Avenue Supermarts Q4 results: Healthy revenue, PAT expected?

Within three weeks of its listing, the company managed to cross Rs 800 per piece, which makes it the most expensive share in retail segment.

Recently listed retail major Avenue Supermart (parent company of D-Mart) is set to announce its financial results for the quarter ended on March 31, 2017 on May 6. This will be the first time the company will be announcing result on BSE since its listing.

With its listing on March 21, the company made its investors "richie rich", with shares rising 114.3% from its offer price on its debut. In fact Radhakishan Damani, founder of D-Mart, became richer by Rs 6,100 crore.

Within three weeks of its listing, the company managed to cross Rs 800 per piece, which makes it the most expensive share in retail segment.

What experts say

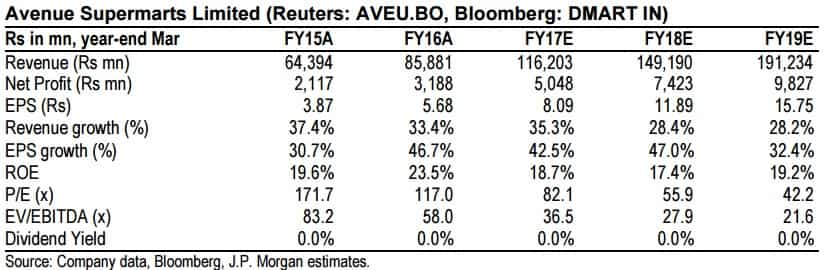

According to a report by J P Morgan, despite its capital-intensive strategy of ownership (vs renting), its asset turns are similar to peers. The analysts believe it is a relatively “safe” play on India’s consumption growth story, given the non-cyclical nature of the food retail business.

Despite low gross margins (owing to low price positioning), ASL has amongst the highest EBITDA margins (vs peers) owing to tight control on operational costs (employee, SG&A) and high sales comps, the report mentioned.

However, the threat from the e-commerce players and slower-than n-expected network expansion and/or tepid SSSG (same store sales growth), are the major risks for the company.

"Any minor lapse near term (store opening, comps, and/or margins) and substantial investments in E-Commerce (earnings dilutive) could strain valuation multiples," it said.

Commenting on the estimate for the whole financial year, the report said that post the "bumper" listing, valuations at 55x/42x FY18E/19E P/E leave little room for disappointment. The research agency predicts the company's net profit to be around Rs 5,048 million in FY17 as against Rs 3,188 million in FY16 and Rs 2,117 million in FY15.

"We forecast 27%/34% revenue/EPS CAGR over FY17-20," it added.

Having similar prediction, Kotak Institutional Equities in its research report said DMart to report healthy revenue, EBITDA and PAT CAGR of 26%, 28% and 35% over FY2017-20 led by robust SSSG, sustained addition to store count and steadily improving margins.

EBITDA margin expansion and repayment of debt post the recent fund raise in the IPO will lead to sharp expansion in PAT margins from 3.3% in FY2016 to 3.7% in FY17 and 5.4% by FY20. Strong revenue growth, stable margins and steady pace of store addition will drive free cash flow generation FY19 onwards, the report stated.

On Friday, at 1445 hours the shares of the company were trading at Rs 795.25 per piece, up 2.90% or Rs 22.40 on BSE.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

02:58 PM IST

Avenue Supermarts shares slip over 4% post-Q3 business update; here is what brokerages say

Avenue Supermarts shares slip over 4% post-Q3 business update; here is what brokerages say Brokerages divided on Avenue Supermarts shares despite robust Q3 earnings – check target prices

Brokerages divided on Avenue Supermarts shares despite robust Q3 earnings – check target prices  D-Mart reports 23.6% rise in Q3 consolidated net profit to Rs 552.53 cr

D-Mart reports 23.6% rise in Q3 consolidated net profit to Rs 552.53 cr Avenue Supermarts Ltd-owned D-Mart's Q3 revenue up 22% at Rs 9,065 cr

Avenue Supermarts Ltd-owned D-Mart's Q3 revenue up 22% at Rs 9,065 cr Consumer discretionary companies’ shares on a roll; Titan, DMart, Jubilant Food, Barbeque Nation hit new life highs

Consumer discretionary companies’ shares on a roll; Titan, DMart, Jubilant Food, Barbeque Nation hit new life highs