RBI walks the talk! Chooses CPI over weak rupee; is 75-mark soon-to-be reality? The case for domestic currency

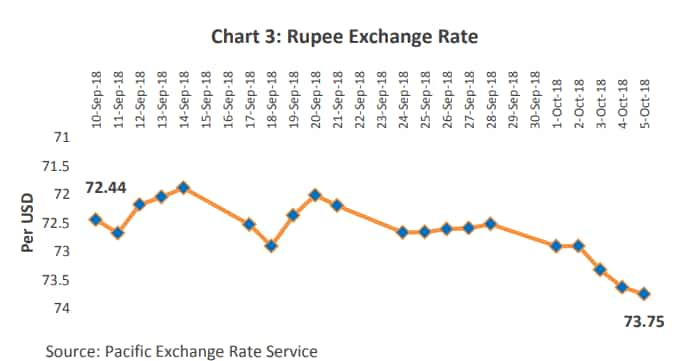

Today, the rupee finished at 74.040 down by 0.065 or 0.09% against US dollar. However, in early hours of trading, the Indian rupee touched an all-time low of 74.165.

The Reserve Bank of India (RBI) stayed firm on its word when it comes to making a policy decision. Even the villain of the piece, the Indian rupee, which has been weakening day by day and thereby giving the shivers to the country’s economy could not move the RBI from its set agenda. RBI has always been an inflation trajectory central bank, which is why, it led to the free fall in Indian currency - it touched an all-time low of over 74-mark against US dollar benchmark. Investors had high hopes for a rate hike from RBI during fourth bi-monthly monetary policy for India, however, the central bank chose to walk the talk. It was unexpected for sure, as the turbulence in domestic currency continued at interbank forex market. Today, the rupee finished at 74.040 down by 0.065 or 0.09% against US dollar. However, in early hours of trading, the Indian rupee touched an all-time low of 74.165.

Talking about today’s performance, VK Sharma, Head Private Client Group & Capital Market Strategy at HDFC Securities said, “Rupee continued to remain under pressure weighed by a further rise in long-term US Treasuries following non-farm payroll data. US 10-year yield jumps to a fresh 7-year high after unemployment rate falls to lowest in 49 years.”

It was the 6th straight session of rupee depreciating against the dollar.”

Well yes, rupee needs some disciplining from RBI and that too urgent one. Interestingly, on October 05, what was least expected was the actual outcome.

Yes a status quo was RBI’s decision. The central bank kept policy repo rate unchanged at 6.50%, and even lowered its CPI outlook ahead. However, the policy stance was changed to "calibrated tightening" compared to previous ‘neutral’.

The moment RBI announced a ‘no change’ decision, the madness in Indian rupee was immediately witnessed as it clocked for the first time over 74-mark against dollar on the same day itself.

From the policy decision last week, many interpretations can be made. Firstly, RBI stayed firm on its inflation target, as CPI eased to 3.69% during the month of August 2018 lower compared to 4.17% of the previous month. While core CPI inflation (ex. Food and fuel) also eased slightly to 5.8% Y-o-Y from 6.2% Y-o-Y in July.

Secondly, according to SBI, the rate decision by the RBI explicitly emphasizes that the Central Bank is largely tolerant with the exchange rate finding its market determined level and is concerned only to the extent that an exchange rate depreciation feeds into headline inflation.

Thirdly, a reason to believe that financial instability concerns may have made the RBI apprehensive of a rate hike at this point.

While another explanation can be that RBI chose to give more weightage to domestic side issues. The decision of status quo can be seen to cap the cost of borrowing in the domestic markets.

Abheek Barua, Chief Economist, HDFC Bank said, “On account of liquidity issues for the domestic NBFCs, risk of fiscal slippage, rising oil prices, and depreciating currency, the cost of borrowing in the domestic wholesale market has already gone up by around 36 bps (on average the upward shift in yield curve for India since the last MPC meet in August).

Barua explained that, a rate hike today would have further aggravated the pressure in the interest rates. Perhaps, the other way of looking at it is that when the recovery in private investment cycle is in its nascent stages, there could be a risk of over-doing the hike in interest rates. At this stage, the RBI seems to be okay with the 50 bps hike done in this cycle and the simultaneous rise in interest rates in the wholesale market that has come so far

Hence, RBI has its reasons for not breaking the ice when it comes to policy repo rate, and free fall in Indian rupee.

On the other hand, the external front involves many central banks have hiked the policy rates, depreciation in emerging market currencies, FII outflows from domestic bonds market and crude oil prices soaring to new heights.

Barua stated that, perhaps there was a case to hike the policy rate on October 05, but the RBI decided to give higher weightage to domestic side pressures.

However, it is noteworthy that, Indian rupee is one of the worst performing currencies this year, having depreciated by 12% from its previous year with foreign investors naturally withdrawing money from Indian market.

Now inflationary pressures and weak rupee has their own role to play in Indian economy. While the former has eased, the latter has become the worst nightmare. The real question is who impacts more to Indian economy at this point of time, and what can RBI do to bring financial stability. It is feels like RBI is trapped in a conundrum.

Although RBI decided for a status quo, yet the central bank left a window open for possible rate hikes ahead. RBI’s new calibrated tightening stance leaves room to act in case the rupee depreciates more and oil prices rise further.

Since April this year, the WTI crude oil prices have increased by 18% till Oct. 5th from USD 63 per barrel to USD 74 per barrel. Similarly, the Brent crude oil prices have surged by substantial 24% from USD 68 per barrel as on 1st Apr’18 to USD 84 per barrel as on 5th Oct’18.

Outlook ahead!

