Here's where GST, demonetisation took India's economy in one year of Diwali

Performance during Diwali festive season serves as a barometer of the health and strength of businesses and the Indian economy as a whole.

Generally Diwali festive is a period of consumption, investment and heightened economic activity in India.

India's domestic consumption driven economy which accounts mainly 56% of GDP – thus the demand and sales during Diwali plays an important role and dictate the performance of economic indicators for the year as a whole.

Interestingly, this year Indian economy has seen major structural changes in last one year of Diwali – not to forget the demonetisation move in November 2016 which was immediately after previous Diwali, followed by implementation of Goods and Services Tax (GST) on July 01, 2017.

Together these two changes in India have caused some disruptions on the demand and supply side.

Here's how key indicators of Indian economy has performed in one year of Diwali.

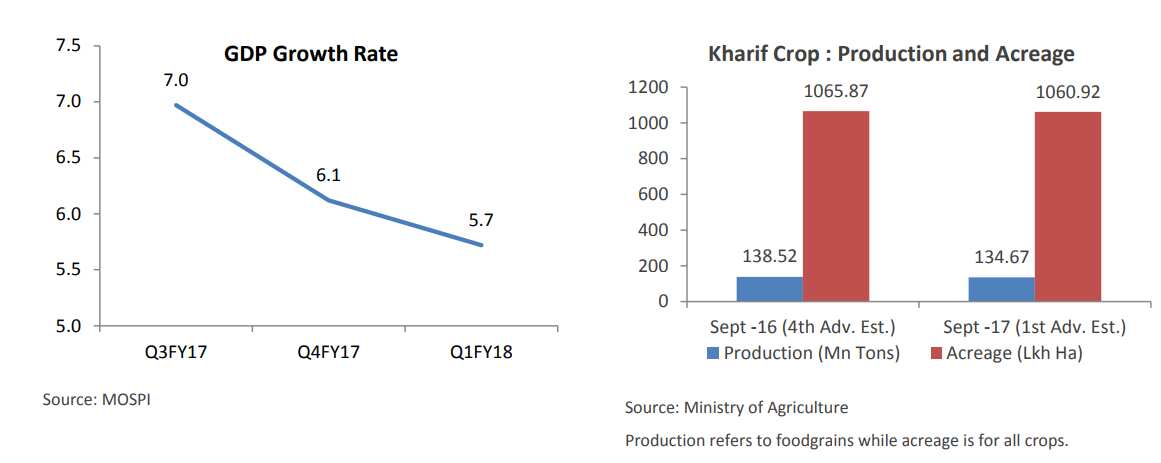

GDP Growth Rate:

Quarterly GDP growth has seen a sharp deterioration since Q3 FY17 and have reached at three-year low of 5.7% in first quarter of FY18 (Q1 FY18).

Decline in GDP in the last 3 quarters can be largely attributed to the demonetization and GST related disruptions. Government has been the leading sector in Q1-FY18. Peformance across sectors has moderated in recent quarters.

Agricultural output in FY18 could be lower than that last year. The kharif output for FY18 as per the 1st advance estimate is 3% lower to 134.67 million tonnes till September 2017 – compared to 138.52 million tonnes a year ago same period.

