Do they really want to solve "bad loan" problem?

N. S. Vishwanathan, Deputy Governor of RBI said, "If banks continue to remain saddled with huge NPAs for a long time, it would make them risk averse and choke the lending for economic activities in general. "

Stressed loans of banks have now risen by 15% to $138 billion (approx Rs 8,71,746 crore) in June 2016, an increase of 15% in just six months, Reuters reported.

Stressed assets is mixture of non-performing assets (NPAs), restructured loans and written off assets. They are realized when a borrower fails to pay its principal amount of loan and interest for a of 90 days.

Total stressed assets in the Indian commercial banks have risen to 11.5% with public sector banks leading the strain at 14.5 % as at end-March 2016, Reserve Bank of India (RBI) data show.

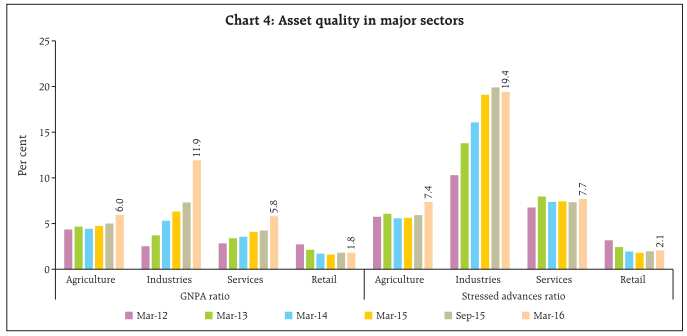

Sectoral distribution of NPAs:

Industries' gross non-performing assets (GNPA) ratios rose by 11.9% as on March 2016, while stressed advances ratio stood at 19.4%.

Sectors like agriculture, services and retail were below 6% in GNPA with agriculture sector being the minimum.

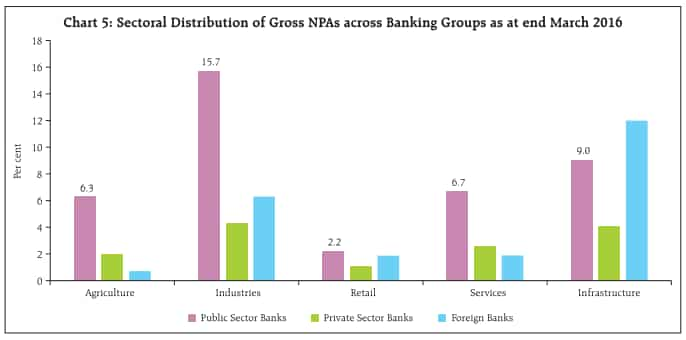

Public Sector Banks (PSBs) gross NPAs are highest, at 15.7%, while in infrastructure sector is at 9%, Agriculture at 6.3%, services at 6.7% and retail sector at 2.2%.

To bring discipline, RBI has tightened the norms for lending to large corporate which will be in effect from financial year 2018.

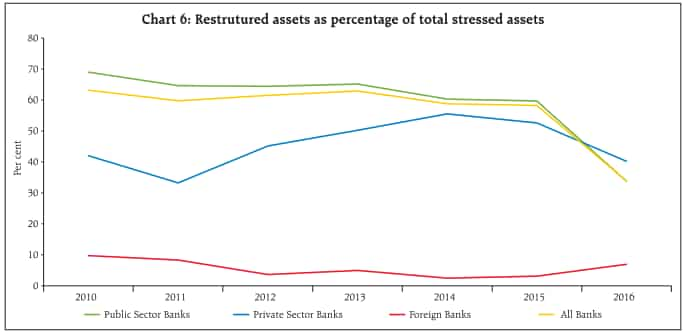

Restructured assets:

RBI said,"During the five years to March 2015, banks have resorted to restructuring of loans in many cases to postpone recognition of non-performance, or what we now call ‘extend and pretend’, rather than using it as a tool to preserve the economic value of the units as intended."

As a result, until 2016 the restructured assets included more than 50% of the stressed assets of all scheduled commercial banks hiding the actual extent of failure of the loan portfolios.

Proportion of these assets was much higher in public sector banks.

The outstanding balance of these assets declined sharply in 2016 post-AQR (asset quality review), as a major portion of these assets has been classified as NPA post AQR reflecting their true quality, stated RBI.

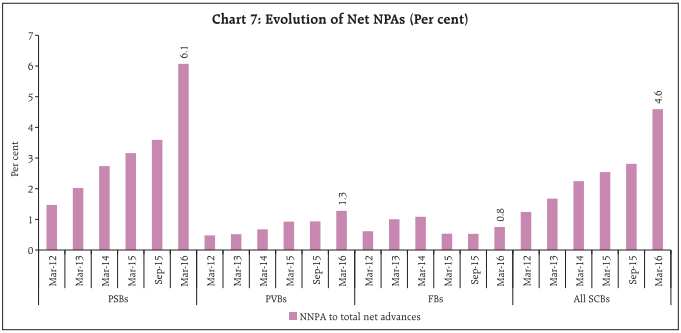

Net NPAs:

There has been consistent rise in net NPAs under banking sector, especially PSBs which has hampered their earnings.

Higher net NPAs show-cases lower provision coverage ratio which should progressively improve as the strain on profitability eases, said RBI.

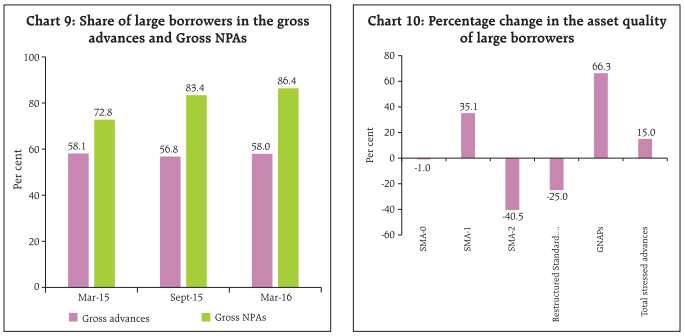

Large Borrowers:

It is also noted that the stress is higher in large borrowers’ accounts. Under overall credit portfolio, share of industrial advances is around 40%.

While this is partly explained based on the relatively higher credit intensity of industrial sector, banks have to see the need for proper balance taking into account the risk return trade-off especially in the larger loan segment, RBI added.

N. S. Vishwanathan, Deputy Governor of RBI said, "If banks continue to remain saddled with huge NPAs for a long time, it would make them risk averse and choke the lending for economic activities in general. "

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

11:16 AM IST

PNB aims to recover Rs 32,000 cr from bad loans resolution this fiscal

PNB aims to recover Rs 32,000 cr from bad loans resolution this fiscal Bad loan ratio of banks likely to fall to 5-5.5 pc by March 2024: S&P Global

Bad loan ratio of banks likely to fall to 5-5.5 pc by March 2024: S&P Global RBI crackdown on NPA: What is Reserve Bank's 'Prudential Framework' plan to deal with stressed assets

RBI crackdown on NPA: What is Reserve Bank's 'Prudential Framework' plan to deal with stressed assets Syndicate Bank hopes to recover Rs 1,500 crore from non-performing assets

Syndicate Bank hopes to recover Rs 1,500 crore from non-performing assets Provision coverage ratio of PSU banks on the rise, crosses 66 pc

Provision coverage ratio of PSU banks on the rise, crosses 66 pc