ICICI Lombard's IPO is now open: What should you do?

ICICI Lombard plans to raise about Rs 5700 crore from its IPO issue - which would be biggest issue after ICICI Prudential's Rs 6,000 crore IPO last year and Coal India's Rs 15,000 crore IPO in 2010.

Key Highlights:

- ICICI Lombard to offer 8.62 crore equity shares in IPO

- Price band for ICICI Lombard fixed between Rs 651 - Rs 661 per share

- ICICI Bank to sell 7% and Fairfax 12% stake in ICICI Lombard

ICICI Bank has once again have entered the initial public offering (IPO) market on Friday with its non-life insurance arm ICICI Lombard General Insurance. This issue is open for subscription and will be available till September 19, 2017.

In this IPO, ICICI Lombard is offering a total of 8.62 crore equity shares in a move to raise about Rs 5,700 crore. Of the total equity shares - ICICI Bank is selling 3.18 crore shares (7%) and Fairfax 5.45 crore shares (12.0%). Of the total issue, ~43 lakh shares are reserved for the shareholders of ICICI Bank.

Price Band for this issue has been fixed at lower end of Rs 651 per piece and upper end of Rs 661 per piece.

50% of the total shares offered are held for qualified institutional buyers (QIB), while 15% has been kept aside for non-individual investors (NII) and remaining 35% for retail institutional investors (RII).

Book Running Lead Managers (BRLM) for this issue were companies like ICICI Securities, Bofa Merrill Lynch, IIFL Holdings, CLSA India Private Limited, Edelweiss Financial Services and JM Financial Institutional Securities.

On September 14, 2017, ICICI Lombard raised nearly Rs 1625 crore from somewhat 64 anchor investors by alloting them 2.45 crore equity shares at the upper price band of Rs 661 per share.

Should you invest in ICICI Lombard's IPO issue?

Firstly, ICICI Lombard has a first-mover advantage among private players in the non- life insurance sector to begin listing process.

The company holds a little over 8% of the non-life insurance market where only 30 companies are present at the moment.

Jignesh Shial, analyst at Quant Broking said, “We continue to believe that ICICI bank, promoter of the company, being saddled with large delinquencies and elevated credit costs is forced to dilute its holding in the company.”

Shial added, “The Company has announced a price band of Rs 651-661 corresponding to ~39x P/FY17 Earnings and ~8x P/FY17 book. Although we surely believe that this is an expensively priced issue however considering first mover advantage to the company along with its market leadership underpenetrated industry and healthy growth opportunities, the valuation is justified.”

Analysts at NVS said, “On the basis of improving macro-economic factors and increasing insurance awareness in India, ICICI Lombard has a huge potential to increase its market share and grow in the nonlife insurance space."

They added, “We are confident that the Insurer will deliver consistent performance and provide an excellent investment opportunity for investors with a long term horizon. We recommend all investors to SUBSCRIBE.”

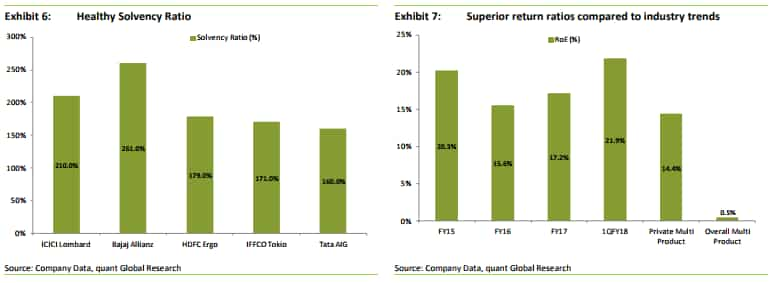

Prabhudas Lilladher giving 'subscribe recommendation', also expects ICICI Lombard's Return on Equity (RoE) to remain strong in the range of 18‐20% on high investment income and better operating efficiency.

Payal Pandya and Siddhartha Khemka, analysts at Centrum Wealth Research said, "Even if money raised at such valuations was flowing into the company, it would have ultimately belonged to shareholders. But in this case 100% of the money raised is going to the selling shareholder and not into the company."

The duo added, "ICICIL may attract adequate investor interest as it is the first general insurance listing, the under-penetration in the sector and the company’s healthy financials. If so, the stock may list at premium to the issue price. If that does not happen, than investors should be ready to expect returns only in the long term.”

Analysts from Adroit Financials, Stallian Asset, Edelweiss Financial Services and SMC too agree on the strong business portfolio of ICICI Lombard and have given thumbs up to its IPO.