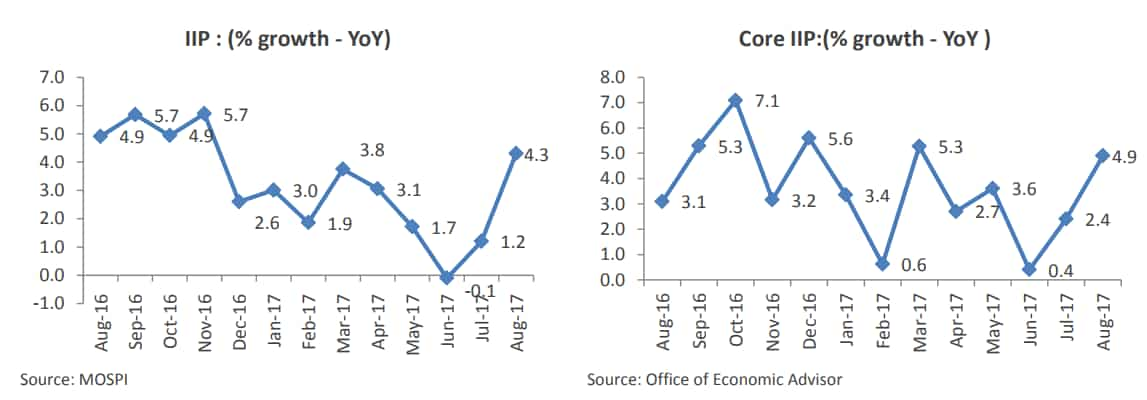

Index of Industrial Production:

Factory output or IIP growth declined to 2.6% in December 2016 (following demonetisation) from 5.7% in November 2016. Decline in IIP continued from March 2017 after the base effect of this indicator was changed to 2011-12.

However, IIP surged in August 2017 to 4.3% from 1.2% of July 2017 – mainly attirbuted to the post GST restocking. August 2017 numbers are still lower compared to 4.9% a year ago same month.

Consumer Price Index:

Retail inflation has been showing mixed pictures in last one year- It did tumbled to 3.2% in January 2017 after demonetisation move ended on December - but also saw consist decline from March 2017.

Inflation has firmed by over 2% since Jun’17, driven by the increases in non-food items viz. housing, transport, clothing etc.

On the other hand, core inflation has been rising and draws attention to the price pressures in the economy. CPI inflation however continues to be lower than the RBI’s target rate of 4%.

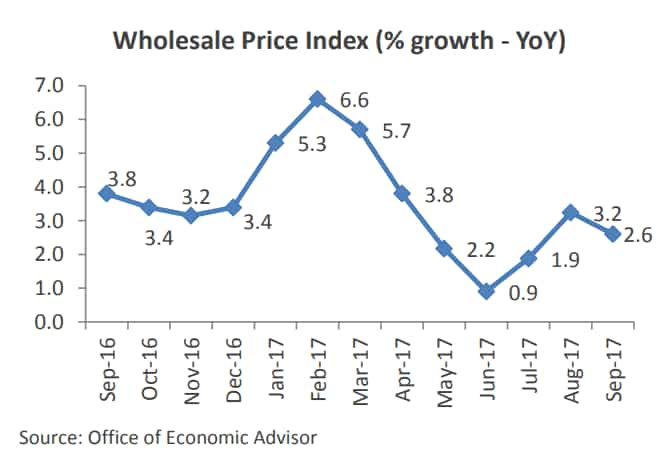

Wholesale Price Index:

Latest number of WPI came in at 2.6% in September 2017 – lower by 3.8% from previous year same month. WPI reached to its slowest pace in more than five year at 0.9% in June 2017.

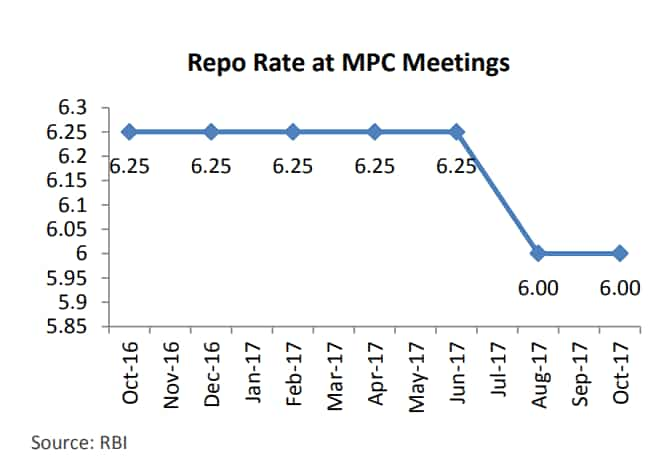

Policy Repo rate:

India's policy repo rate stands at 6% which is lowest since 2010. From October 2016 – June 2017, policy repo rate under liquidity adjustment facility (LAF) were kept unchanged at 6.25% by the monetary policy commitee (MPC) team.

