RBI monetary policy review: Central bank hawkish, but no hike yet, says HDFC Bank report

"There are global factors that the RBI needs to watch out for, and perhaps act during phases of extreme volatility. Rupee movement in 2018 is likely to be marginal in our view but it’s important to keep a tad of exchange rate risks in an environment of tightening monetary policies globally and rising concerns of a full blown trade-war. Therefore, a status-quo for the major part of the year is the most likely scenario for the RBI. The rate hike could happen in the last quarter of FY19," said the HDFC Bank treasury research report.

The Reserve Bank of India (RBI) is likely to keep the repo rate unchanged at its upcoming monetary policy review on April 5th. Despite downside surprises in the recent inflation readings, the Central Bank is likely to stay hawkish on account of two factors. One, there could be caution related to higher Minimum support prices (MSPs) that the government could offer to farmers in line with its budget ‘commitment’s and because of surging oil prices. Second, core inflation has become more broad-based and is markedly high for categories like services, said HDFC Bank treasury research paper today, adding that increase in components of salaries (like housing allowance) due for employees of the state governments could add to these pressures.

"We would also parse the commentary carefully for the RBI’s assessment of global risks such as an economically costly trade war between the US and its major trading partners, comments from the White House on dismantling or diluting trading arrangements like NAFTA, regulatory push-backs in industries like tech on the back of the recent controversy on data leaks, and finally geopolitical tensions with Russia and China (likely to flex their muscles) and the US taking a harder line on Iran and North Korea," said the paper, while adding that this may or may not directly lead to a change in monetary stance, but the central bank’s view on how prepared the domestic economy and markets are to face these risks become important.

The report said that change in the outlook of oil prices and emergence of new risks on the international front (trade-war etc.) could have a direct bearing on our exchange rate assumptions as well, and added, "We no longer expect the marginal degree of appreciation (Q2 vs. Q1) that we had previously pencilled in. We now expect the USD/INR pair to trade in the range of 64.5 – 65.5 in the short term."

A-Inflation Dynamics

In the February meeting, the RBI had revised its inflation forecast for the fourth quarter (2017-18) to 5.1% from 4.3%-4.7% earlier. Inflation print is now expected to be lower than the RBI’s estimate in Q4 (so far the average has been 4.8%).

Going ahead in FY19, CPI inflation could inch-up to around 5.6% in June. HDFC Bank said that it expects average inflation of 5.1% in H1-FY19 with much of the rise likely to be on account of an adverse base. Thereafter, in 2H-FY19, while the base effect could be favourable and lead to some moderation in inflation, a lot would depend on how other factors pan out. Price of crude oil, potentially higher minimum support prices, the impact of housing rent allowance increase by several state governments, besides the performance of monsoon are some risks that could emerge in 2H-FY19, warranting a reasonable degree of caution by the RBI, the report added.

Given the recent softer inflation prints while the RBI can afford to wait longer and maintain status quo, eventually it could lead to a rate hike by the last quarter of 2018-19, explained the report. Upside risks to inflation are detailed below:

1. Core inflation pressures building up

Rising core: Core inflation (excluding food, fuel and petrol and diesel) has been sticky in the past three months, remaining unchanged at 5.1%. Prior to this, it had gradually risen from 3.9% in June 2017 to 5.1% in December 2017.

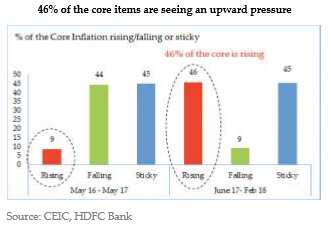

46% of the items in core are rising versus only 9% last year: Analysis shows that between June 2017 and February 2018, 46% of the core items have seen upward pressures while 45% of the items have remained sticky. Only 9% of the items have seen a fall. This is in contrast to the trend seen between May 2016 and May 2017, when only 9% of the core items were rising while 44% of the items where seeing a downward pressure.

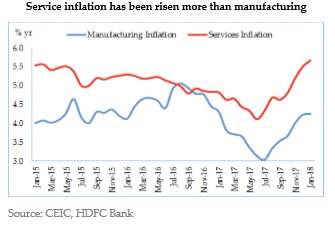

Services inflation is leading the upswing, rising to 5.7% in February from 4.4% in the beginning of the financial year (April 2017). This indicates that any downside pressures due to the introduction of GST on service prices, as was expected, has been offset by other core items or has not filtered through to retail prices.

2. Return of oil pressures: Crude oil prices posted their biggest weekly gain in eight months with rising geopolitical risk in the Middle East and Saudi Arabia hinting that the current OPEC output cuts could be extended into 2019.

MSPs risk: In the Union Budget 2018-19, the government had announced that MSPs will be set at 1.5 times the cost of production. The impact of this increase is dependent on the definition of cost used. The report says that according to estimates, a 1.5 times increase over the A2+FL costs could lead to a 5060bps increase in headline inflation. The RBI has also highlighted the increase in MSPs as a key risk in the past and are likely to reiterate the same in the April 5 policy meeting. That said, the RBI is likely to wait and watch before the final decision on MSPs is announced in May this year, before making changes to its stance or forecasts.

B-Global Dynamics

Change in the outlook of oil prices and emergence of new risks on the international front (trade-war etc.) could have a direct bearing on the exchange rate assumptions and thus on the overall monetary policy equation of the RBI.

Watch this Zee Business video on RBI

The report summed up saying "there are global factors that the RBI needs to watch out for, and perhaps act during phases of extreme volatility. Rupee movement in 2018 is likely to be marginal in our view but it’s important to keep a tad of exchange rate risks in an environment of tightening monetary policies globally and rising concerns of a full blown trade-war. Therefore, a status-quo for the major part of the year is the most likely scenario for the RBI. The rate hike could happen in the last quarter of FY19."

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

04:41 PM IST

RBI monetary policy review meeting commences, another pause in repo rate likely

RBI monetary policy review meeting commences, another pause in repo rate likely RBI launches key surveys to get inputs for monetary policy

RBI launches key surveys to get inputs for monetary policy LIVE UPDATES: RBI MPC Meeting June 2022: Monetary Policy Review Expectations - What will be outcome? Here is what experts say

LIVE UPDATES: RBI MPC Meeting June 2022: Monetary Policy Review Expectations - What will be outcome? Here is what experts say  RBI Monetary Policy Review Oct 2021 announcements: Who said what? How experts reacted to MPC decisions?

RBI Monetary Policy Review Oct 2021 announcements: Who said what? How experts reacted to MPC decisions? RBI Monetary Policy October 2021 Highlights: Interest rates unchanged; status quo maintained - Check top points from Governor Shaktikanta Das' MPC address

RBI Monetary Policy October 2021 Highlights: Interest rates unchanged; status quo maintained - Check top points from Governor Shaktikanta Das' MPC address