Lemon Tree Hotels IPO: No juice in valuations, but turnaround seen; should you subscribe?

Lemon Tree Hotels IPO: Lemon Tree is one of the largest hotel chain in the mid-priced hotel sector and one of the most cost efficient players in the segment. However, despite being operationally & capex efficient and occupancy of over 70 per cent in each of it’s brands the company has low RoCE.

Lemon Tree Hotels IPO: The initial public offering (IPO) of Lemon Treet Hotels hit the primary market on Monday to raise around Rs 1,040 crore in the price band of Rs 54 and Rs 56. With valuations fixed at higher end, analysts are not so gung-ho on the IPO with most of them recommending 'avoid' on the issue.

The IPO of the hospitality chain raised Rs 311 crore from anchor investors on Saturday. The company has allotted 5,56,43,820 shares to 18 anchor investors at a price of Rs 56 per scrip, garnering Rs 311.61 crore. Among the anchor investors are SBI Magnum Balanced Fund, DB International Asia, HDFC Small Cap Fund, Aberdeen Asian Smaller Companies Investment Trust Plc, BNP Paribas Arbitrage and Alpine Global Premier Properties Fund.

Lemon Tree Hotels IPO comprises sale of up to 18,54,79,400 equity shares by the existing shareholders, including Maplewood, Whispering Resorts, Palms International and RJ Corp.

The issue will close on March 28.

Here's what analysts recommend on the issue:

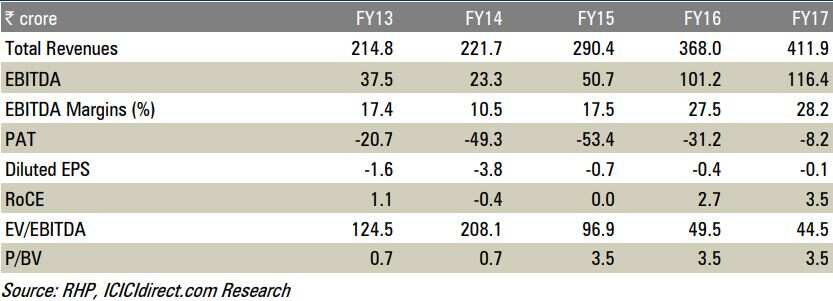

ICICI Securities:

Lemon Tree is one of the largest hotel chain in the mid-priced hotel sector and one of the most cost efficient players in the segment. However, despite being operationally & capex efficient and occupancy of over 70 per cent in each of it’s brands the company has low RoCE. This is mainly due to high capex oriented nature of expansion, which has kept its turnover ratios lower (at 0.2x). Further, although the EBITDA margin has improved from 17.4% in FY13 to 28.2% in FY17 leading to robust operating cash flow generation, the FCFF has remained negative. Going forward, considering the company intends to expand through owned hotels, we expect the capex intensity to remain higher. This will impact FCFF generation. In addition, with higher share of B2B segment and higher competition from branded and unbranded hotels, we believe there is limited room for ARR upside. Further, the company’s current valuation of EV/EBITDA of 44-46x is at 25-30%, higher than comparable peers. Hence, we have an AVOID rating on the offering.

Angel Broking:

Lemon Tree has seen turnaround in M9FY2018 by posting a PAT of Rs 2.9 cr which was achieved at sort of peaked occupancy and 9 per cent price hike (taken after September 2017). Hence, any further improvement in margins have to largely come via price hikes, which looks difficult specially in the lower range hotels, amid intense competition. At the upper end of the price band, the EV/EBITDA multiple works out be 44.5x EBITDA of FY2017 and ~38.6x on its FY2018 annualized EBITDA, which appears on the higher side even when compared to large listed hotel players like Indian Hotels (available at 33x FY2018 EV/EBITDA, others are available at 20-25x). We recommend ‘Neutral’ on the issue for a mid-to-long term period.

Gaurang Shah, Geojit Financial Services

We would not recommend investing in this IPO as the hospitality industry has seen underperformance lately. Overall market sentiment is negative too, which would impact the listing gains.

Key financials

Over FY13-17, revenues and EBITDA have grown at a CAGR of 17.7 per cent and 32.7 per cent, respectively.

Key positives:

- Emerged as the leading mid-priced hotel chain in a short span of 14 years

- Positive hotel industry dynamics with mid priced room demand

- Expected to grow 11% CAGR ahead of supply till 2022

- Differentiated business model in terms of property development ( 65% owned properties), employee selection specially the inclusion of opportunity deprived Indians, including differently-abled individuals

- Well-diversified geographical location of hotel properties

- Additions of new hotel properties will help in sustaining robust revenue growth in future.

Key risks:

- Heavy capex has negatively impacted FCFF generation

- Potential dilution of shareholding in subsidiaries (Carnation)

- Limited room of average room revenue (ARR) growth

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

11:08 AM IST

Lemon Tree Hotels IPO kicks off on March 26; here are the details

Lemon Tree Hotels IPO kicks off on March 26; here are the details  Lemon Tree Hotels IPO soon; CMD Patanjali Keswani has unusual take on shareholders

Lemon Tree Hotels IPO soon; CMD Patanjali Keswani has unusual take on shareholders