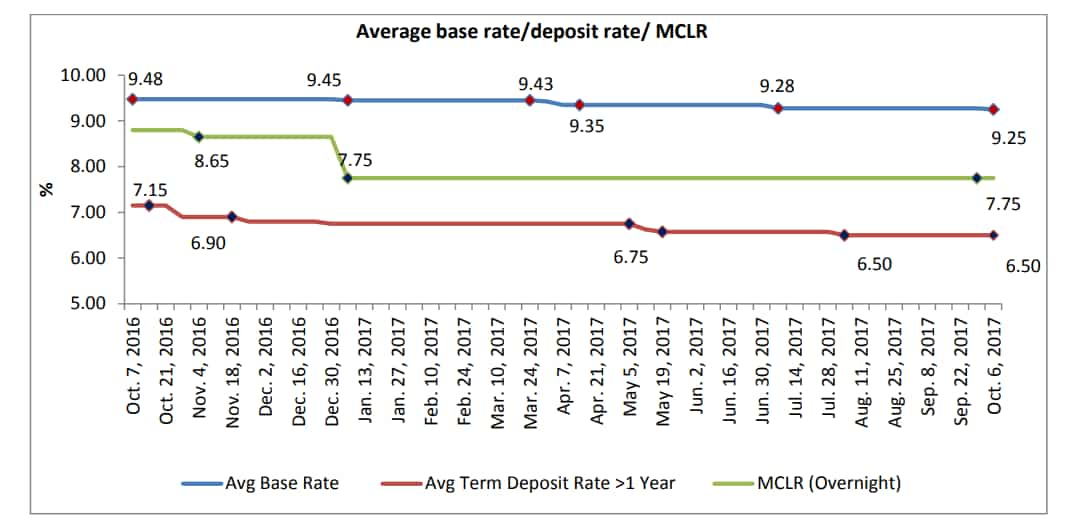

MCLR, Average Base rate:

Although the RBI has cut policy rates, banks have been slow in transmitting the rate cuts to their borrowers.

Where MCLR rates have come down by 90 basis point to 7.75% by October 06, 2017, from 8.65% of October 2016, the average base rate just been lowered by 23 basis points in one year by banks.

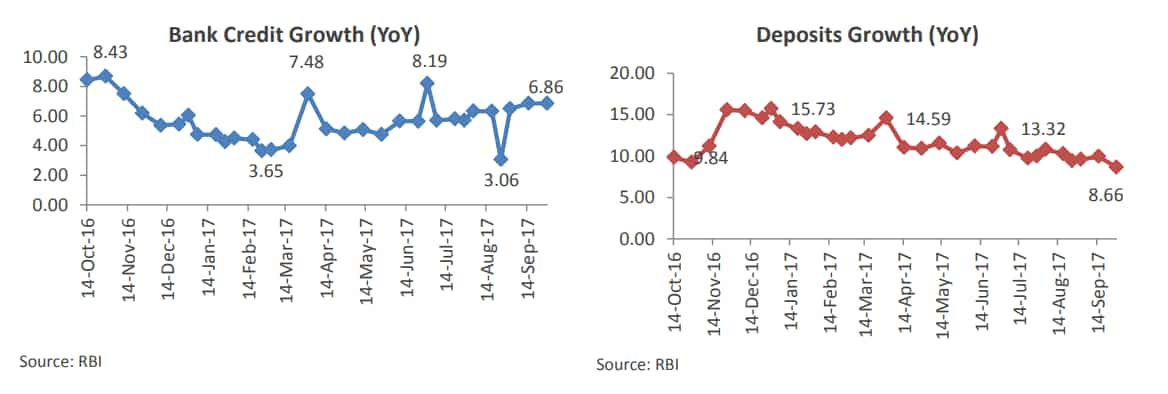

Banks credit and deposit growth:

Bank credit growth saw a sharp decline immediately after demonetization. It has been lackluster since the beginning of the fiscal with credit offtake across sectors being low/weak. The growth in bank credit continues to be led by retail loans.

While deposit growth has moderated/normalized since then. The recent moderation can in part be attributed to the growing investor preference for other financial instruments/markets that offer higher returns viz. mutual funds.

