Was Q4FY17 able to bring cheer in corporate sector?

There was continued weakness in private capital expenditure cycle, absence of broader consumption pick-up and sluggish asset quality trends in financials.

The last financial year (FY17) saw a lot of turbulence, change in strategies and in total a bag mixed of ups and downs.

Beginning from this week, the companies will be announcing their financial results for the quarter ended on March 31, 2017 along with overall financial year performance.

How was FY17?

The financial year 2017 started with higher hopes of an "ever-elusive earnings recovery". This was backed by good monsoon expectations, 7th Pay Commission awards and benefits, passage of Goods and Service TAx (GST) and positive macro lookout.

But the whole scenario changed. There was continued weakness in private capital expenditure cycle, absence of broader consumption pick-up and sluggish asset quality trends in financials. Moreover, adding to it were events like demonetisation, which turn-around the financial situations, leading to a flatting earnings performances.

How Q4FY17 earnings will be?

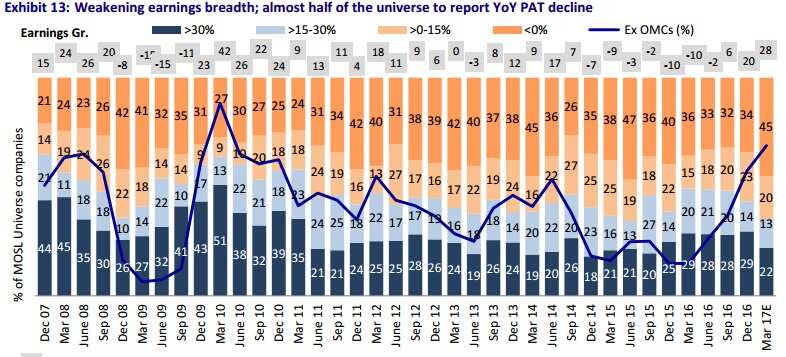

The earnings growth is expected to be at 11-quarter high at 28%, but the quality is expected to remain weak, as suggested by Motilal Oswal in its research report.

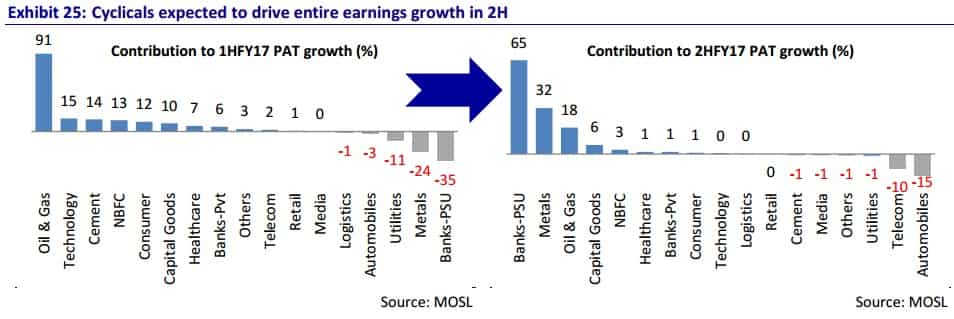

As per the report, excluding public sector banks (PSUs), Metals and Oil & Gas sectors, the companies' profit after tax (PAT) is expected to drop by 5.9% on year-on-year basis. However, entire financial year growth of Rs 224 billion for companies in Q4FY17 will be led by PSU Banks and Metals.

Niket Shah and Chintan Modi, Analysts at Motilal Oswal, in the report titled 'Q4FY17 Preview', said, "We cut our FY18/FY19 Sensex EPS estimates by 4% to Rs 1,572/Rs 1,904. We now expect 1% EPS decline for Sensex in FY17, followed by 20% growth in FY18 on a low base of H2FY17."

Moreover, the report mentioned that the earnings picture in Q4FY17 appears to have an "uncanny resemblance" to that in the previous quarter, with select sectors driving the performance led by favorable bases.

Shah and Modi, said that they estimate EBITDA growth at 8.3% on year-on-year, the lowest in four quarters, underpinned by margins disappointment after eight consecutive quarters of expansion.

PAT is likely to grow 28% YoY, the highest since 1QFY15 (18% decline in the base). Also, 4QFY17 is estimated to be the third straight quarter of double-digit PAT growth.

"However, it is largely led by the depressed bases of PSU Banks, Oil & Gas (PAT down 24%) and Metals (PAT down 19%). Excluding these sectors, we estimate 4.4% YoY sales growth, 2.5% YoY EBITDA decline and 5.9% YoY PAT fall," the report mentioned.

A quick sector review

Auto sector: According to the research agency, the auto sector is expected to witness adverse impact by commodity cost inflation, costs related to BS-III inventory clearance, sluggish two-wheeler sales and continued margin headwinds for Tata Motors.

Auto aggregate PAT is expected to decline 32% YoY. Excluding Tata Motors, PAT should grow 2% YoY, the report said.

Information technology: Technology is expected to witness another sluggish quarter, with muted 2% EBITDA growth and first-ever quarter of YoY decline in PAT.

Cement, Media, Retail and Telecom are also expected to report decline in PAT on year-on-year basis at (-22%), (-31%), (-12%) and (-85%) respectively, the report mentioned.

However, Private Banks (18%), Capital Goods (15%), Consumer (5%), NBFC (11%), Healthcare (6%) and Utilities (1%) are expected to post PAT growth.

PSU Banks: Punjab National Bank, Bank of Baroda and Canara Bank, which reported losses in the previous quarter, are expected to report profits in 4QFY17. Bank of India and Oriental Bank of Commerce are estimated to post losses.

NBFCs are likely to see moderation, posting 11% YoY PAT increase after three consecutive quarters of 16-20% growth. Bajaj Finance (44%), Dewan Housing (30%), Indiabulls Housing (26%), LIC Housing Finance (19%), Muthoot Finance (23%) and Gruh Finance (18%) are expected to deliver strong performance.

Private Banks are expected to report healthy 18% YoY PAT growth – the best in nine quarters. ICICI Bank (+3.3x), RBL (71%), Yes Bank (30%), Kotak (28%) and IndusInd (23%) are expected to post strong performance, while Axis (-61%) will have a muted quarter.

Capital Goods sector is expected to post muted performance with flattish PAT excluding BHEL. BHEL is expected to post 3x jump in PAT YoY, which should aid sector PAT growth of 15%.

Metals would have a bumper quarter, reporting PAT of Rs 91 billion (+2.8x YoY) and highest absolute PAT in 19 quarters. Hindustan Zinc (+2.7x), Vedanta (+2.1x) and Tata Steel (+2.1x) are expected to post strong results.

Oil & Gas would report healthy 16% YoY PAT growth – fourth consecutive quarter of double-digit growth. Indian Oil (+3.3x), Indraprastha Gas (+41%), Gail (+44%), ONGC (+65%) and Petronet (+66%) are expected to report strong performance.

Telecom would report PAT decline (-85% YoY), despite the low base (PAT was down 2% YoY in 4QFY16). PAT of Rs 4.3 billion for our Telecom universe is the lowest in multiple quarters.

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.