Can a home loan push help banks revive credit growth?

Banks credit growth continues to remain at a historic low. It stood at Rs 69.45 lakh crore in July 2017 – recording growth of just 4.7% year-on-year (YoY) basis.

Key Highlights:

- Bank credit growth at Rs 69.45 lakh crore in July 2017

- Personal loans remain at double-digit growth of 15% in the same month

- Housing loan is expected to boost banks credit demand in future ahead

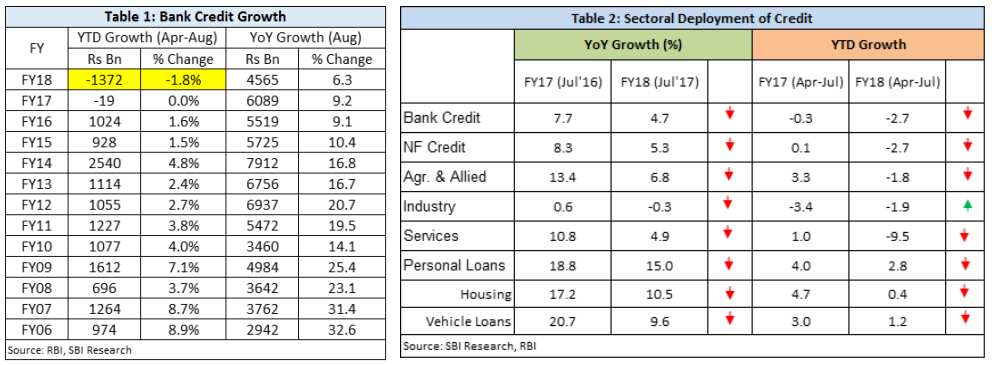

All Scheduled Commercial Banks' (SCBs) credit growth continues to remain at historic lows. Recent data compiled by the Reserve Bank of India showed this gross lending by banks stood at over Rs 69.45 lakh crore in July 2017 – recording growth of just 4.7% year-on-year (YoY) basis.

In the same month of previous year – SCBs gross lending was at Rs 66.32 lakh crore but the growth was higher at 7.7% yoy.

Interestingly, data compiled by State Bank of India indicated that between April 2017 – till August 2017, bank credit growth tumbled by over Rs 1.37 lakh crore down 1.8% as against the similar period of the previous year.

Soumya Kanti Ghosh, Group Chief Economic Adviser at SBI said, "The deceleration in credit growth also highlights the role of supply side factors – stressed assets and capital constraint – in hindering a revival in the credit cycle. The sectoral data on flow of credit indicate that deceleration in credit, though broad-based, is characterised by a sharp contraction in exposure to industry."

Almost all indicators in bank credit growth as per RBI's data saw sharp deceleration in the month of July 2017 – except credit to industry where performance entered the territory of -0.3% from gradual improvement of 0.6% a year ago.

Credit to agriculture and allied sector tumbled to 6.8% (from 13.4% in July 2016) and services sector to 4.9% from 10.8% growth in July 2016.

Only personal loans managed to stay at a firm double-digit growth of 15%, however, still lower compared to 18.8% in the similar month of the previous year.

Credit cards outstanding recorded a whopping 32.5% growth to Rs 56,800 crore versus Rs 42,900 crore in the same month of previous year – rowing 29.4%.

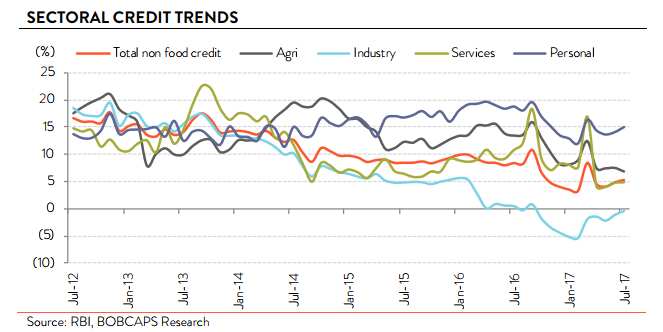

Clyton Fernandes and Abhijay Thacker analysts at BOBCAPs said, "The runaway winner of the year has been credit cards, growing at 32.5% YoY in July. This reflects greater appetite in the unsecured segment. The lion’s share of credit demand continues to arise from housing.”