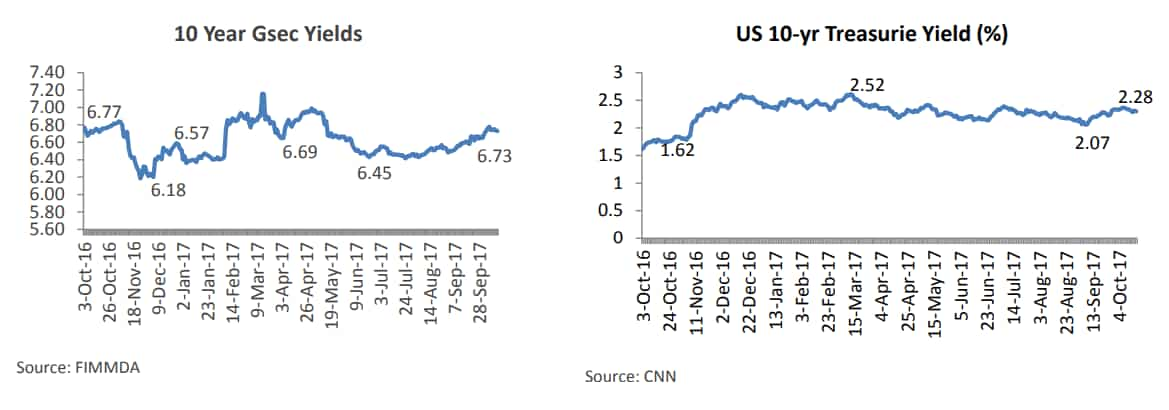

GSec yields:

Surplus liquidity in the banking system has lowered the yields of GSecs. Yields have risen since Sept’16 with firming inflation that lowers the chances of further rate cuts by the RBI.

US Treasuries yields have risen in the last 12 months with the US Federal Reserve raising interest rates (Mar’17 and Jun’17) and moving toward unwinding/unloading its portfolio of bonds that it has accumulated since the financial crisis of 2008.

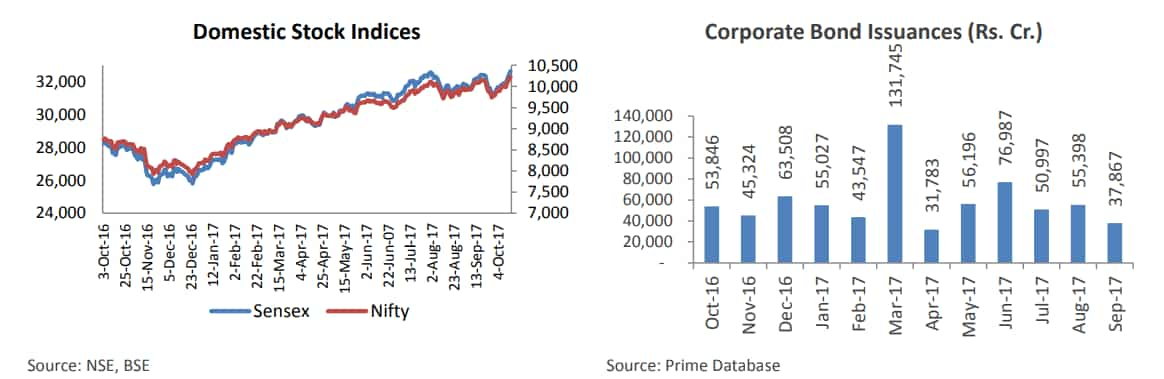

Benchmark equity indices and corporate bonds:

Benchmark equity indices have seen a sharp rise since Nov’16 and have touched record highs, driven mainly by higher domestic investments chiefly by DIIs (domestic institutional investors) in the stock markets.

Corporates have been increasingly tapping bond markets for their funding needs given the stress in the banking system that has been curtailing bank lending. However, it stood at Rs 37,867 crore by end of September 2017 – lower from Rs 55,398 crore of previous month.

