Airtel's weak third quarter operating result weigh on Baa3 rating, Moody's says

Chiara said, " We still expect Bharti's cash flow from operations and monetisation opportunities -- including divestments in subsidiaries -- to reduce absolute debt levels permanently to expedite deleveraging towards 3x over next 6 months. Bharti has no headroom for any delay in its deleveraging plans,."

Moody's Investors Services stated that though weak operating results of Bharti Airtel in third quarter (Q3FY17) is credit negative, yet it will not have an immediate effect on the company's Baa3 issuer rating and stable outlook.

Di Chiara, Moody's lead analyst said, “This primarily reflects declines in ARPUs across mobile services - voice and data - and as well as a 12.4% drop in data customers QoQ, as India's newest mobile operator, Reliance Jio Infocomm (unrated) in its promotional entry proposition - providing all services free of charge - continued to drive intense price competition.”

This Q3, Bharti Airtel faced decline in average revenue per user (ARPU) by 10% year-on-year (YoY) to Rs 172. Also voice RPM (revolutions per minute) fell by 9% quarter-on-quarter (QoQ) to Rs 294 per minute due to higher proportion of incoming traffic. On the other hand, voice traffic grew by 5% qoq to 330 min, led by high incoming traffic from Jio.

Chiara said, "Still this elevated leverage can be accommodated in the rating for a short period of time. We still expect cash flow from operations and monetisation opportunities -- including divestments in subsidiaries -- to reduce absolute debt levels permanently to expedite deleveraging towards 3x over next 6 months. Bharti has no headroom for any delay in its deleveraging plans,."

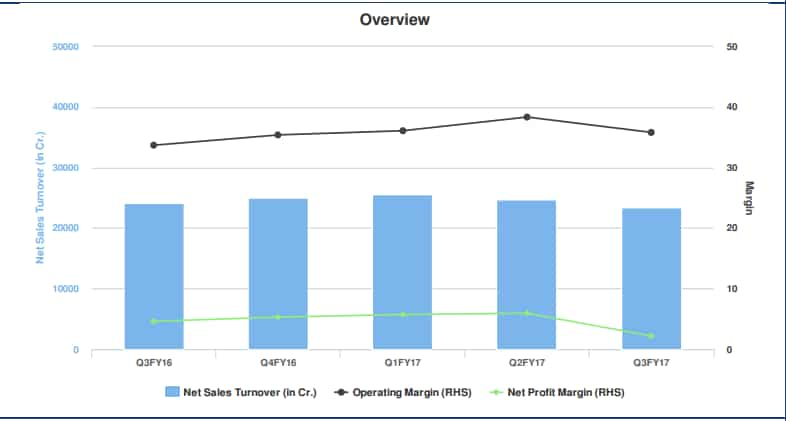

Here is an overview of Bhart Airtel's financial performance in previous quarters.

India Infoline, in its report, said, "Airtel management expects free offers to impact everyone in the short term. It believes blended ARPU is the key metric since bundled offerings would be the way forward in the market which over longer term would lead to customer upgrades."

It added, "Bharti could launch Rs 2000 4G feature phone in April-June 2017 period, but would subdise, given that feature phones account for 65% of the sector revenues, it would be prudent not to ignore such large revenues base. "

Another analyst report from Motilal Oswal said, "Management believes there is a strong market share improvement potential and once the dust settles and free usage ends, there is a strong growth opportunity in the market."

It said, "Bharti's free offerings will be countered by financial prudence at some point as return on capital will start getting prioritized. The effect of the market disruption is high on smaller players as the low prices will challenge their position."

Overall, India Infoline stated, Bharti is still best bet to ride out the Jio blitzkrieg, we remain wary of the damage to earnings in the interim.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

12:09 PM IST

Airtel become first private telecom to connect Kupwara, Baramulla, Bandipore

Airtel become first private telecom to connect Kupwara, Baramulla, Bandipore  Midday Market Report: Sensex tumbles 930 points, Nifty slips below 24,400; Airtel, TCS drag

Midday Market Report: Sensex tumbles 930 points, Nifty slips below 24,400; Airtel, TCS drag  Bharti Airtel, TCS, ICICI Bank, 2 other blue-chip firms gain Rs 1.1 lakh crore in mcap in a week

Bharti Airtel, TCS, ICICI Bank, 2 other blue-chip firms gain Rs 1.1 lakh crore in mcap in a week Bharti Airtel hits 7-week high; shares surge 4% on heavy volumes

Bharti Airtel hits 7-week high; shares surge 4% on heavy volumes Airtel flags 8 billion spam calls, 800 million spam SMSes

Airtel flags 8 billion spam calls, 800 million spam SMSes