Share of credit cards and other personal loans in incremental credit has spiked from 34% to 58%, at the cost of a near mirror slide in the share of housing, from 50% to 38% over the past year.

Housing loans account for 12% of overall bank credit growth.

Performance of housing loans have been volatile since the start of 2017. In percentage terms, credit to housing which stood at 13.5% yoy growth in January 2017 have now reached to 10.5% growth in July 2017.

In this past seven months – credit in this sector was only highest in March 2017 – were it clocked 15.2% yoy growth.

This can come as a surprise considering banks have been consistently trimming down home loan rates. Currently most of the banks are charging home loan rates at 8.35% per year.

Housing loans which was over Rs 8.21 lakh crore in January 2017 increased to Rs 8.60 lakh crore in March 2017 and further to Rs 8.64 lakh crore in July 2017.

After demonetisation, analysts now estimate that credit growth may reach 10% by FY18 due to performance of housing loans.

According to ICICI Securities, retail credit demand of banks are expected to be driven by home loans, given the increased affordability on falling product rates, favorable demographic drivers (nuclear families, internal migration) and government incentivisation (upfront interest subvention in affordable housing).

Rohit Inamdar, Group Head Financial Sector Ratings, ICRA, “The growth in the sector was impacted by a slowdown in new project launches and buyers and investors deferring their home purchase decisions in expectation of a decline in real prices. In addition disruptions in the real estate market owing to implementation of Real Estate Regulation and Development Act (RERA) and; Goods and Service Tax (GST) and preference of end users for finished inventory /RERA approved projects also resulted in a slowdown.”

Yet ICRA still believes that despite the slowdown in housing loans, it long term prospects look favourable.

Outlook for this sector has always been considered positive due to various moves taken by the Reserve Bank of India (RBI) and banks.

Among latest one is RBI's housing finance committee recommending banks to quote loans to customers using the RBI repo rate rather than based on their own MCLR rates. This means that every floating rate home loan to prospective borrowers in the form of a market-wide standardised rate plus spread as opposed to MCLR plus spread.

This would boost demand for more home loans as at present the policy benchmark repo rate stands at 6% while MCLR is hovering around below 9%.

Dhaval Kapadia, Director - Portfolio Strategist, Morningstar said, "If banks transmit the lower rates to borrowers it could result only in a slight improvement in consumption demand, since the rate reduction by Banks and other lenders might be limited to 10 to 20 basis points.”

Apart from this, RBI has taken measures like maintained the Statutory Liquidity Ratio at 20% and also reduced risk-weights and loan to value (LTV) ratios boosting the demand further.

Chanda Kochhar, MD and CEO, ICICI Bank, said, "The SLR cut and reduction in risk weights for housing loans are positive moves that will support bank liquidity and encourage growth in housing loans.”

ALSO READ:

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

10:33 AM IST

Banks' credit to industry grows by 8% in October, as per RBI data

Banks' credit to industry grows by 8% in October, as per RBI data  RBI's decision will support growth, check inflation: Experts

RBI's decision will support growth, check inflation: Experts RBI Survey: Bankers highly optimistic about credit demand across sectors

RBI Survey: Bankers highly optimistic about credit demand across sectors Bank credit growth accelerates to 14% in Q1 despite hike in lending rates: RBI data

Bank credit growth accelerates to 14% in Q1 despite hike in lending rates: RBI data Bank credit offtake is expected to pick up following normalisation of economic activities

Bank credit offtake is expected to pick up following normalisation of economic activities