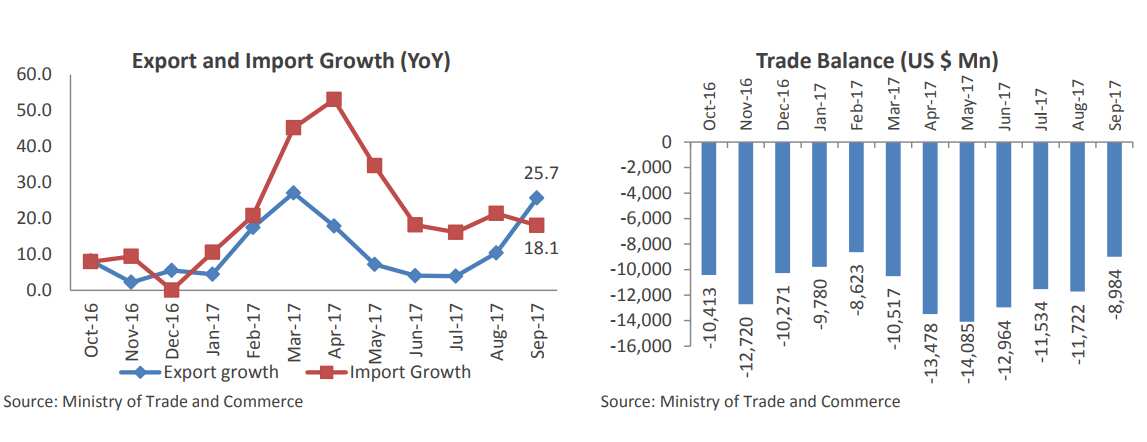

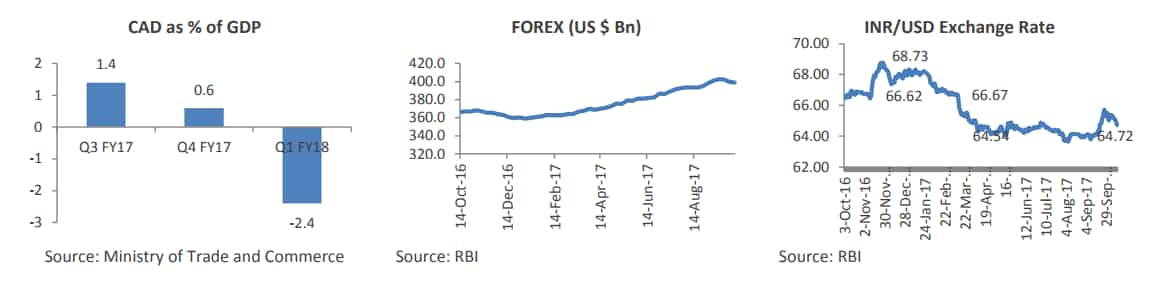

Trade balance and Current Account Deficit (CAD):

Imports have been growing at a higher rate than exports in recent months, widening the trade balance.

Imports grew by 28% in H1 FY18 and exports by 8% in H1 FY18.

Trade deficit has narrowed to its lowest in last 7 months in Sept’17. The widening trade balance has been pressuring the current account deficit which has risen in FY18.

Forex reserves have risen to record levels (over $ 400 bn) driven by the rise in foreign inflows. This has led to the appreciation in the rupee. The present level is almost Rs 4 lower than the peak witnessed in Nov-Dec.