In Barua’s view, “Going forward, there is now an upside risk to our USD/INR call of 70-71 for December-end. It is clear that the RBI would let the market forces prevail and would not try to defend any particular level of exchange rate. That is, overshooting above the fair value (72-73 in our view) could also be acceptable unless it becomes a serious threat to inflation.”

“Given that oil is the most important driver at the moment for the exchange rate, we await to get further clarity about the oil market (Iran sanctions, increase in supply from OPEC etc.) and investors' behavior in response to today’s monetary policy decision before we change our call,” said Barua.

Care Ratings said, “We are expecting the rupee to vary between Rs. 71-75 up to March’19 depending on when the oil prices retreat.”

Shockingly, Sujan Hajra, chief economist at Anand Rathi Share and Stock Brokers said, "Barring an unexpected softening of crude oil prices and/or major improvements in global liquidity, the rupee touching 78 a dollar in the next six-nine months seems to be a distinct possibility.”

Can Urjit Patel do a Raghuram Rajan?

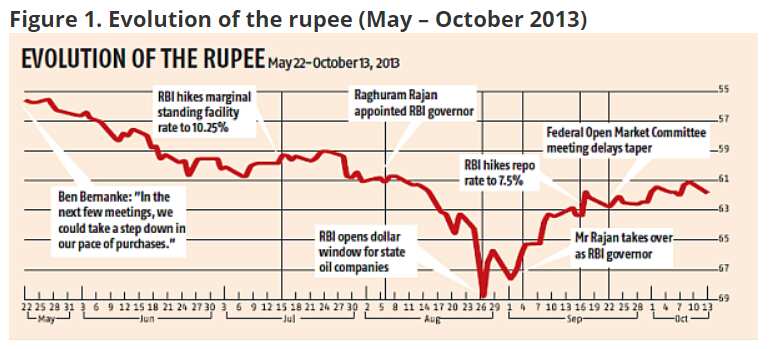

Remember 2013!

The rebellious free fall in Indian rupee is not new to the country, one such, in fact quite extreme scenario was witnessed in 2013. Rupee depreciated by 25% since June 2013, and was staring right at 69-mark per dollar by end of August 2013. FDI inflows in India witnessed decline of 38%, to $22.42 billion during in 2012–2013 versus $35.12 billion in 2011–2012. While, the country's current account deficit rose to 4.8% of GDP in 2012–2013, exceeding the government’s target level of 2.5% to 3% of GDP.

Hence, the rupee had been in free fall in August 2013, inflation and the current account deficit were high.

(Image Source: Arvind Subramanian blog in IdeasforIndia.in website in November 2013.)

A new face was going to take charge of RBI then. Raghuram Rajan who is known as the most successful economist and the writer of ‘I Do What I Do’, brought stability in not only Indian currency but his methods also helped the Indian economy.

Rajan who began his tenure on September 04, 2013, talked about the primary role of the RBI as preserving the purchasing power of the rupee. In Rajan’s mind there were two other important mandates; inclusive growth and development, as well as financial stability for India.

Within days into his job, Rajan proposed a special concessional window for swapping Foreign Currency Non-Resident (FCNR) deposits that mobilized following the recent relaxations permitted by the bank.

What basically was decided that, RBI offered a window to the banks to swap the fresh FCNR dollar funds, mobilized for a minimum tenor of three years and over, at a fixed rate of 3.5% per annum for the tenor of the deposit.

Based on requests received from banks, RBI decided that the current overseas borrowing limit of 50% of the unimpaired Tier I capital will be raised to 100% and that the borrowings mobilized under this provision can be swapped with the RBI at the option of the bank at a concessional rate of 100 basis points below the ongoing swap rate prevailing in the market.

The scheme was open up to 30 November 2013.

Basically, bankers told RBI, that they would bring plenty of dollars in as 3-year FCNR deposits, which was then converted to rupees and invested in India.

In return, the banks demanded a cheap rate at which they were converting the rupees back into dollars. As long as, RBI was trusted in delivering the forward dollars, such was a great deal for the banks, as the lenders got rupee interest income and guaranteed cheap price for swapping the matured domestic currency.

This was not an easy decision to make, as it had its own pros and cons. There was not even any guarantee that rupee will appreciate once the move takes place.

RBI in its biography as RBI governor, revealed about 2013 dilemma, where he mentions that, if we did not move the rupee back to fundamental value, every one-rupee rise in the dollar-rupee rate would costs us Rs 40,000 crores more in import costs. Assuming the rupee was undervalued by Rs 3 for a couple of years, this would mean a loss of lakhs of crores to national income.

Having obtained the concurrence of the finance ministry, the Rajan had to decide, and he chose to go ahead with it.

The FCNR scheme drew in $26 billion, more than any one could anticipate.

With this, the confidence picked up, the rupee strengthened beyond when the money came in. This was also because global investor mood as well as Indian electoral projections also changed, and RBI covered our forward swaps cheaply.

In fact, the Indian rupee became one of the most stable emerging market currencies for a while.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

08:17 PM IST

Currency market update: Rupee settles 4 paise lower at 83.96 against US dollar

Currency market update: Rupee settles 4 paise lower at 83.96 against US dollar Rupee rises to 83.49 against US dollar in early trade

Rupee rises to 83.49 against US dollar in early trade Rupee slips to end at 83.52 vs dollar

Rupee slips to end at 83.52 vs dollar  Rupee slips to end at 83.52 vs dollar on Wednesday

Rupee slips to end at 83.52 vs dollar on Wednesday Currency Market News: Rupee opens on a flat note at 83.50 vs dollar

Currency Market News: Rupee opens on a flat note at 83.50 vs dollar