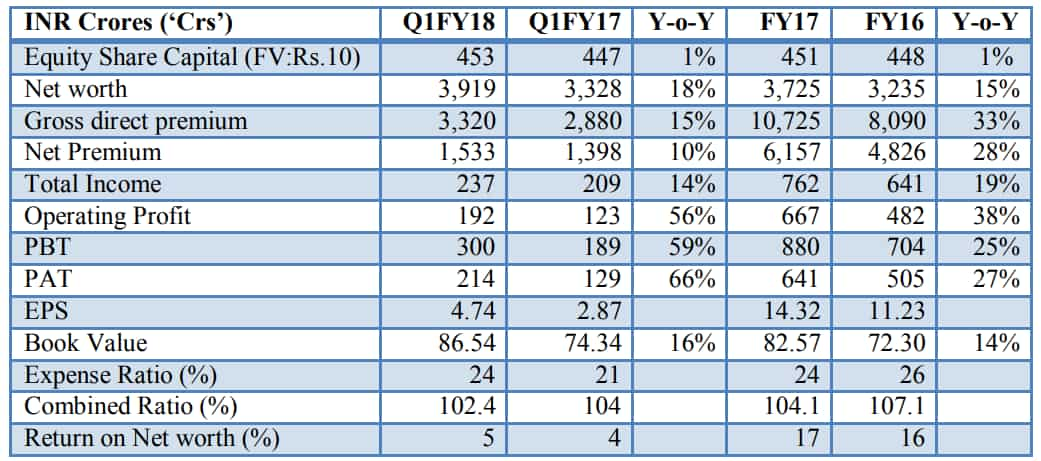

ICICI Lombard became the 1st Private Sector General Insurance Company in India to cross the Rs 10,000 crore mark in terms of premium income.

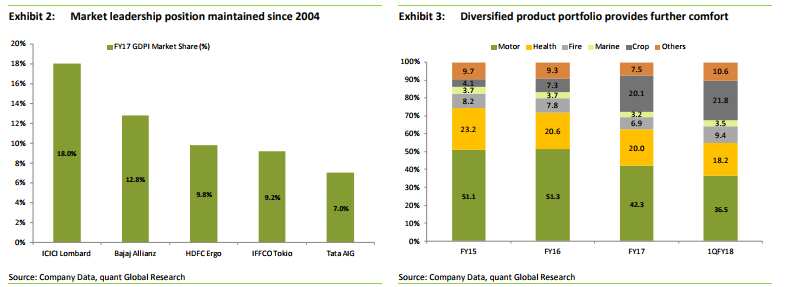

The company has a diversified composition of insurance products with motor, health and personal accident crop/weather, fire, marine, and engineering insurance contributing 42.3%, 18.9%, 20.1%, 6.9%, 3.2% and 2.1%, respectively, of its GDPI in fiscal 2017.

ICICI Lombard’s gross direct premium has grown at a CAGR of 15% in last 5 years to Rs 10,725 crore in FY17 (FY13: Rs. 6,134 crore) indicating a strong growth for general insurance business in the Indian economy for the years ahead.

Compared with peers, ICICI Lombard holds the leadership in non-life insurance and has maintained it since 2004.

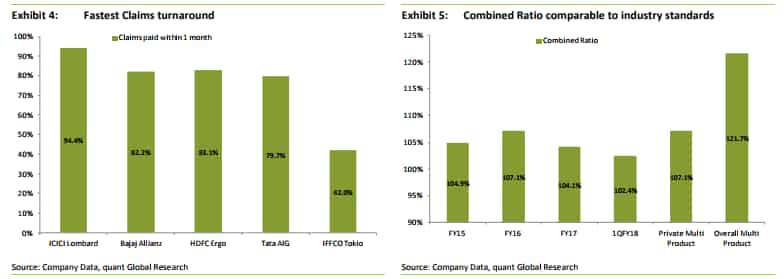

In terms of settlement claims, ICICI Lombard takes the top spot with 94.4%, followed by Bajaj Allianz at 82.2%, HDFC Ergo at 83.1% and Tata AIG at 79.7%.

It has a strong capital position with a solvency ratio of 2.10x as at March 31, 2017 compared to the IRDAI prescribed control level of 1.50x, and an Indian non-life private-sector average of 1.95x.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

01:15 PM IST

ICICI Lombard surges higher after insurance firm's Q3 results meet Street estimates

ICICI Lombard surges higher after insurance firm's Q3 results meet Street estimates ICICI Lombard General Insurance Q3 results due on Tuesday; here's what to expect

ICICI Lombard General Insurance Q3 results due on Tuesday; here's what to expect Profit-booking in ICICI Lombard? General insurer's stock hits a speed bump after Q4 results

Profit-booking in ICICI Lombard? General insurer's stock hits a speed bump after Q4 results ICICI Lombard, IGL, Zomato, United Spirits, Coal India: Should you buy, sell or hold stocks in focus today?

ICICI Lombard, IGL, Zomato, United Spirits, Coal India: Should you buy, sell or hold stocks in focus today? ICICI Lombard trades in green as company delivers better-than-expected Q2 results

ICICI Lombard trades in green as company delivers better-than-expected Q2 results