RBI identifies 25% gross NPAs for insolvency; we bring pros and cons

RBI has made its move in bring 12 accounts under insolvency and bankruptcy code. How will banks cope up with this would be keenly watched, however we bring you pros and cons for the central banks decision.

Key Highlights

- Gross NPAs were at 9.5% of gross advances valuing up to Rs 7.65 lakh crore in FY17

- RBI identifies 12 accounts for resolution under IBC

- These accounts carry up to 25% of exposure of banks gross NPAs

The Reserve Bank of India (RBI) has formed a Internal Advisory Committee (IAC) on Tuesday and recognised 12 accounts for resolution under Insolvency & Bankruptcy code (IBC).

The IAC will focus on top-500 exposures in the banking system which are classified partly or wholly as non-performing assets (NPAs).

For accounts with more than Rs 5000 crore – where 60% or more exposure was already NPA by banks as on FY16 – immediate reference to resolution through IBC will be made. Thus a total of 12 accounts constituting of 25% of gross NPAs of banks will qualify for insolvency.

In case of other NPAs, banks are given six months time to agree upon a resolution plan. If a resolution is not provided by banks in this time, the banks should be required to file for insolvency proceedings under the IBC.

Specific directions will be issued by RBI to banks for identifying individual cases for filing under IBC. These cases will be accorded priority by the National Company Law Tribunal (NCLT).

The letter ended stating RBI is also going to issue revised provisioning norm for cases accepted for resolution under the IBC.

Performance of banks under IBC:

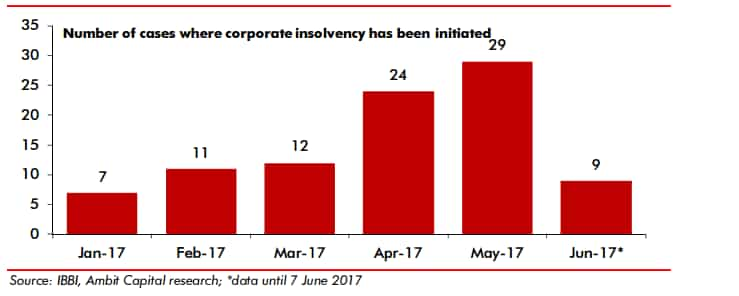

So far, there has been 92 cases filed since the IBC came into effect in December 2016.

Time period for completion of case has maximum limit of 180 days and can be extended further by 90 days. Both debtor or creditor can opt for this code.

Among this 92 - a total of 14 cases were filed by banks.

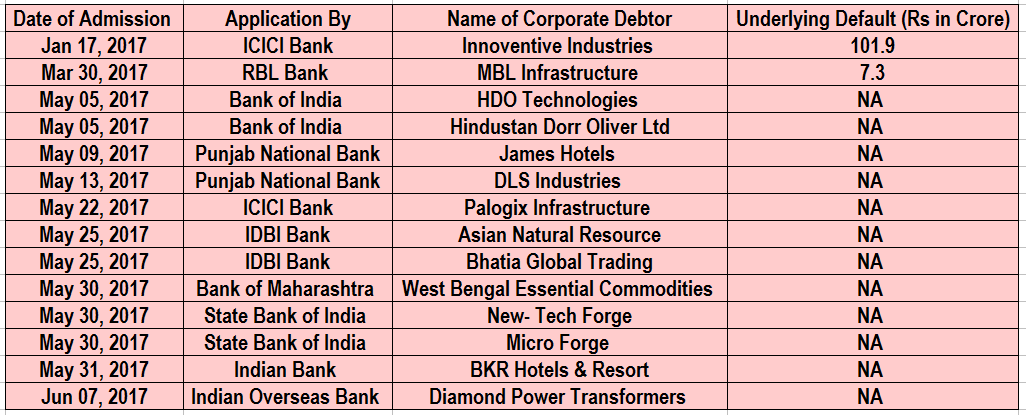

First insolvency was filed by ICICI Bank against Innoventive Industries of Rs 100 crore on January 17, 2017.

This was followed by Bank of India and RBL which applied for insolvency mechanism between March 30, 2017 – May 05, 2017.

Interestingly, it was only in May 2017 - more banks started coming in for insolvency. RBI was given more power under Section 35AA on May 05, 2017.

The problem in these banks insolvency cases was that they brought accounts of smaller cases and which were already NPAs for which banks have already made provisions.

After carrying a discussion with many experts, Ambit Capital stated out few reasons why banks have been shying away.

Firstly, there is a widespread misconception amongst the bankers that bankrupcty code is for liquidation of companies – which means lower recovery for them. Secondly, there is fear that liquidation value will be lower than the book value of the bad assets – which could lead to higher provisioning further. Lastly they are testing IBC with small cases and once process streamlined, they may bring in larger cases through this route

Now that RBI has tighten the screw for banks under the IBC, we bring few pros and cons.

Ambit Capital has highlighted few situation on banks and their assets after RBI identified 25% of gross NPAs.

Pros:

Experts believe resolution of stressed cases through IBC will mean higher rate of recoveries would be higher than what banks were experiencing so far under the much more protracted routes of NPA recoveries.

With RBI providing clarity and timelines around now, resolutions are likely to take place and in turn take corporate insolvency as a credible solution.

This move of RBI's reduces flexibility for Indian corporate lenders to deal with their large stressed cases and make them clean in a time manner rather than delaying and making provisions in a hope for favorable solution later.

Such decision will make corporate lenders to set aside significant provisioning for large stressed case which are being dealt either by Joint Lender Forum or IBC in next 6 – 12 months.

Discussion with insolvency experts by Ambit stated that expect a haircut of 50-60% under insolvency proceedings. Indian corporate lenders carry aggregate provision coverage of 37% on their bad loans.

On sector-wise performance, banks stare at a debt haircut of 50-80% in power, steel and road sectors.

Lenders will likely engulfed in clean-up of their balance sheet in next few years – this will lead the competitive landscape to be accomodative for banks with little exposure to stressed corporates, superior asset quality and stronger capital positions.

Cons:

While significant debt haircuts appear a certainty for banks, lack of information on banks' provisioning against specific large stressed cases and differing classification of these assets add uncertainty to banks earnings over 6 – 12 months.

PSU banks are particularly more vulnerable due to lower provisioning coverage on stressed assets and capital requirement there earnings will be volatile in near time. This would be the case of major lenders also like State Bank of India, HDFC Bank, Axis Bank, ICICI Bank, Yes Bank and Bank of Baroda.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

02:01 PM IST

Electricity distribution companies continue to remain a burden on state finances: RBI

Electricity distribution companies continue to remain a burden on state finances: RBI Rupee hits all-time low; RBI intervenes to curb further losses

Rupee hits all-time low; RBI intervenes to curb further losses Rupee slumps to record closing low of 84.88 vs dollar

Rupee slumps to record closing low of 84.88 vs dollar Bank stocks rally up to 2% after RBI cuts CRR to 4%

Bank stocks rally up to 2% after RBI cuts CRR to 4% RBI raises retail inflation estimate for FY25 to 4.8% amid rising food prices

RBI raises retail inflation estimate for FY25 to 4.8% amid rising food prices