RBI Monetary Policy: CPI will ease, but a rate hike is still on table going forward

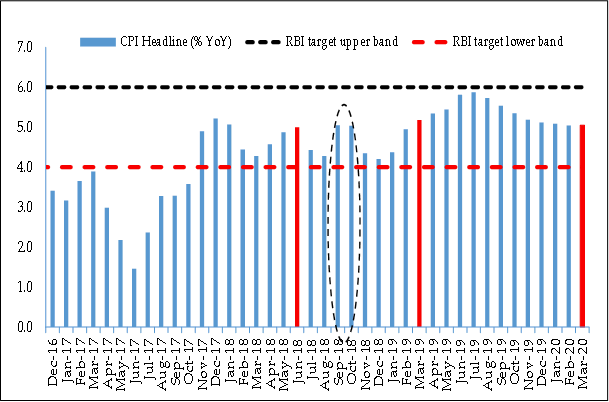

The reason behind the RBI repo rate hike was attributed to core inflation, which is at four-year high.

Over two policies now, India has seen a rise of 50 basis points in policy repo rate, with latest hike made yesterday by RBI in the third bi-monthly monetary policy for FY19. Now policy repo rate stands at 6.50% from previous 6.25%. With this, India’s policy repo rate has reached a two year high because the last time when 6.50% mark was achieved was in 2016 April policy. The reason behind the RBI repo rate hike was attributed to core inflation, which is at four-year high.

Abheek Barua, Chief Economist, HDFC Bank said, “The discussion on the possible increase in inflation early next year (Estimate of Q1 2019-20 to 5%) as well the assertion that policy rate changes impact the real economy with a lag (with a shorter lag in transmitting to lending rates) corroborates this.”

For RBI’s statements on increasing external risks and discussions on currency contagion (currency war) in the press conference, confirms Barau’s belief that the RBI is not in favour of excess depreciation and seems to want to hold on to a certain exchange rate level.

Barua explains, given the upside risks to inflation, discussed extensively, another policy rate hike cannot be ruled out. However, if there is an escalation in trade war risks and a resultant global output compression then the RBI could be prompted to stay on a prolonged pause.

According to HDFC Bank, RBI committed that liquidity conditions would be maintained close to the neutral level. This means the supply side pressures in the second half of this year could be offset by OMOs but it is unlikely that we will have any liquidity surplus. We expect OMO purchases to the tune of INR 800bn in 2018-19, including INR 300bn done so far.

Meanwhile, bond market seems to have reacted in a positive way to the rate hike (decline in 10 year yield by 6bps). This we believe is in response to the RBI’s commitment to keep the liquidity situation neutral instead of allowing the system to move into a large deficit.

Considering the above, Barau says, “We believe, that another rate hike is still on the table and as a result bond yields could continue to go up (after today’s relief rally). In this regard, it’s important to watch out for the inflation readings in September and October (which could be reflective of the impact of higher MSPs).”

He even reiterates that, even without a major uptick in inflation, the sheer supply of government bonds (states and centre) could keep the yields elevated.

Importantly, Barau pointed out so far only 20% of the budgeted borrowings for centre and state governments has been done with majority of the supply expected to come in the second half of the year.

Moreover, markets have reacted negatively on the rate hike with Sensex trading at 37,269.05 down by 252.57 points or 0.67%, whereas Nifty 50 below 67.85 points or 0.60% trading at 11,278.35 at around 1349 hours.

Even Indian rupee was trading at 68.475 above 0.160 points or 0.23% against US dollar benchmark.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

02:37 PM IST

Electricity distribution companies continue to remain a burden on state finances: RBI

Electricity distribution companies continue to remain a burden on state finances: RBI RBI imposes penalties on IndusInd Bank and Manappuram Finance for non-compliance of certain norms

RBI imposes penalties on IndusInd Bank and Manappuram Finance for non-compliance of certain norms Forex reserves drop $2 billion to $652.86 billion

Forex reserves drop $2 billion to $652.86 billion RBI flags rising subsidies by states as incipient stress

RBI flags rising subsidies by states as incipient stress Wholesale inflation eases to 1.89% in November from 2.36% in previous month

Wholesale inflation eases to 1.89% in November from 2.36% in previous month