfolio, but at the same time acceptance of higher risk can also provide a kicker in the portfolio return wise, if equity allocation is increased.

Although, the risk associated with equity investing, if measured by the probability of negative returns, decreases substantially in the longer run.

Fixed Income:

This asset class is characterized by capital protection and guaranteed regular income to the investors. Securities like govt. securities, corporate bonds, and money market instruments form part of this asset class.

Capital protection coupled with significantly reduced volatility as compared to that in equities, make this asset class preferable for investors with lower risk appetite.

Company treasuries often prefer fixed income instruments simply for the primary objective of capital protection. It has also been observed that as an individual investor ages and approaches retirement, they prefer to allocate more into fixed income instruments.

Others:

Real estate, commodities or even cryptocurrency can be as treated different asset classes depending on their attributes. The value of real estate can vary depending upon the cost of living and location and can act as a good investment to combat inflation.

The issue of liquidity in the real estate market becomes very important while investing and also valuing the portfolio later on. Gold is an important and arguably most popular commodity to invest in.

It is often regarded as a safe haven and is treated as a hedge against equity. In many popular investment solutions, even international equity is regarded as a different asset class as it is often used for the purpose of diversification.

Q) How do we compare performances of different asset classes?

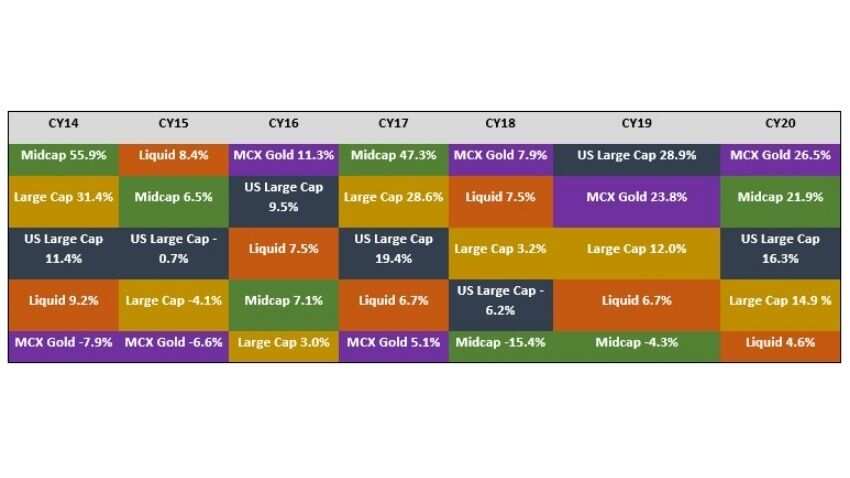

A) Identification of a perfect asset class becomes even more confusing when you look into the historical data. It can be very easily observed (as shown in the below table) that not a single asset class has come out to be the consistent winner.

Every year, there is altogether a different asset class or sub-asset class which comes out on top. For example, if we look at the decade of 2010s, US equity is the clear winner over any other emerging market equities but the same trend reverses when we look into the 2000s data.

It is often a tricky task to predict which sub-asset class will outperform for that specific period but a tactical allocation in right asset class at the right time can contribute towards creating alpha effectively. These experiences make diversification extremely important while not getting hung on to the idea of a perfect asset class.

As seen from the above illustration a perfect mix of multiple asset classes makes a good portfolio. As domestic equity is necessary for propelling growth, international equity becomes equally important for diversification purposes.

Gold provides a hedge against falling markets while fixed income is essential for capital protection. Risk-reward dynamics has to be well balanced in order to come up with perfect asset class allocations.

Dynamics of business cycles and economy have become important factors while tactically shifting from one asset to another. An investor needs to develop an outlook and overview of the economy as well as various asset classes.

Today, the economy and especially the financial world is globally entwined more than ever which makes it important to remain regularly updated.

For an investor, it is essential to be aware of the kinds of events that could have a larger impact on their portfolio and therefore should be able to realize the benefits of diversification across asset classes.

Q) What should one take into consideration while allocating money towards various asset classes? Please highlight the concept of diversification.

A) Diversification across asset classes is clearly the right way to invest but the optimum level of allocation in each asset class can be decided as per respective risk profiles. While devising an investment solution for an investor, risk profiling acts as a stepping-stone for the long journey.

This initial and extremely critical step acts as a guiding light for the identification of the perfect asset class. Depending upon the risk profiles, a dominant asset class with strategic asset allocation can be decided. We can look at some of the examples through various risk profiles to better understand the idea of a perfect asset class.

Conservative:

Under this risk profile, the primary aim remains to avoid undue market risks coupled with capital protection. Fixed income instruments form majority allocation while equity is capped to 25%-30% of the entire portfolio.

The stability of the portfolio is given more importance than returns. Capital protection becomes the driving factor while small allocations towards riskier assets keep providing added returns.

Moderate:

A balance between equity and fixed income is maintained under this risk profile. The allocation in equities is generally capped to 45-55% while return expectations and volatility remain somewhat bounded between what is expected under conservative and aggressive risk profiles.

Aggressive:

This is suitable for such investors who are willing to take more risks for added returns in the portfolio. In such cases, equity allocation becomes dominant as it can provide superior returns over others.

Allocation in riskier assets like equity can be as high as 80-90%, with some allocation towards fixed income for capital appreciation or tactical allocation purposes.

In all the above cases, diversification across other asset classes is also essential depending upon the needs of the investors. The asset class that investors are more inclined to depends on their risk appetite, financial goals and objectives.

In conclusion, we can say that a single asset class is not enough to meet all objectives of the investors. There can be varied objectives that can be met by allocation into different asset classes.

Each asset class provides its own unique dimension to the portfolio. All these dimensions become critical in creating a portfolio that can fulfill the needs of the investor in the best way possible.

So, it can be said that there is no perfect asset class but rather there exists a framework for achieving a near to ideal strategic asset allocation.

Gradually, the investor realizes that asset allocation becomes one of the most important factors in determining portfolio performance. It becomes easier to assess portfolio risks and performance attributes if a disciplined asset allocation approach is followed.

That makes a win-win situation for investors as they can achieve their objectives while having control over portfolio risks.

(Disclaimer: The views/suggestions/advice expressed here in this article are solely by investment experts. Zee Business suggests its readers to consult with their investment advisers before making any financial decision.)

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

11:11 AM IST

Edelweiss Financial Services sells Rs 1,759-crore stake in Nuvama Wealth

Edelweiss Financial Services sells Rs 1,759-crore stake in Nuvama Wealth  Edelweiss Alternatives fund acquires Bengaluru's MMTP Projects for Rs 1,500 crore

Edelweiss Alternatives fund acquires Bengaluru's MMTP Projects for Rs 1,500 crore Edelweiss Financial board clears Rs 1,500 crore fund raising via NCD

Edelweiss Financial board clears Rs 1,500 crore fund raising via NCD 1st company to introduce usage-based motor insurance in India - Edelweiss General Insurance launches Switch ‘Pay as you Drive’ add on

1st company to introduce usage-based motor insurance in India - Edelweiss General Insurance launches Switch ‘Pay as you Drive’ add on Edelweiss Housing Finance ties up with SBI for co-lending in priority sector home loans

Edelweiss Housing Finance ties up with SBI for co-lending in priority sector home loans