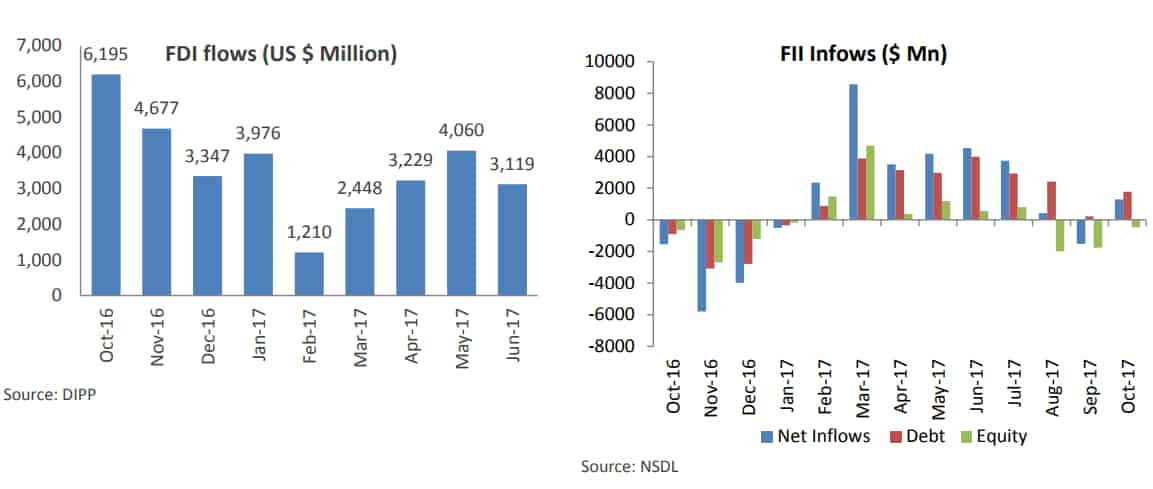

FDI inflows:

FDI inflows have been lower since Nov’16. The inflows aggregated $28 billion during the 7 month period Apr-Oct’16. FDI inflows were $22 billion for the subsequent 7 months i.e. Nov- May’17.

FII inflows have predominantly been in the debt segment and have been driven by the yield differentials between domestic debt securities and those of other global markets coupled with the fairy stable currency. Since Mar’17, debt inflows have totaled $21.3 billion, compared with the net outflows of $ 6 billion during Oct’16-Feb’17.

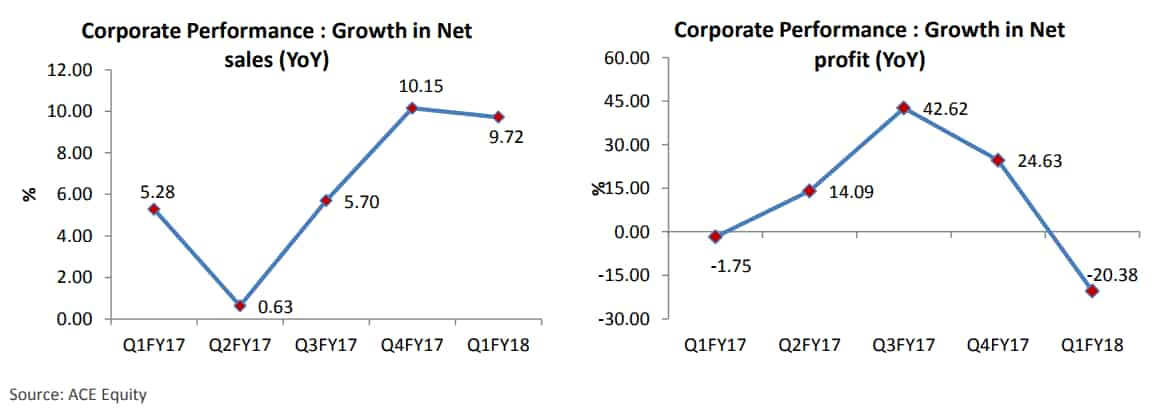

India Inc performance:

Corporate performance based on the sample of 3,102 companies (including banks and oil companies) indicated a growth of 10% in net sales in Q1FY18 - 5% higher than the growth registered in the corresponding period last year.

However there been a contraction of (-) 20% in net profits during Q1FY18 (highest in the last 5 quarters) compared with the growth of 25% witnessed in the preceding quarter (Q4 FY17).

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

03:27 PM IST

Post-Chhath travel rush: Railway’s special arrangements as station crowds surge

Post-Chhath travel rush: Railway’s special arrangements as station crowds surge Delhi's air quality deteriorates to 'very poor' on Diwali

Delhi's air quality deteriorates to 'very poor' on Diwali  PM Modi celebrates Diwali with armed forces near Indo-Pak border in Kutch

PM Modi celebrates Diwali with armed forces near Indo-Pak border in Kutch  Diwali 2024: Easy tips to take best photos with your smartphone this festive season

Diwali 2024: Easy tips to take best photos with your smartphone this festive season Diwali 2024: From smartphones to smartwatches, best tech gifts for this festive season

Diwali 2024: From smartphones to smartwatches, best tech gifts for this festive season