Guess what! New villain is in town, RBI may hike key rate by 50 bps despite inflation cooling

CPI inflation came in at 3.69% during the month of August 2018 lower compared to 4.17% of the previous month, but that is not likely to comfort the RBI.

With the India’s consumer price index (CPI) or retail inflation cooling off for second consecutive month, all eyes have now shifted to RBI. The central bank will be presenting the country’s fourth monetary policy for fiscal year FY19 soon. Looking at the CPI numbers for latest month, markets would be expecting a status quo this time from RBI, which has increased the policy repo rate by 50 basis points in past two policies. However, looks like the status quo dilemma is still not in picture, because the RBI’s new problem has just gotten worse and if it continues, you never know, the central bank may well make a massive 50 basis point rate hike in the upcoming policy!

CPI inflation came in at 3.69% during the month of August 2018 lower compared to 4.17% of the previous month. However, the latest number was slightly higher compared to 3.28% in the same month of previous year.

This easing was primarily on account of low food inflation which came in at 0.29% versus 1.3% YoY last month. Core inflation, which has been a cause of concern for RBI, also moved to 5.9% this month compared to 6.3% YoY last month aided by dissipating HRA impact from the housing index, fall in inflation in sin goods and personal care and effects services, even while education and transport services saw continued upside movement.

source: tradingeconomics.com

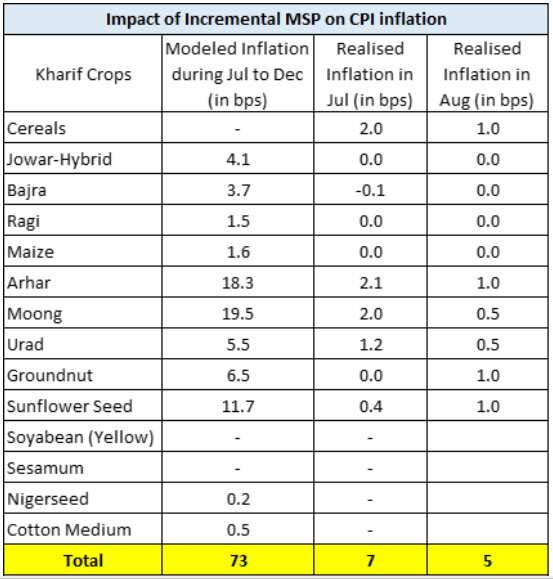

Even the MSP hike who has given RBI sleepless nights in deciding India’s monetary policy, has also not impacted inflation that much.

A research note of SBI says, “We estimate that the realised value of MSP Direct Pathfinder during Jul’18 was 7 bps and for Aug’18 it was 5bps, hence the combined impact is now 12 bps. The realization of MSP Indirect Pathfinder will however take time.”

Sure, the CPI numbers do indicate that RBI should maintain a status quo, because it is well within its target for second half of FY19.

RBI has projected inflation at 4.6% in Q2, 4.8% in H2 of 2018-19 and 5% in Q1:2019-20, with risks evenly balanced. Excluding the HRA impact, CPI inflation is projected at 4.4% in Q2, 4.7-4.8% in H2 and 5% in Q1:2019-20.

Despite inflation coming down, RBI may still go in for a tightening and this time it is the Indian rupee that has turned to be the new villain. Indian rupee has depreciated by 12.3% so far this year against the dollar. This week, the rupee has even touched a new low of over 73-mark.

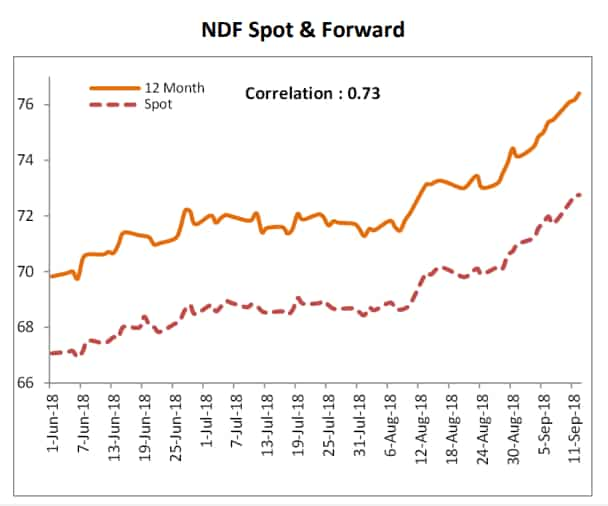

Dr. Soumya Kanti Ghosh, Group Chief Economic Adviser at SBI said, “The value of Rupee in NDF 12-month forward market has already touched 76 and the strong and positive correlation (0.73) between spot and forward NDF rate indicate that rupee is still under pressure though it has rebounded.”

As per Ghosh, we believe that in the hope of a better export growth, talking down the rupee as was done recently by officials (but later reversed) when the markets were volatile has been counterproductive and thus the pace of depreciation picked up at frantic pace in the last week or so.

It is noteworthy, that RBI’s intervention in the foreign exchange market recently have been limited given the costs associated with such moves.

Therefore, Ghosh says, “We believe October rate hike of 25 bps is imminent, but the question is whether the magnitude of rate hike could be even higher by 25bps (say 50 bps).”

In Ghosh’s views, a currency crisis by logic calls for an bigger rate intervention, but given that RBI is an inflation targeting central bank, it will be really difficult to justify such action with inflation numbers continuing to be in 4.-4.7% range through current fiscal, with the downside at sub 3.5% in November’18. Clearly, the RBI is now caught between Scylla and Charybdis!

Similar projections were from ICICI Bank. According to the private lender the headline CPI inflation is seen to average 4.7% by FY2019 with core inflation averaging at 5.8%.

Upside risk in CPI continues in the form of input cost pressures and closing of the output gap putting upward pressures on core, fears of food inflation (driven by MSP increases) feeding into inflationary expectations and recent volatility in the Rupee feeding into fuel prices and second round impact of the depreciation.

ICICI Bank says, “Given the recent volatility in the INR since the August policy - seeing a depreciation of 5.2%, recovering partially today (12th September 2018) on account of expectations of a combination of policy measures to be announced by the government soon, monetary action in terms of a rate hike cannot be ruled out.”

Following the ICICI Bank lastly mentioned, “We had originally expected the MPC to pause in October as the inflation trajectory currently looks fairly benign. However, if the pressure on the currency were to continue, then October hike of 25-50 bps is certainly on the cards and we feel that it is time that the MPC also changes its stance from “neutral” to “withdrawal of accommodation”.

Hence, ruling out a rate hike stance is not in picture anymore because of Indian rupee. How, the domestic currency goes ahead and how RBI decides to take policy stance in these midst will be keenly watched.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

12:41 PM IST

Electricity distribution companies continue to remain a burden on state finances: RBI

Electricity distribution companies continue to remain a burden on state finances: RBI RBI imposes penalties on IndusInd Bank and Manappuram Finance for non-compliance of certain norms

RBI imposes penalties on IndusInd Bank and Manappuram Finance for non-compliance of certain norms Forex reserves drop $2 billion to $652.86 billion

Forex reserves drop $2 billion to $652.86 billion RBI flags rising subsidies by states as incipient stress

RBI flags rising subsidies by states as incipient stress Wholesale inflation eases to 1.89% in November from 2.36% in previous month

Wholesale inflation eases to 1.89% in November from 2.36% in previous month