Financial planning: Just married? This is what you need to keep in mind to manage expenses

From taking care of your parents to family planning, list of expenditure will grow with each passing year if you are recently married. What to do in such case?

Once you are married, comes series of responsibilities. More the responsibilities more will be the expenses.

From taking care of your parents to family planning, list of expenditure will grow with each passing year. What to do in such case? Loans?

Taking loan is always an open option, but before that you need to do financial planning. The first step to making a financial plan is taking stock of your liabilities and stating your goals.

In case when you are just married and moving towards new phase of life by starting a family, your investments which you need to keep in mind are expenses associated with the education of your children, health of your parents, your own, spouse and child’s health, and your retirement plans.

In addition to these, you may also want to save up for your child’s higher education or wedding expenses. At some point, you may also want to purchase a house or car if you do not have one of your own.

In short, these will be never ending expenditures. You have to be financially ready at each point.

But, before all the investment planning, comes "securing". If you are already investing small amount, the immediate step is to make sure that you and your dependents are adequately covered. If you do not have a personal health insurance policy for yourself and your family, this is the time to get one.

Ajit Narasimhan, Category Head - Savings and Investments, BankBazaar.com said, "Get a health insurance for your parents as well. With medical expenses on the rise, it is always good to have some form of backup. You might also want to consider a term insurance that can provide cover in case of any unforeseen circumstances."

Now, you should start planning for all milestones for which you need to save.

For instance, you may want to purchase a car in the next two years or a house in the next five years. Calculate the amount of funds you would need for the same keeping inflation in mind.

Remember, that you would not get the full amount as a loan even if you are eligible. So, a part of the cost (as well as the registration expenses in case of a house) will have to be bourne by you.

"Once you have a rough understanding of these expenses, break it down to how much you would need to save every month in order to build your corpus, and start investing accordingly. The same applies to every milestone, such as children’s education or marriage. More the time you have, the bigger would be your corpus," Narasimhan added.

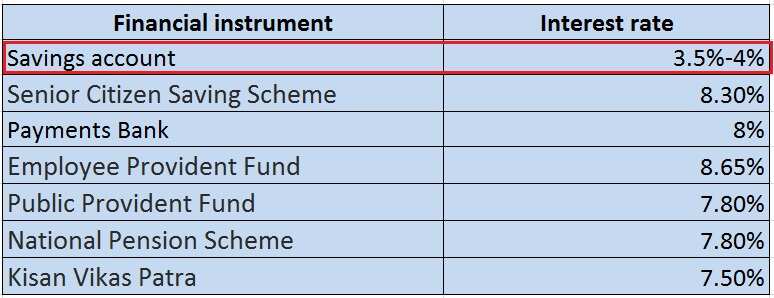

Unlike earlier times, where only few investment options were known, now a days, there are many financial instruments which you can choose depending on your goals.

Here's a list of instruments and rate of returns:

Disclaimer: This story is for informational purposes only and should not be taken as an investment advice.

ALSO READ:

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

02:00 PM IST

10 Financial habits to avoid for a smoother and diligent financial life

10 Financial habits to avoid for a smoother and diligent financial life  The Rule of 72: How long will it take for your monthly investment to cross Rs 10 lakh with 12% returns?

The Rule of 72: How long will it take for your monthly investment to cross Rs 10 lakh with 12% returns? Why for achieving financial freedom investors need to have adequate insurance coverage?

Why for achieving financial freedom investors need to have adequate insurance coverage? HCLTech elevates Shiv Walia as Chief Financial Officer

HCLTech elevates Shiv Walia as Chief Financial Officer Why over diversification of portfolio can jeopardise your financial planning? Know expert view

Why over diversification of portfolio can jeopardise your financial planning? Know expert view